撰文:ChandlerZ, Foresight News

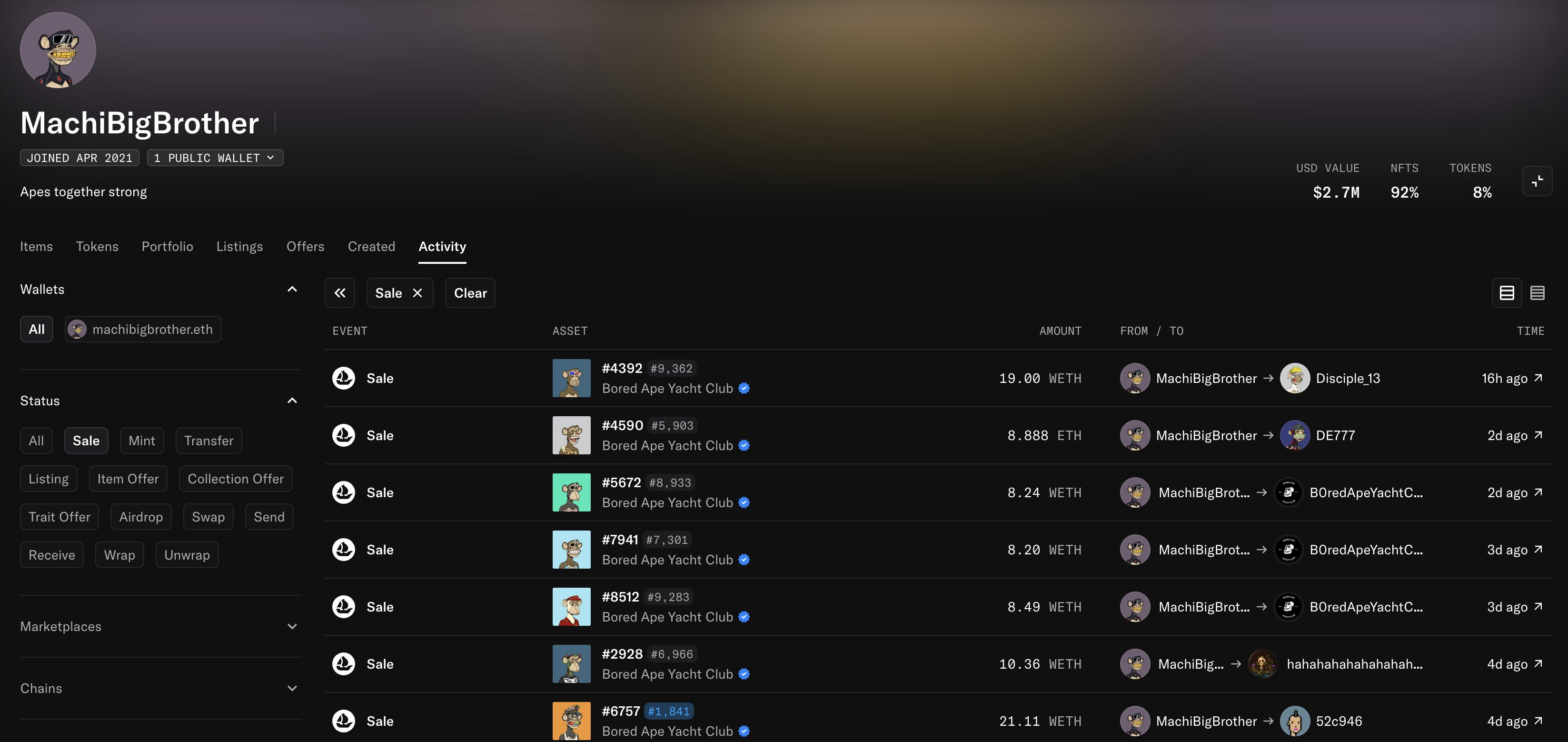

6 月 27 日,Lookonchain 监测称,台湾加密巨鲸黄立成(Machi Big Brother,麻吉大哥)在过去一个月内出售 34 枚 Bored Ape Yacht Club(BAYC) NFT,换得 326 枚 ETH(约 51.4 万美元),实际亏损 399 枚 ETH(约 63.1 万美元)。

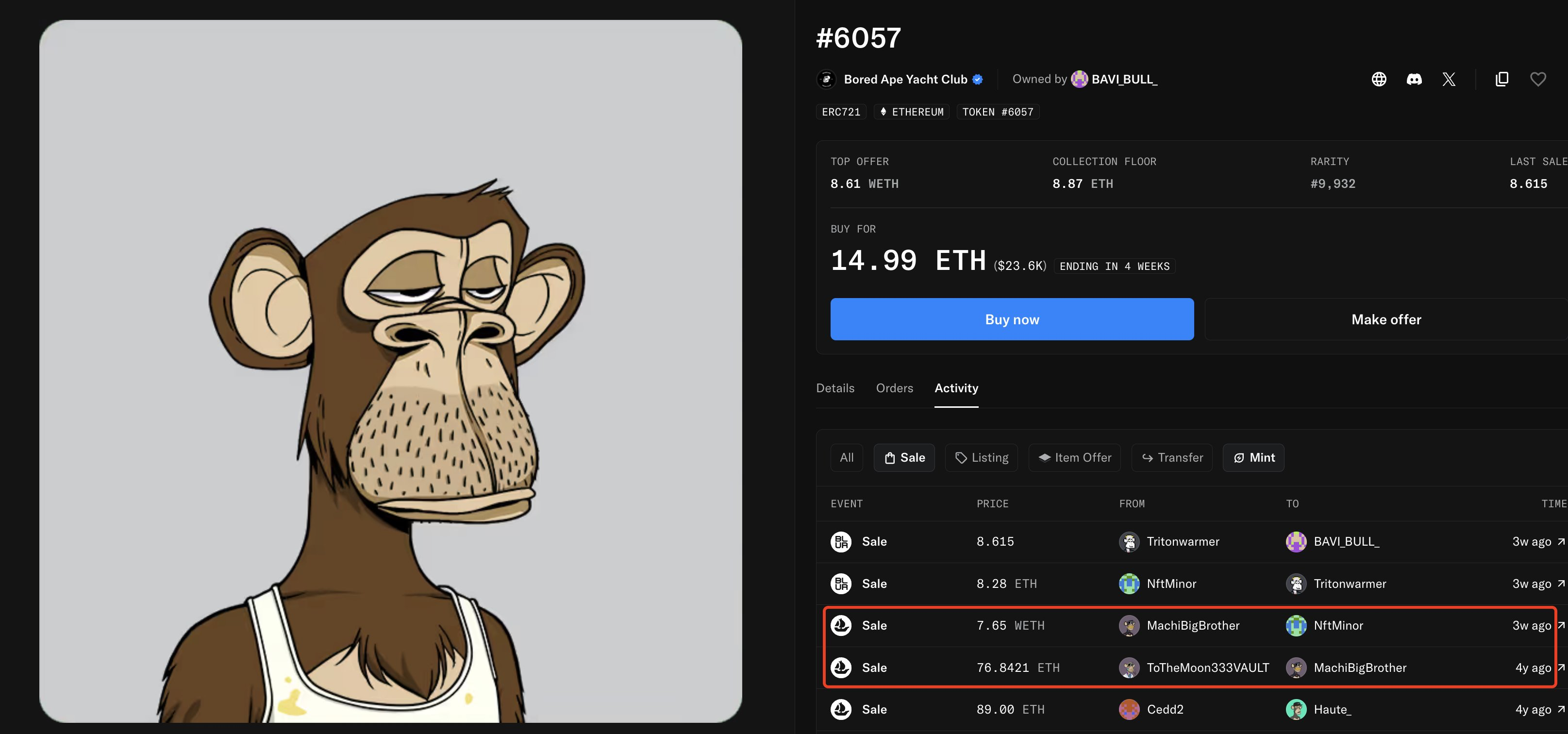

其中 Bored Ape #6057 四年前以 76.84 枚 ETH 购入,如今以 7.65 枚 ETH 售出,ETH 本位亏损达 90%。链上数据显示,这批 ETH 全部转入 Hyperliquid,用于补充其 ETH 多单保证金。

BAYC 成为最后一根输液管

黄立成卖猴的原因,就是合约账户的保证金已经撑不住了。

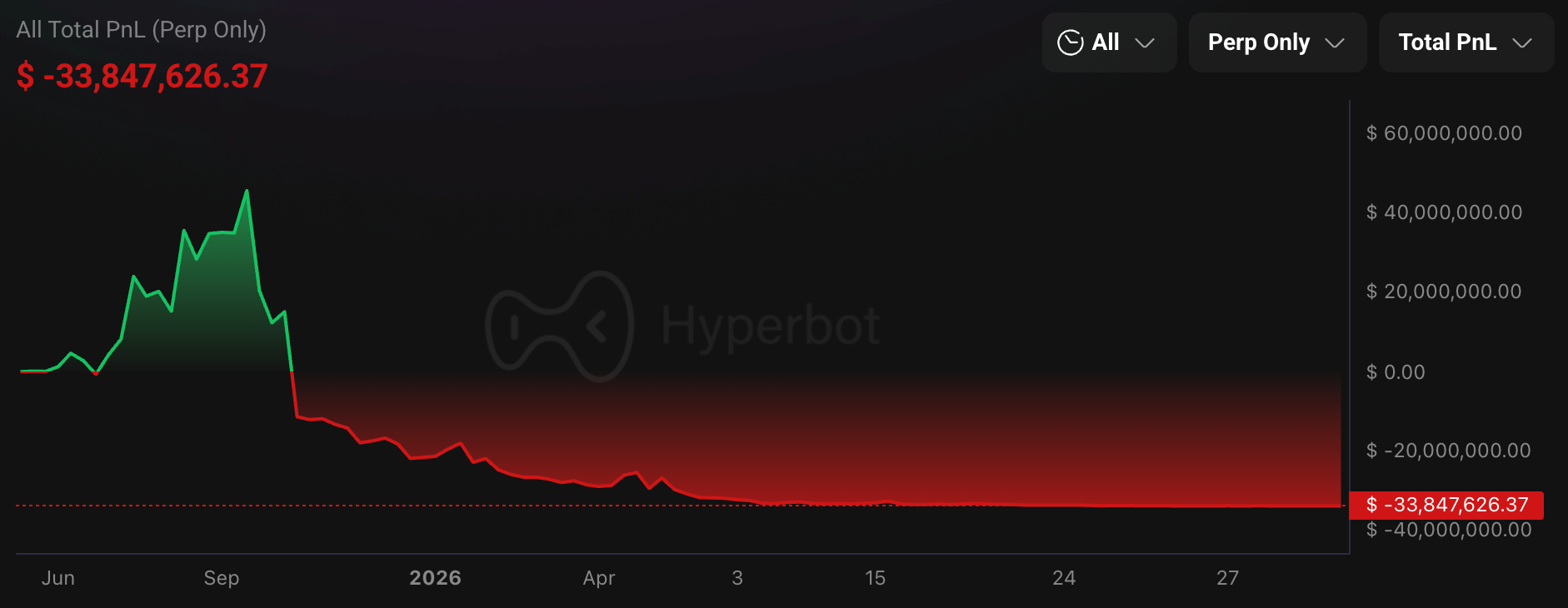

他从 2025 年 9 月开始在 Hyperliquid 上做多 ETH,彼时 ETH 报价约 4700 美元,典型操作是 25 至 40 倍杠杆。策略在初期表现亮眼,2025 年底至 2026 年初,账户一度录得 4566 万美元浮盈,他也因此在加密社区中获得了「链上巨鲸交易员」的新标签。

但 ETH 随后一路下跌至 1600 美元区间,浮盈全部回吐并转化为巨额实亏。据 HyperInsight 数据,截至 6 月 26 日,黄立成在 Hyperliquid 上的累计亏损已达 3385 万美元。若按过去一年的总交易损益计算,其亏损规模已超过 8000 万美元。

更能说明问题的是爆仓频率,截至 2026 年 3 月,黄立成已累计遭遇超过 335 次清算,被社区封为「爆仓之王」(King of Liquidations)。此后爆仓仍在持续,6 月 8 日,他在 8 小时内被连续清算 10 次,账户一度仅剩约 5.2 万美元;6 月 23 日 ETH 跌至 1607 美元,10 小时内再被清算 7 次。他的账户余额多次跌至几千美元的极端水平,2 月一度仅剩 8500 美元,但每次归零后都重新充值继续开多。

链上数据平台 Arkham 在 6 月 6 日曾特别指出,那是黄立成首次被清算后「没有立刻补入保证金」,引发社区猜测这场豪赌是否即将收场。但仅仅两天后他便再次入金,重新开出 ETH 多单。

当常规资金来源消耗殆尽,黄立成开始从 NFT 收藏中抽血。此前其还持有约 150 枚 BAYC,但按当前地板价(约 8.8 ETH)计算,剩下的 NFT 总价值约在 160 万美元左右,仅够支撑数轮高杠杆仓位的保证金。他曾在 2025 年底的一次访谈中表示,自己会「死扛 3000 万美元的亏损不卖」,坚定看多 ETH。半年过去,亏损早已超过这个数字,而曾经价值数千万美元的蓝筹 NFT 收藏,已经变成了合约账户的输液管。

6 月 26 日,他在 X 平台发帖:「We‘re going to need more Tom. 8 percent.(我们需要更多的汤姆。8%)」疑似喊话 Tom Lee 救市。

从猴子教父到爆仓之王

回溯黄立成的加密历程,他的起点远非普通散户。黄立成是华语嘻哈先驱 L.A. Boyz 创始成员,2015 年创办的直播平台 17 Media(M17)一度成为亚洲最大直播应用之一。2017 年牛市期间接触加密货币,同年在台湾区块链会议上结识以太坊创始人 Vitalik Buterin。2020 年参与创建 DeFi 协议 Cream Finance,该协议此后遭遇三次安全漏洞攻击,累计损失超过 1.92 亿美元。

真正让他在加密社区名声大噪的是 NFT,2021 年牛市中,黄立成以仅 0.08 ETH 的铸造价拿到数十只 BAYC,随后大举扫货,巅峰时期持有约 200 只 BAYC 和 100 多只 MAYC,钱包中 NFT 收藏总计约 3200 件,总价值超过 4000 万美元。

他将 BAYC 赠送给周杰伦等华语圈顶流明星,一手推动了无聊猿在亚洲市场的出圈传播,被社区称为「猴子教父」。那是 BAYC 地板价从 0.08 ETH 飙升至超过 100 ETH 的年代,黄立成的猴子持仓一度价值数千万美元。

但从 2023 年后,NFT 市场急速降温,黄立成在 Blur 平台的空投挖矿活动中大量接盘蓝筹 NFT,两天内扫入 71 只 BAYC 和 77 只 CryptoPunks,遭遇严重亏损。当年 4 月他宣布退出 NFT 市场。2024 年 7 月短暂回归,两周内再度买入 23 只 BAYC,但四个月内亏损超过 2000 万美元。此后他的注意力全面转移到 Hyperliquid 的永续合约上,开启了那场持续至今的高杠杆做多 ETH 的循环。

从铸造价 0.08 ETH 到巅峰超过 100 ETH,再到如今 7 至 10 ETH 的抛售价,BAYC 的价格曲线本身就是 NFT 周期最完整的注脚。而黄立成的个人轨迹与这条曲线高度重合:NFT 造就了他「猴子教父」的身份,也为他之后在合约赌桌上的连续加注提供了最初的本金。如今猴子正在被一只只卖掉,换成 ETH,换成保证金,再换成下一次清算通知。