Misconception1: "Running a node requires staking 32 ETH."

False. Anyone is free to sync their own self-verified copy of Ethereum (i.e. run a node). No ETH is required. Not before The Merge, not after The Merge, not ever.

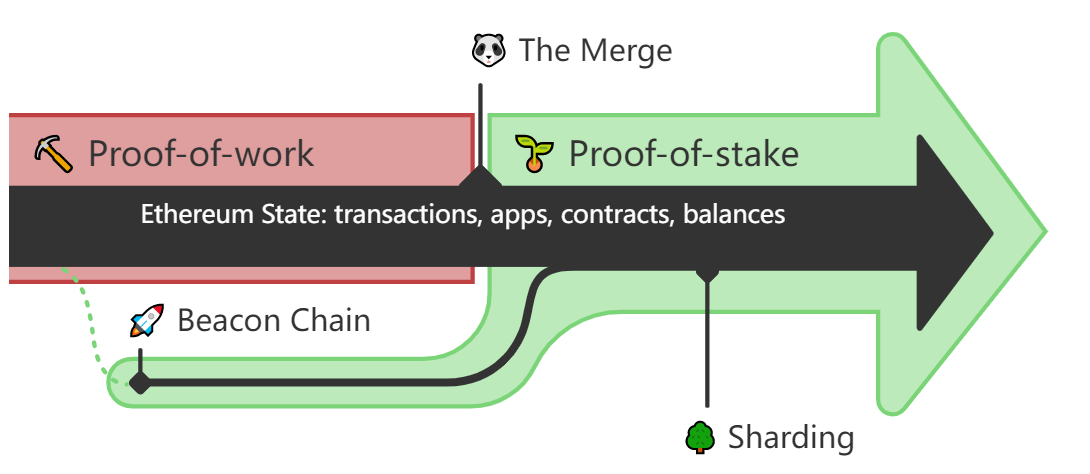

There are two types of Ethereum nodes: nodes that can propose blocks and nodes that don't.

Nodes that propose blocks are only a small number of the total nodes on Ethereum. This category includes mining nodes under proof-of-work (PoW) and validator nodes under proof-of-stake (PoS). This category requires committing economic resources (such as GPU hash power in proof-of-work or staked ETH in proof-of-stake) in exchange for the ability to occasionally propose the next block and earn protocol rewards.

The other nodes on the network (i.e. the majority) are not required to commit any economic resources beyond a consumer-grade computer with 1-2 TB of available storage and an internet connection. These nodes do not propose blocks, but they still serve a critical role in securing the network by holding all block proposers accountable by listening for new blocks and verifying their validity on arrival according to the network consensus rules. If the block is valid, the node continues propagating it through the network. If the block is invalid for whatever reason, the node software will disregard it as invalid and stop its propagation.

Running a non-block-producing node is possible for anyone under either consensus mechanism (proof-of-work or proof-of-stake); it is strongly encouraged for all users if they have the means. Running a node is immensely valuable for Ethereum and gives added benefits to any individual running one, such as improved security, privacy and censorship resistance.

The ability for anyone to run their own node is absolutely essential to maintaining the decentralization of the Ethereum network.

More on running your own node

Misconception2: "The Merge will reduce gas fees."

False. The Merge is a change of consensus mechanism, not an expansion of network capacity, and will not result in lower gas fees.

Gas fees are a product of network demand relative to the capacity of the network. The Merge deprecates the use of proof-of-work, transitioning to proof-of-stake for consensus, but does not significantly change any parameters that directly influence network capacity or throughput.

With a rollup-centric roadmap, efforts are being focused on scaling user activity at layer 2, while enabling layer 1 Mainnet as a secure decentralized settlement layer optimized for rollup data storage to help make rollup transactions exponentially cheaper. The transition to proof-of-stake is a critical precursor to realizing this. More on gas and fees.

Misconception3: "Transactions will be noticeably faster after The Merge."

False. Though some slight changes exist, transaction speed will mostly remain the same on layer 1.

A transaction's "speed" can be measured in a few ways, including time to be included in a block and time to finalization. Both of these changes slightly, but not in a way that users will notice.

Historically, on proof-of-work, the target was to have a new block every ~13.3 seconds. On the Beacon Chain, slots occur precisely every 12 seconds, each of which is an opportunity for a validator to publish a block. Most slots have blocks, but not necessarily all (i.e. a validator is offline). On proof-of-stake blocks will be produced ~10% more frequently than on proof-of-work. This is a fairly insignificant change and is unlikely to be noticed by users.

Proof-of-stake introduces the transaction finality concept that did not previously exist. On proof-of-work, the ability to reverse a block gets exponentially more difficult with every passing block mined on top of a transaction, but it never quite reaches zero. Under proof-of-stake, blocks are bundled into epochs (6.4 minute spans of time containing 32 chances for blocks) which validators vote on. When an epoch ends, validators vote on whether to consider the epoch 'justified'. If validators agree to justify the epoch, it gets finalized in the next epoch. Undoing finalized transactions is economically unviable as it would require obtaining and burning over one-third of the total staked ETH.

Many dapps require a number of proof-of-work block confirmations that take a period of time on par with how long proof-of-stake finality takes. Finality can offer additional security guarantees, but will not significantly speed up transactions.

Misconception4: "You can withdraw staked ETH once The Merge occurs."

False. Staking withdrawals are not yet enabled with The Merge. The following Shanghai upgrade will enable staking withdrawals.

Staked ETH, staking rewards to date, and newly issued ETH immediately after The Merge will still be locked on the Beacon Chain without the ability to withdraw.

Withdrawals are planned for the Shanghai upgrade, the next major upgrade following The Merge. This means that newly issued ETH, though accumulating on the Beacon Chain, will remain locked and illiquid for at least 6-12 months following The Merge.

Misconception5: "Validators will not receive any liquid ETH rewards til the Shanghai upgrade when withdrawals are enabled."

False. Fee tips/MEV will be credited to a Mainnet account controlled by the validator, available immediately.

This may seem counterintuitive to the above note that withdrawals are not enabled til the Shanghai upgrade, but validators WILL have immediate access to the fee rewards/MEV earned during block proposals.

The protocol issues ETH as a reward to validators for contributing to consensus. This Beacon Chain accounts for the newly issued ETH, where a validator has a unique address that holds its staked ETH and protocol rewards. This ETH is locked until Shanghai.

ETH on the execution layer (Ethereum Mainnet as we know it today) is accounted for separately from the consensus layer. When users execute transactions on Ethereum Mainnet, ETH must be paid to cover the gas, including a tip to the validator. This ETH is already on the execution layer, is NOT being newly issued by the protocol, and is available to the validator immediately (given a proper fee recipient address is provided to the client software).

Misconception6: "When withdrawals are enabled, stakers will all exit at once."

False. Validator exits are rate limited for security reasons.

After the Shanghai upgrade enables withdrawals, all validators will be incentivized to withdraw their staking balance above 32 ETH, as these funds do not add to yield and are otherwise locked. Depending on the APR (determined by total ETH staked), they may be incentivized to exit their validator(s) to reclaim their entire balance or potentially stake even more using their rewards to earn more yield.

An important caveat here, full validator exits are rate limited by the protocol, so only six validators may exit per epoch (every 6.4 minutes, so 1350 per day, or only ~43,200 ETH per day out of over 10 million ETH staked). This rate limit adjusts depending on the total ETH staked and prevents a mass exodus of funds. Furthermore, it prevents a potential attacker from using their stake to commit a slashable offense and exiting their entire staking balance in the same epoch before the protocol can enforce the slashing penalty.

The APR is intentionally dynamic, allowing a market of stakers to balance how much they're willing to be paid to help secure the network. When withdrawals are enabled, if the rate is too low, then validators will exit at a rate limited by the protocol. Gradually this will raise the APR for everyone who remains, attracting new or returning stakers yet again.

Misconception7: "Staking APR is expected to triple after The Merge."

False. More up-to-date estimations predict closer to a 50% increase in APR post-merge, not a 200% increase.

The APR for stakers is expected to increase post-merge. To understand by how much, it is important to recognize where this increase in APR is coming from. This does not come from an increase in protocol ETH issuance (ETH issuance after The Merge is decreasing by ~90%), but is instead a reallocation of transaction fees that will start going to validators instead of miners.

This will be a new separate source of revenue for validators when they propose blocks. As you can imagine, the amount of fees a validator receives is proportional to network activity at the time of their proposed block. The more fees being paid by users, the more fees validators will receive.

Looking at recent blockchain activity, approximately 10% of all gas fees being paid are currently going to miners in the form of a tip, while the rest is burnt. Outdated predictions estimated this percentage to be much higher, and was calculated when network usage was at all time highs. Extrapolating the 10% number to average recent network activity, it is estimated that the APR for staking will increase to ~7%, approximately 50% higher than the base issuance APR (as of June 2022).

Misconception8: "The Merge will result in downtime of the chain."

False. The Merge upgrade is designed to transition to proof-of-stake with zero downtime.

An immense amount of work has been put into making sure the transition to proof-of-stake does not disrupt the network or its users.

The Merge is like changing an engine on a rocketship mid-flight and is designed to be performed without needing to pause anything during the switch. The Merge will be triggered by terminal total difficulty (TTD), which is a cumulative measure of the total mining power that has gone into building the chain. When the time comes, and this criterion is met, blocks will go from being built using proof-of-work in one block to being built by proof-of-stake in the next.

Ethereum does not have downtime.