Animoca Brands再获巨额融资

2022年9月8日,风险投资公司Animoca Brands宣布已经获得由淡马锡、博裕资本和GGV资本支持的1.1亿美元融资。

此次融资将以发行可转换票据的形式进行,而这些可转换票据日后可能转换为股票的形式。Animoca表示,该票据的到期日为发行之日起的三年,可以在该日之前的任何时间由票据持有人选择进行兑换。它将利用新资金继续为战略收购、投资和产品开发提供资金,确保流行知识产权的许可,并推进“开放元宇宙”,包括努力为在线用户推广数字产权。

其实早在今年7月12日,Animoca Brands就以59亿美元的投前估值完成了一笔7532万美元的融资,投资者包括Liberty City Ventures、Kingsway Capital、Alpha Wave Ventures、10T、SG Spring Limited Partnership Fund、Generation Highway Ltd、Cosmic Summit Investments Limited等。而这轮融资实际上属于今年1月份由Liberty City Ventures领投的3.588亿美元融资的第二部分。

Animoca Brands作为加密顶级风投机构,其一举一动可以说是备受瞩目。然而在现如今熊市氛围的渲染之下,Animoca Brands等一众头部机构但凡有一些风吹草动都会牵动用户的内心,乃至左右其对市场的认知,因此今天就让我们通过Animoca Brands的投资布局来共同探究一下接下来的加密市场可能迎来的走向。

从开始,到低谷

Animoca Brands是一家从Animoca公司拆分出的子公司,Animoca是由香港著名科技创业家萧逸(Yat Siu)创立于2014年的链游开发与投资公司,总部位于香港。

Animoca Brands不仅是元宇宙头部项目The Sandbox、NFT赛车游戏F1 Delta Time的开发商,还是Dapper Labs、Decentraland等明星项目的早期投资者。除此之外,Animoca Brands还拥有哆啦A梦、樱桃小丸子、漫威等大IP漫画手游的开发代理权。

Animoca Brands的创始人是Yat Siu,他出生于二十世纪80年代,童年在维也纳度过,由于其中国血统,他总是感觉自己难以融入维也纳的主流社会。好在凭借其从小对科技的热情,而他又恰逢生长在计算机和互联网蓬勃发展的时代,Yat Siu找到了属于自己的避难所,通过技术排解了孤独。

在经历大学辍学与几次创业的经历后,Siu于1995年定居香港,他创立了亚洲首家免费网页和电子服务提供商。

时间来到1998年,他创办了集游戏开发和网络服务业务于一身的Outblaze,在屡获多项殊荣后,2009年,Yat Siu以数亿美元的价格将公司的云部门卖给了IBM。

之后,Yat Siu将更多精力放在投资最前沿的新赛道上。于是在2014年,Animoca Brands应运而生。

在Animoca Brands成立之初,Yat Siu将其定位为移动游戏公司,主要以手游研发和发行业务为主,业务范围甚至一度涉及电子书。也许是由于Yat Siu常年的外国生活经历,相较于一般的手游公司,Animoca比较重视IP授权的游戏,先后研发了《加菲猫》、《哆啦A梦》、《铁臂阿童木》等超级IP的授权手游。

2015年1月,Animoca Brands在澳大利亚证券交易平台上市,尽管其已经有了一定的影响力,但在盈利方面却还是平平无奇,甚至不得不通过多次融资来不断补充现金流。

据相关报道数据显示,Animoca Brands从2015年到2019年总共进行了9轮IPO融资,累计金额达3430万美元,这些资金大多用以推进各类手机游戏、电子书、VR、链游等业务的发展,但最终却都收效甚微。

截止2017年第四季度,Animoca Brands的季度经营现金流持续保持负数。除此之外,据数据显示,该公司在17年8月的股价从此前的高点0.2澳元一度跌至0.01澳元以下,跌幅超 95%。

时间来到2017年下半年,在澳大利亚证券交易平台对业绩问询的压力下,Animoca Brands进行了三项以精简成本、提高营收为目的的改革,具体包括:调整董事薪酬结构、出售非核心资产,以及裁员。

在改革举措推出之后,Animoca Brands的全体高管减薪50%;且该公司以800万美元总价出售了旗下524款手游中的318款。此外,公司的员工总数也从110余人锐减至不到70人。这些激进的举措使得Animoca Brands艰难的度过了退市危机。

而2017年也成为了Animoca Brands的转折之年。因为在这一年,Animoca Brands开始正式涉足于区块链和NFT市场。

加密即是转折

2017年底,Animoca Brands开始接触一家参与过CryptoKitties开发的游戏公司。通过同该公司的接触,Yat Siu敏锐的嗅到了隐藏在NFT市场的巨大潜力,因此从那时起,Animoca Brands 开始专注于基于NFT的游戏。

在接下来的两年里,Animoca接连投资了Axie Infinity的开发商Sky Mavis、OpenSea平台、Wax公链以及Decentraland,还收购了The Sandbox。

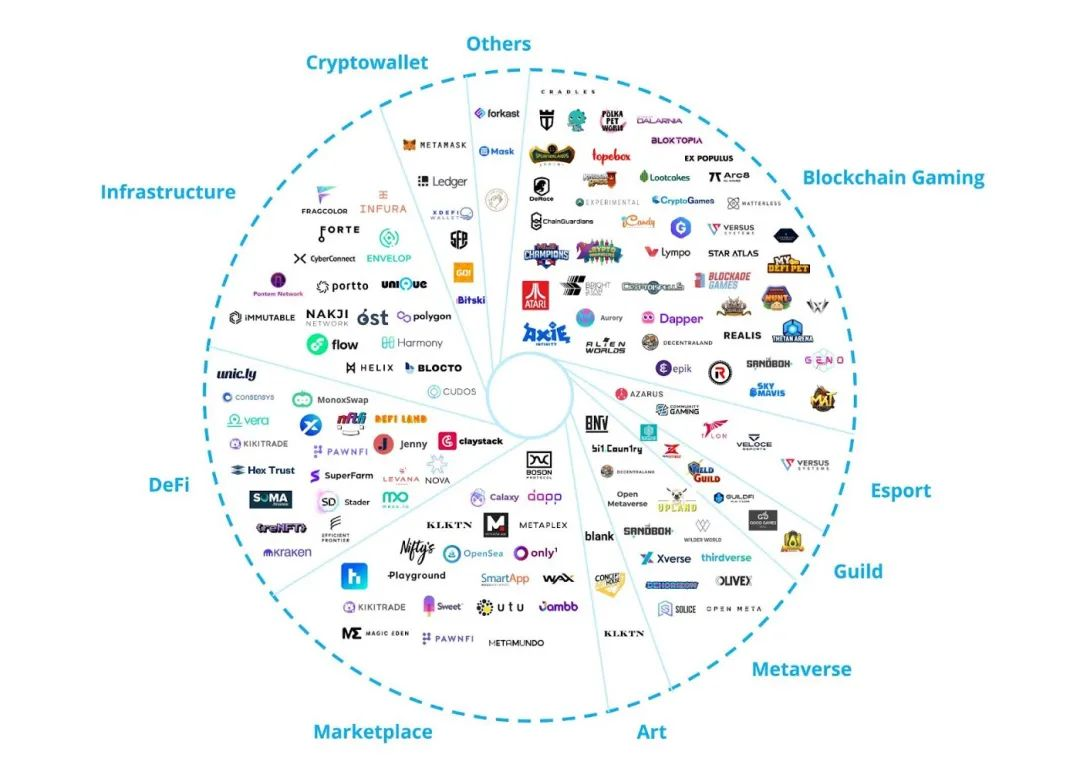

根据Animoca Brands公布的2021年最后3个月至2022年前4个月未经审计的主要财务和业务报告数据显示,Animoca Brands参与的投资项目约为340余项,总投资金额达15亿美金。投资项目主要涉及区块链游戏、电子竞技、公会、元宇宙、艺术、市集、去中心化金融、基础设施、加密钱包等。

而在众多赛道之中,Animoca Brands投资金额前三的分别为区块链游戏、Web3基础设施和DeFi,投资金额分别占总投资金额的35.4%、14.8%和10.6%。

从Animoca Brands领投参投项目的分布来看,312个项目中,Animoca Brands领投项目有84个,参投的项目达119个,参与战略投资成为合作伙伴的项目数量和收购项目数量分别为90个和18个。

这些数据虽然相当直观,但由于时间跨度过长,还不足以用来预测市场接下来的走向。因此,接下来我们将仅对2022年上半年的数据进行分析。

2022投资数据分析

据统计,Animoca Brands在2022年上半年共进行了66笔投资,投资总额超过1.85亿美元。其中,大约三分之二的投资流向了游戏和基础设施。而游戏领域内的投资又占据了最大的比例,共包含28笔交易。

平均而言,Animoca Brands每月大约完成11笔投资。但自5月起,其出手次数显著下降,其原因也不难理解,毕竟当时整个加密市场都被Luna/UST的崩盘拉入谷底。

进入6月后,Animoca Brands逐渐开始恢复其投资频率,并且当月支出达到了上半年之最。究其原因,很可能是由于大量5月就已完成融资的项目出于种种考虑直到六月份才正式公布。果不其然,紧接的7月Animoca Brands只宣布了一笔投资。自此,Animoca Brands可能已经在逐步放缓自己的投资节奏。

而从Animoca Brands的投资倾向来看,我们对当下的市场也将有一些新看法。

首先,Animoca Brands在2022年上半年的投资大部分都流向了游戏和基础设施。关于基础设施赛道的投资,在当下整体走熊的大背景下是相当符合逻辑的。毕竟牛市加码应用,熊市关注基建。但游戏作为典型的应用端,其受关注的程度却超过了更加符合熊市投资逻辑的基础设施,这不免会让人思考Animoca Brands对于接下来市场爆点的研判是否就落在GameFi之上。

回想之前的几轮爆点,如Defi、NFT,其所具备的特性同GameFi也的确存在一些相似之处,而年初STEPN的成功也打破了人们以往的认知,成功接棒了牛市最后的爆点。

因此,在这多重因素的推进之下,诸多顶级机构将GameFi作为下轮牛市的种子选手可以说不足为奇。这一点从他们的投资布局中也可以管中窥豹。

GameFi——下轮牛市的种子选手

在我看来GameFi是一个具有天然优势的赛道。

首先,游戏本身就天然具有吸引力。

根据数据显示,当前全球游戏产业的产值已经超过3000亿美元,其超过了电影和音乐产业的总和。而现实生活中也有大量玩家已经将游戏视为生活的一部分。

而相比于普通游戏,GameFi中的游戏资产完全归属于玩家所有,并且可以兑换为现实收入。试想一下,一般的游戏已经让无数玩家愿意投入其中,甚至花费大量金钱和精力。

那么如果出现一种可以让玩家完全掌握自己的数据资产,甚至能够靠它谋生的游戏,将带来多少可能性?

其次,GameFi降低了普通人进入Web3和加密市场的知识和技术门槛。

在快节奏的现代社会生活中,普通人很难有兴趣专门再去学习Web3的相关知识。而GameFi却可以以游戏的形式吸引玩家进入Web3,在娱乐的过程中实现无痛进入加密市场。

甚至目前已经出现了STEPN这种GameFi进军现实生活的成功案例,这为Web3同现实的交融提供了全新的思路。

况且,如Animoca Brands的诸多头部机构也在大力押宝GameFi,作为散户的我们很难不看好其发展前景。