昨日,2025年8月25日,是足以被铭记的一天。它并非无声的下跌,而是一场伴随着巨响的崩塌。根据Coinglass的精确数据,在过去24小时内,加密市场全网爆仓总额高达 9.43亿美元。

这场风暴的指向性异常明确:在崩塌中被碾碎的多头头寸高达 8.33亿美元,而空头爆仓仅1.1亿美元。以太坊($3.22亿)和比特币($2.68亿)成为了这场清算盛宴的中心。正如知名分析账号BTC Archive所指出的,这是自2024年12月以来最大规模的多仓清算事件。对于每一个身处其中的杠杆交易者而言,这组冰冷的数据背后,是切肤之痛与孤独的煎熬。

然而,当我们把镜头拉远,从散户的爆仓通知切换到上市公司的资产负债表时,一幅更为波澜壮阔的“亏损画卷”正在展开。在我们为账户归零而绝望时,那些将比特币、以太坊作为核心战略储备的巨头们,正在以“亿”为单位,承受着账面价值的剧烈回撤。

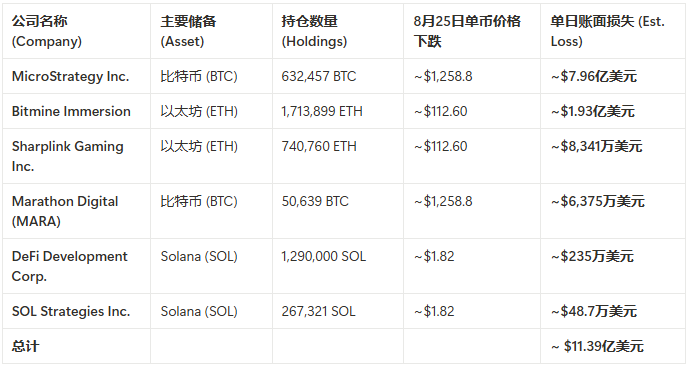

单日账面亏损排行榜:巨头们的“失血”报告

在我们深入探讨结构性风险之前,让我们先用最直观的数据,来看看这些加密储备巨头在8月25日这一天里,究竟“流了多少血”。根据各公司最新披露的持仓数据及当日行情计算,其单日账面损失如下:

注:持仓数据基于各公司截至2025年8月的最新公开报告。价格变动基于2025年8月25日的开盘价与收盘价计算,存在细微误差。

是的,你没看错。仅仅一天之内,仅我们统计的这几家代表性公司,其加密资产的账面价值就合计蒸发了超过 11亿美元。其中,比特币最大的“布道者”MicroStrategy一家就承担了近8亿美元的账面亏损,这个数字已经超过了散户爆仓的总和。

看到这里,你账户里的那点损失,是否瞬间有了一丝别样的“慰藉”?但真正的重点在于下一个问题。

价值百亿美金的问题:他们会被“爆仓”吗?

这是散户与巨头最核心的区别,也是理解加密市场结构的关键。答案是:几乎不可能,因为游戏规则完全不同。

散户的“爆仓”通常源于 高杠杆衍生品交易。当交易者使用借来的资金(杠杆)在交易所开立合约头寸时,他们需要提供保证金。一旦市场价格朝不利方向剧烈波动,导致保证金不足以覆盖潜在亏损时,交易所的清算引擎会强制平仓,这便是“爆仓”。

而这些上市公司的储备结构,与此截然不同:

现货持有,而非合约杠杆 (Spot Holdings, Not Leverage)

绝大多数情况下,无论是MicroStrategy的比特币,还是Bitmine的以太坊,它们持有的都是现货资产,直接存储在冷钱包或由合规托管机构保管。它们拥有这些加密货币的100%所有权。只要他们不主动卖出,价格的短期波动只会影响财务报表上的“账面价值”(Paper Value),而不会触发任何保证金追缴或强制平仓。

低成本的长期债务融资 (Long-term, Low-cost Debt)

以MicroStrategy为例,其购买比特币的资金主要来源于发行可转换票据和公司债券。这是一种企业级的、长期的、相对低利率的融资行为。其偿付义务是固定的利息和到期的本金,与比特币的短期价格波动没有直接关联。

它们的风险点不在于交易所的清算线,而在于一个极其遥远的比特币价格——远低于其平均持仓成本(约$35,000/BTC)。只有当币价跌破某个临界点,导致其无法通过再融资或经营活动来偿还到期债务时,才会出现真正的危机。而目前,它们仍然拥有巨大的利润缓冲。

矿工的特殊地位 (The Miner's Advantage)

对于Marathon Digital (MARA)这样的矿企而言,情况更为特殊。它们不仅是比特币的持有者,更是比特币的生产者。只要比特币的市场价格高于他们的“挖矿成本”(包括电力、设备折旧、运营等),他们的业务就在持续产生正向现金流。他们持有的比特币更多是作为战略储备和资产负债表的一部分,其核心业务的健康度与币价和挖矿难度直接相关,而非杠杆风险。

给散户的一剂“结构性安慰剂”

在加密世界这场残酷的生存游戏中,没有人能对剧烈的波动免疫。巨鲸们流的“血”在数量上远超常人,但性质却截然不同。他们的损失是战略性的账面回撤,而许多散户的损失,则是毁灭性的现金清零——一场载入史册的清算事件再次证明了这一点。

理解这一结构性差异至关重要。它告诉我们,不要用衍生品交易的短期、高危逻辑去揣测巨头们的长期现货策略。他们是在进行一场基于宏观判断的、长达数年的资产配置,而我们中的许多人,则是在玩一场以分钟计的概率游戏。

因此,下一次当你看到市场满目疮痍时,不妨想一想MicroStrategy那缩水了近8亿美元的资产负债表。你的痛苦并非独一无二,整个市场都在一同经受洗礼。但更重要的是,要从巨头们的策略中得到启发:降低杠杆、着眼长远、理解你所持有的资产的真实风险结构。

或许,这才是这场血色风暴中,最值得散户带走的、最有价值的“安慰剂”。