1. BTC volume stagflation

BTC's 4-hour K-line chart hours. With the price adjustment, BTC, which currently maintains a high-volume state, has continued its decline for several trading days. Since July 20, BTC has fallen below the middle rail of the brin line after falling back from the high US $24200. BTC's short-term decline expanded to 12.5%, and the Bollinger line expansion trend continued. In the case of high trading volume, the possibility of BTC falling beyond expectations has significantly increased.

Recently, BTC has accumulated more chips below US $24000. The large volume of spot BTC transactions and the increase in the number of online transfers have increased the concentration of chips in this price range. In terms of support, we are concerned about the possibility that BTC will rebound at US $19000 and US $20000.

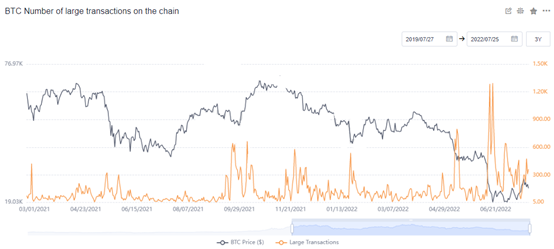

2. BTC high-level operation of large transactions

The number of large transactions with more than 500 BTCs is running at a high level, and the current value has frequently reached 500, indicating that the main force is highly active. The activity of the main players in the low price zone has increased, which represents the growth trend of the number of low turnover BTCs. A large number of BTCs transfer money in the low price zone, and it is difficult for BTCs to get out of the price range below $24000 at present. However, after the change of hands is completed, considering that the volatility of BTC price rebounded on July 25, it seems to be preparing for a downward break. In the short term, we can prepare for emergencies, and the important $19000 may be used as the key support point.

3. BTC estimated high leverage operation

BTC estimates that the leverage ratio is running at a high level, and there has been no significant growth since June. Nevertheless, judging from the growth trend of leverage ratio, it is still the highest level in history. It is estimated that the high leverage ratio means that the stock of BTC in the exchange decreases, the trading leverage ratio of investors is high, and BTC still has high volatility potential.

Numerically, the leverage ratio was estimated to be around 0.315 on July 24, with a significant increase of 43% during the year. In terms of trading, pay attention to the intra day amplitude performance of BTC, and pay attention to the expectation of high-intensity fluctuations caused by price changes.

4. Eth continuous adjustment signal

The daily K-line chart of eth shows that after the price fell from the high platform, the trading volume maintained a shrinking trend. At present, the trading volume is close to falling below the equivalent line, and the ETH price is close to the brin line medium rail. According to the price operation rhythm, ETH implementation will seek the support of $1348 corresponding to the brin line medium rail, so as to further verify the price long and short rhythm.

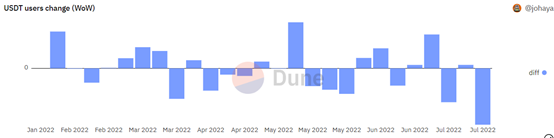

5. Decrease in stable currency users

The decreasing trend of stable currency users continued, especially the number of users of usdt with the highest market value continued to decline, and the decline was significantly increased. The data showed that the number of usdt users fell by 80884 on July 25, the largest decline in the year. Judging from the downward trend of usdt users, investors' trading enthusiasm for the current mainstream currencies is obviously at a low level. The decline in the number of users means that more investors are less willing to copy the bottom of the market. Although mainstream currencies such as BTC and eth retreated, it may be difficult to support the short-term rebound, so the recent trend is not optimistic.