Klaytn 正在为 Klaytn 2.0 做准备,它包括扩展 L2 解决方案、元宇宙文件、创建 DAO 的 DAO (工具)以及更多的基础设施。

Klaytn 是韩国的(非)官方公链,于 2019 年推出,它是:

OpenSea 支持的 4 个区块链之一;

TVL 在 DeFi 中排名第 14 位;

$KLAY 按市值排名第 66 位。

然而,韩国以外的人很少听说过它,在这次的 KBW 中,让我们来一起了解它。

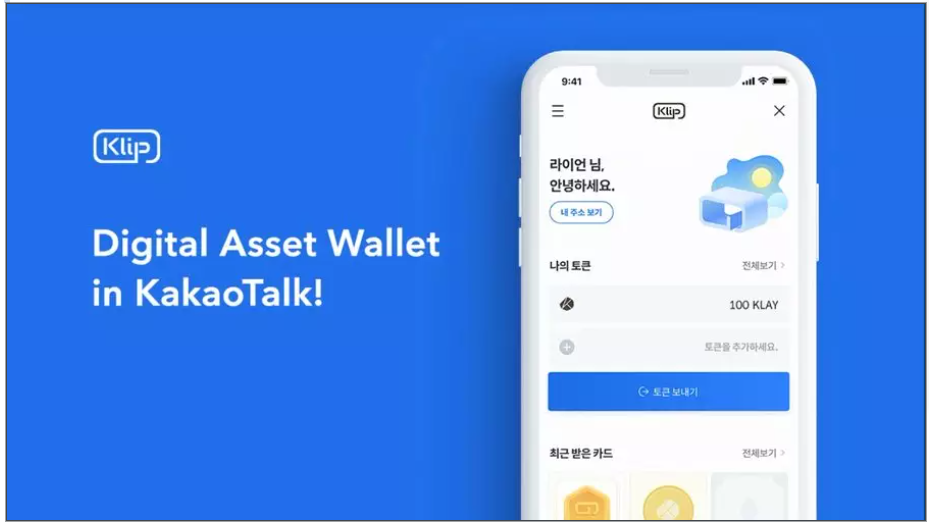

Klatyn 得到了韩国的「Facebook」—— Kakao 的支持。Kakao 是韩国使用最多的短信应用,拥有 5300 万活跃用户。而这些用户可以在 Kakao 应用中使用 Klaytn 的区块链钱包。可以想像,在 Facebook 的 Messenger 或 WhatsApp 中拥有一个 Ethereum 钱包,会给 Web3 带来多大的流量。

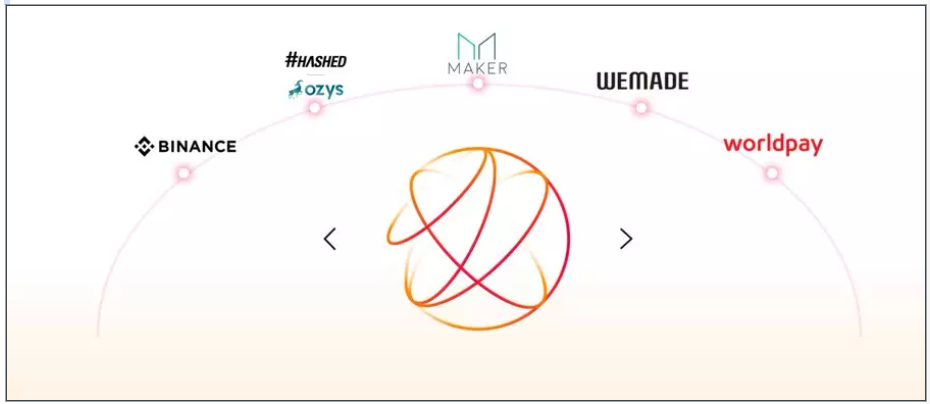

Klatyn 最初是以太坊的一个分叉,它通过治理委员会(GC)专注于可扩展性和性能。它的运营商是 DAO 和跨国组织,如:

LG;

MakerDAO;

Binance;

Hashed/Ozys;

Kakao 等等。

多亏了那些坚定的支持者,Klaytn 才能成为了第二个集成在 OpenSea 上 的公链,甚至在 Polygon 或 Solana 之前。正如他们在 KBW 的团队成员告诉我的那样,他们在 OpenSea 的早期就接触了 OpenSea,当时 NFT 板块还没有那么火热。

Klaytn 的 DeFi 生态同样在 4 月份遭受到了打击,TVL 从 12 亿美元下降到目前的 4.15 亿美元。当前,其链上最受欢迎的 dApp 是:

DEX——KLAYswap 和 Kokonutswap;

借贷市场 Klapfinance;

流动性 KLAY 质押;

虽然 KlaySwap 占领了其 50% 的 TVL。

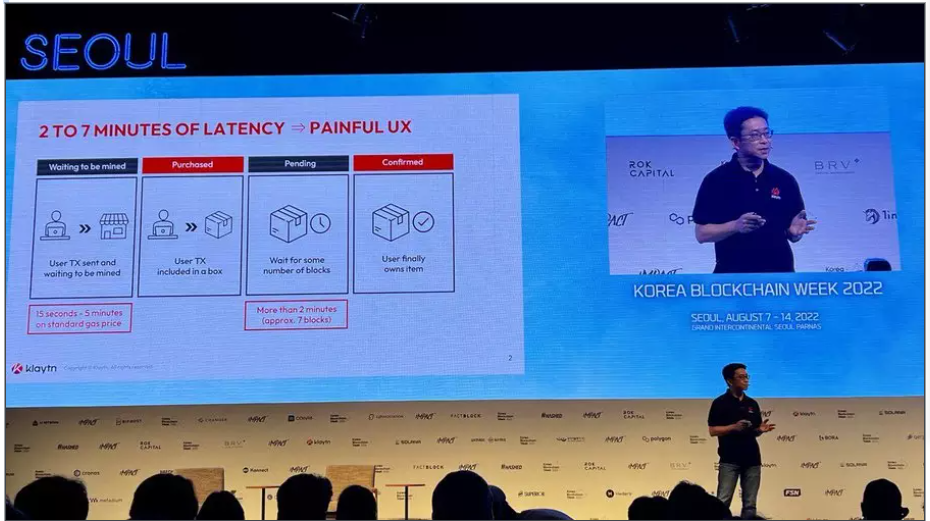

考虑到这一点,Klaytn 的第一目标是元宇宙。Klaytn 首席 Sangmin SEO 在 KBW 上介绍了他对 Klaytn 在加密货币生态系统中的愿景和定位。

我参加了他的演讲,这是他说的内容:

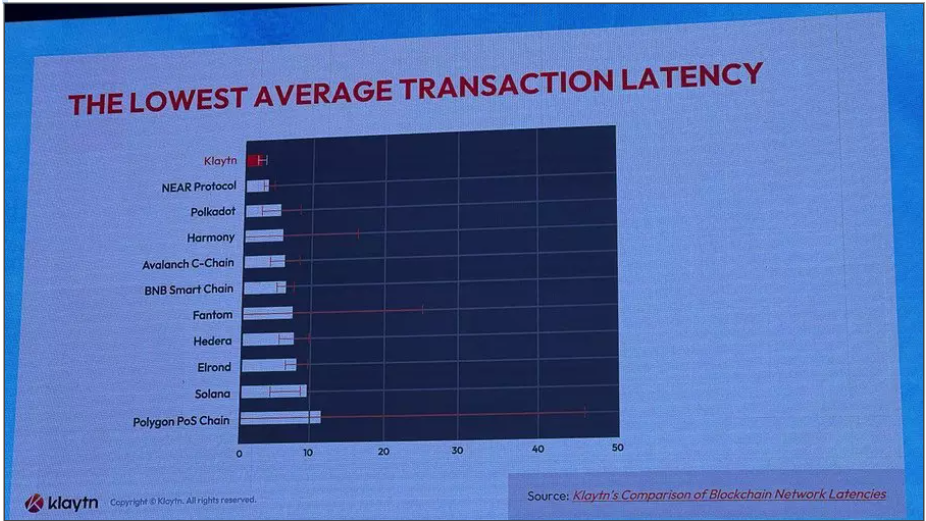

忘记 TPS。区块链上的不同元宇宙用户体验需要低延迟,交易延迟=交易被纳入区块的时间 - 交易被提交给网络的时间,这是一个输入和接收输出之间的时间延迟。

根据 Klaytn 自己的研究,Klaytn 的交易延迟最低,平均为 2.1 秒。 其次是 NEAR 在 2 到 5 秒之间,Solana 在 2 到 30 秒之间,而 Polygon 平均为 10.9 秒,而且还经常超过 100 秒。

更重要的是,Klaytn 拥有 1 秒的区块生成时间和即时的最终确认时间。作为比较,$ETH 需要 14 次网络确认才能被纳入区块链上的一个区块中。

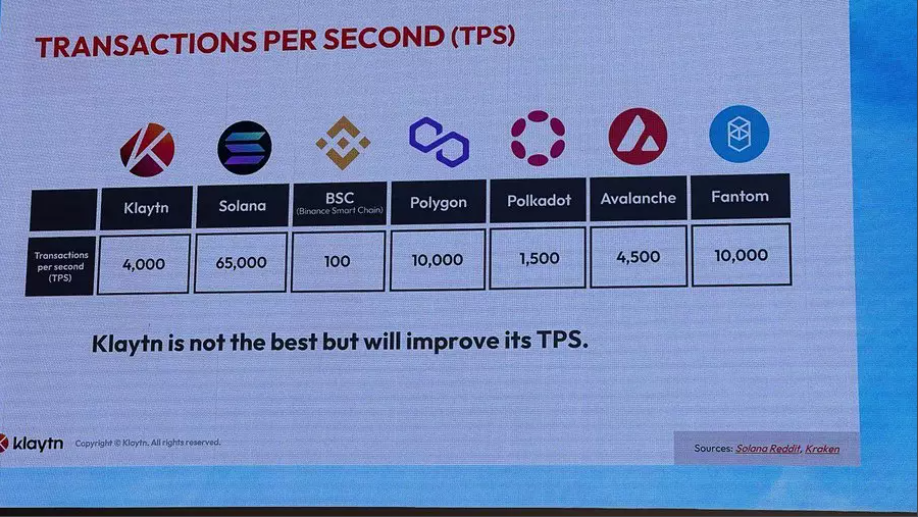

不过,如果按每秒交易量(TPS)计算,它并没有使 Klaytn 成为最快的区块链。在 4k TPS 时,它远远落后于 Polygon、Fantom 或 Solana,但 Klaytn 正计划对此进行改进。

最后,Klaytn 正在为 Klaytn 2.0 做准备,它包括扩展 L2 解决方案、元宇宙文件、创建 DAO 的 DAO (工具)以及更多的基础设施。