In crypto trading, market crashes leave marks that investors don’t forget.

Looking back at Q4 last year, things were rough across the board; spot trading and even long-term HODLing all took a hit. Crypto markets lost nearly $1 trillion, triggering massive liquidity sweeps, forcing deleveraging, and sending shocks across the market, which left investors cautious and their sentiment fragile for months.

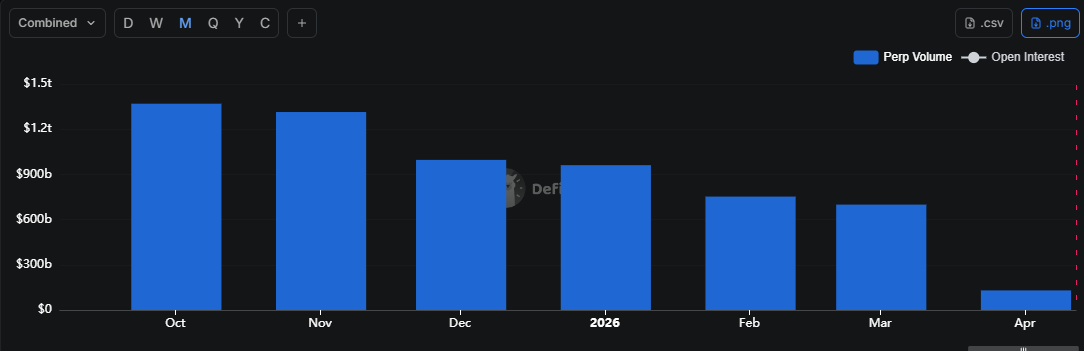

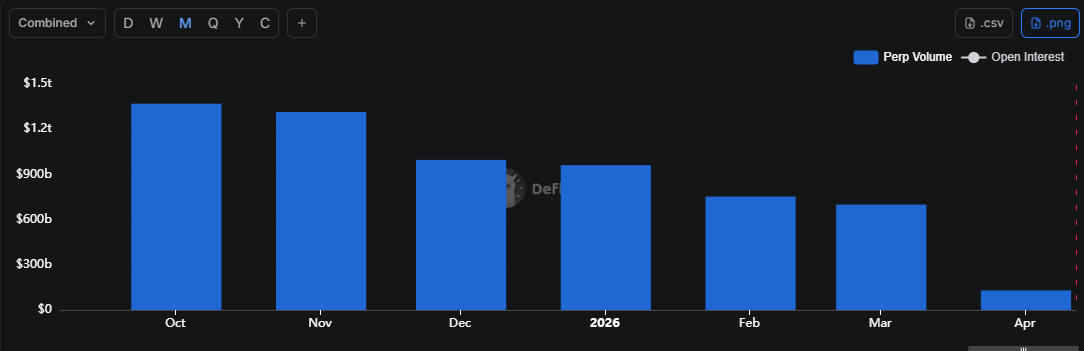

Fast forward to now, that wave of volatility hasn’t fully disappeared. Data from DeFiLlama shows that perpetual volumes across major DEX chains have been on a steady decline for five consecutive months. From a peak of $1.36 trillion in October 2025, volumes slid all the way down to $699 billion by March 2026.

Technically speaking, traders wiped out nearly half of last quarter’s perp volume. For context, perp volume measures the total value of all perpetual contract trades happening on decentralized exchanges. It’s basically a snapshot of how actively traders are betting on short- and long-term price moves in crypto.

And let’s be real, anything involving “bets” is pure speculation. In a bull market, that speculative capital acts like rocket fuel, pushing rallies higher and giving momentum to the market. But since the October crash, crypto still sits about 40% below pre-crash levels, showing how much ground the market has yet to cover.

So what do we make of falling perp volume in a bear market? Could it be a healthy sign that traders are stepping back and markets are consolidating, or is it a warning that liquidity is drying up?

Falling perp volumes highlight lingering bear market pressure in crypto

Unlike spot trading, speculative trading is highly sensitive to macro conditions.

In other words, traders in perpetual markets don’t just react to crypto-specific news. Instead, they watch the broader financial landscape closely. Global market shifts, interest rate changes, and even geopolitical events can quickly influence their positions. In this context, that nearly 50% wipeout of perp volume really highlights the bearish setup the market is facing right now.

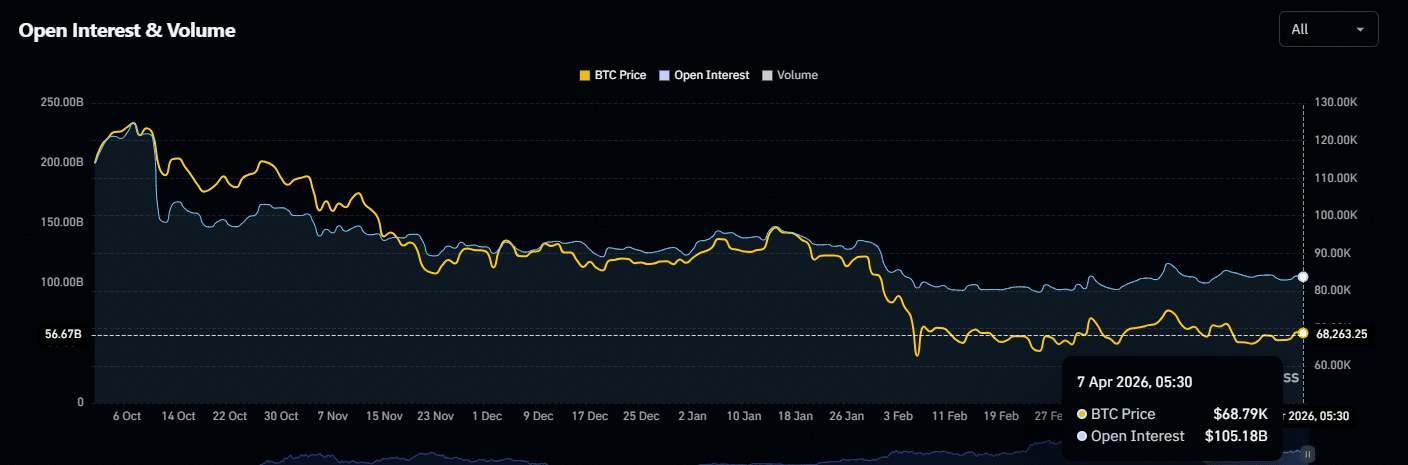

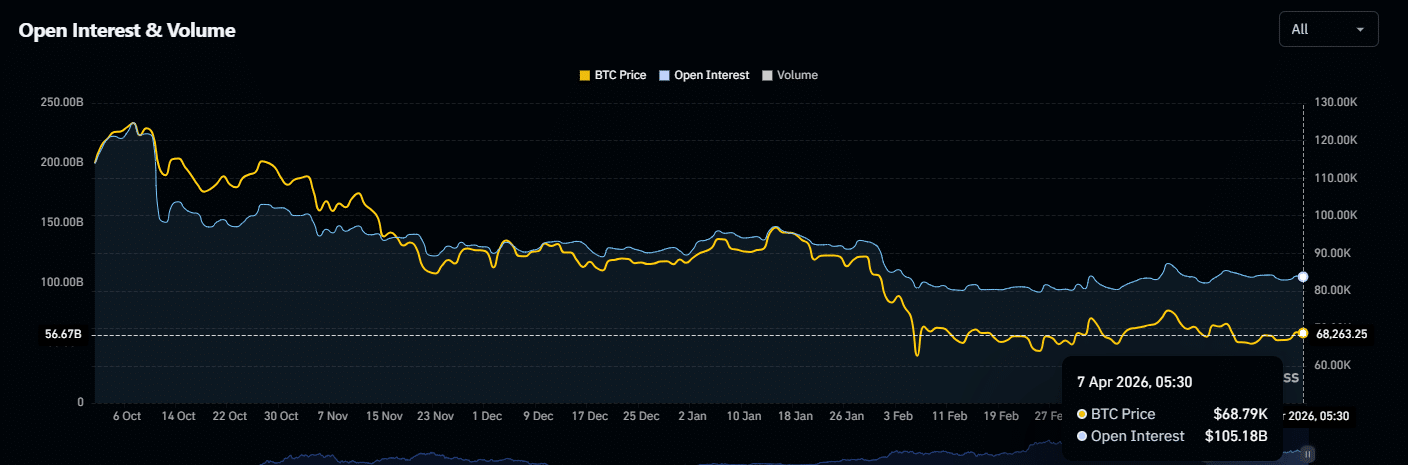

Adding to that, Coinglass data shows that open interest (OI) across all crypto assets combined has also dropped 50% from the $200 billion pre-October levels. For context, open interest is basically the total value of all “outstanding” contracts that haven’t been settled yet, showing how much capital traders have at risk.

Taken together, the drop in perp volume and open interest tells a clear story: crypto traders are actively recalibrating risk and waiting for clearer signals before jumping back in. In a bear market, that’s actually a bullish sign. It indicates that traders aren’t blindly chasing moves. Instead, they’re letting the market settle, which helps reduce the risk of sudden swings and wild volatility.

At the same time, the scars from the October crash haven’t fully healed.

Still, traders are taking notes from past shocks, pulling back when risk is high, and redeploying capital more strategically. As a result, the market may look quiet on the surface, yet behind the scenes, this cautious behavior is quietly building a stronger foundation for crypto’s next move.

Final Summary

- Perp volume and open interest are down nearly 50%, reflecting traders’ caution and a still-bearish market setup.

- Measured trading behavior in a bear market helps stabilize liquidity, limit volatility, and lay the groundwork for the next crypto rally.