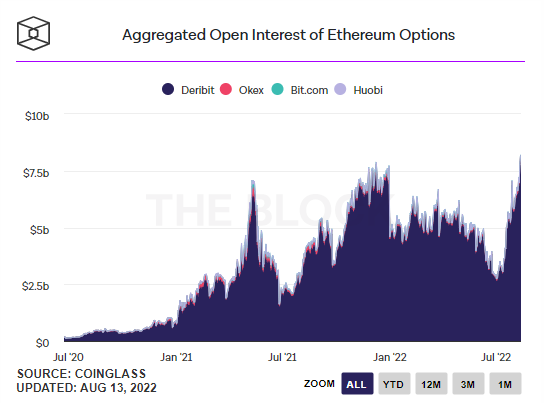

Open interest of ether options has hit a fresh all-time high.

Per The Block's data dashboard, August 12 saw open interest hit $8.11 billion—a figure that's nearly three times higher than where it stood a month ago.

The surge in open interest of ether options appears to be tied to the emergence of new, more complex strategies, among traders positioning themselves ahead of Ethereum's transition from proof-of-work to proof-of-stake, according to hedge fund LedgerPrime. That transition is expected to finalize next month.

In a Telegram message to counter-parties, LedgerPrime wrote: "The Long Call Butterfly, which has been the most traded structure for ETH over the last month, has moved this week to the second position, with the Bull Call Spread taking the lead at a volume of 160K."

By signing-up you agree to our Terms of Service and Privacy Policy

Meanwhile, open interest of bitcoin options has been slumping for months, currently sitting around $5.5 billion.

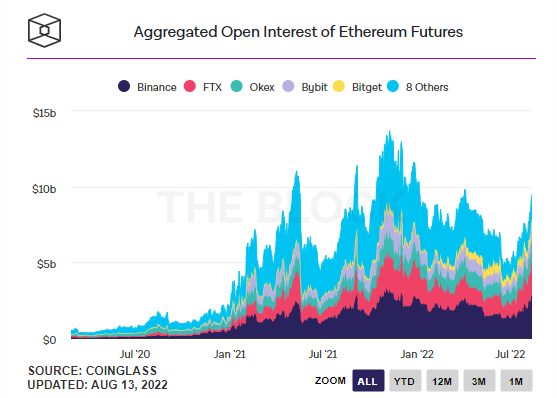

Ether itself is up over 16% on the week amid a broad rally in cryptocurrencies. Open interest of ether futures is also on the rise, approaching levels not seen since early April and topping $9.15 billion.