作者:Stablecoin Blueprint

编译:深潮 TechFlow

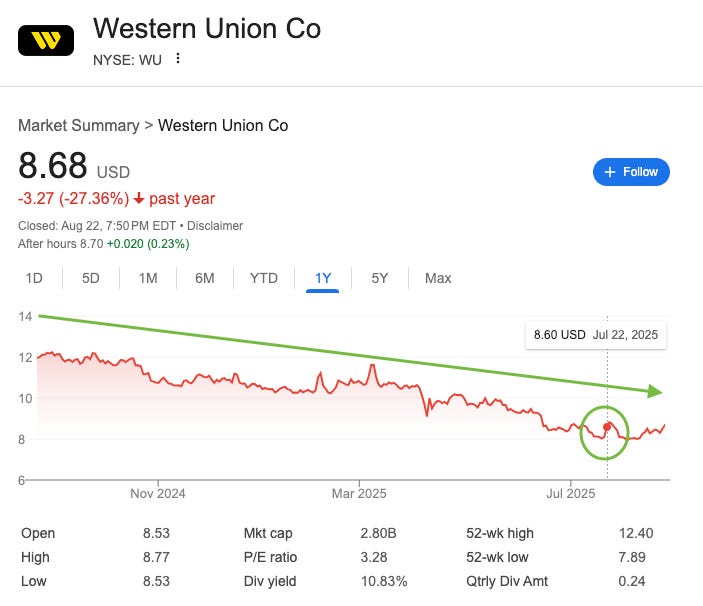

7 月 22 日,西联汇款(Western Union)似乎迎来了久违的曙光。在其 CEO 于彭博采访中提及公司将深入探索稳定币领域后,这家传统支付巨头的股价迅速飙升,当日收盘上涨近 10%,吸引了投资者多年未见的“抄底”热潮。然而,这份希望转瞬即逝。一周后,西联汇款发布的财报再次未达分析师预期,股价随即回落至低点,早前的涨幅被彻底抹去。

这一短暂的市场兴奋不仅关乎西联汇款,还折射出华尔街对稳定币的全新偏好。在标志性天才法案通过以及稳定币发行商 Circle 股价惊人上涨五倍的背景下,投资者几乎形成了一种条件反射:听到“稳定币”便蜂拥而至。但这种对“稳定币”的追捧更多是对流行词的误解,而非真正的商业战略。稳定币无法拯救西联汇款的核心业务,但如果该公司能够采取正确的行动,它或许能借此开启全新的未来。

巨人的衰落

成立于 1851 年的西联汇款(Western Union),曾是全球汇款领域的巨头,但其财务表现却讲述了一个巨人在新时代挣扎的故事。近年来,华尔街将这家世界最大汇款公司视为逐渐消融的“冰块”,而数据也印证了这一观点:自 2021 年以来,公司收入从超过 50 亿美元缩减至预计 2025 年的 41 亿美元,同时市场份额不断被数字化优先的竞争对手蚕食。这一衰退同样反映在其股价上——从 2021 年的高点 26 美元跌至如今徘徊在 8 至 9 美元之间。

支撑这家拥有 172 年历史巨头的基础力量——其全球近 40 万家实体代理点的网络——如今却成为其最大的结构性弱点。这种依赖代理商的模式成本高昂,占西联汇款服务成本的约 60%。这一网络主要服务于一个关键客户群体:依赖现金且通常无法获得银行服务的移民工人。数十年来,这一模式曾是西联汇款的护城河。

然而,随着全球数字化进程加速,这一依赖现金的客户群体正处于长期结构性衰退中。而在数字化领域——未来的战场——西联汇款的表现则远逊于竞争对手。在上季度,西联汇款品牌的数字收入仅增长了 6%,而竞争对手如 Wise 和 Remitly 的增长率却达到了 20%-30% 甚至更高。曾经是汇款领域无可争议的王者,如今却在竞争对手的数字领域节节败退。

迷人却有缺陷的解决方案

表面上看,西联汇款(Western Union)提出的稳定币计划似乎颇具全面性。在最近的财报电话会议中,公司阐述了四项关键战略:

-

改善自身的财务管理;

-

通过稳定币实现全球支付;

-

在数字钱包中提供买卖和持有功能;

-

最为重要的是,将其全球网络作为加密生态系统的出入口。

然而,公司目前的重点显然集中在第一项战略上。正如 CEO Devin McGranahan 所言,“我们大部分时间和精力都放在这一领域”,即通过稳定币解决后台运营效率问题。

这一策略的吸引力毋庸置疑。McGranahan 强调稳定币可以“显著提升结算速度,并减少合作伙伴所需的预付款金额”。他举例提到,印度近期发生的一次周末流动性紧张事件导致支付延迟,而稳定币可以实现实时补充流动性,全天候提供服务,从而大幅改善客户体验。

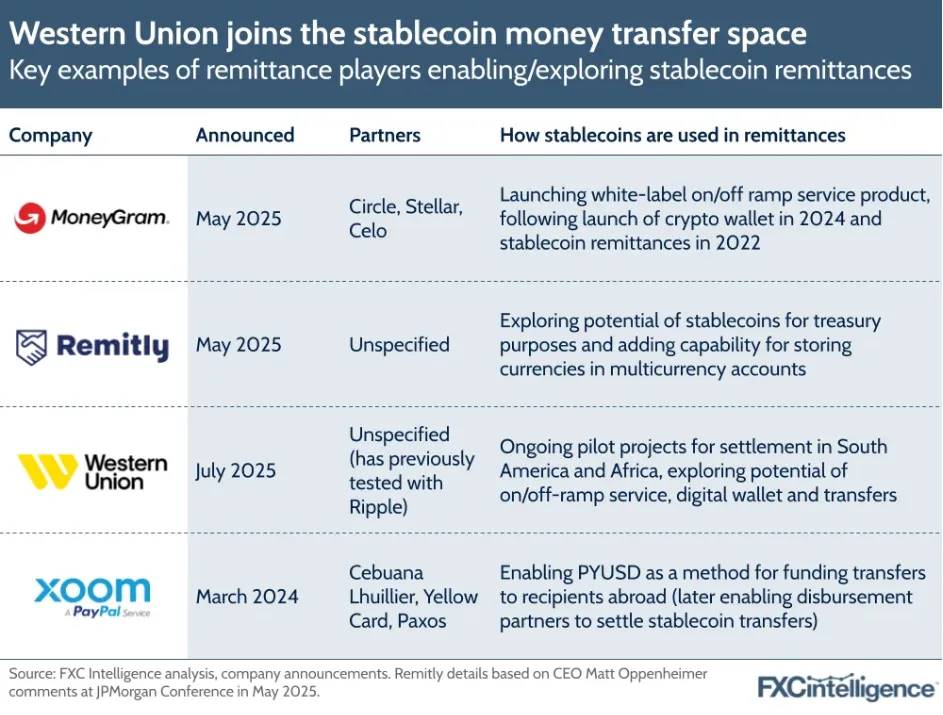

然而,尽管通过稳定币优化财务管理是一个明智的目标,它却无法带来长期的竞争优势。西联汇款的主要竞争对手,例如 MoneyGram 和 Remitly,已经在实施类似的基于稳定币的结算策略。任何成本节约都可能会在竞争压力下被削弱,尤其是在那些本身运营成本较低的数字化企业面前。这使得这一潜在创新沦为一种“商业运营成本”,无法扭转公司目前的结构性衰退。

真正的机遇:通向数字经济的现金桥梁

西联汇款(Western Union)的未来并不在于试图在数字领域追赶竞争对手,而在于成为一个他们无法取代的角色:全球主要的现金到稳定币的接入层。公司应充分利用其拥有的 40 万家实体代理点,将其视为最重要的战略资产。通过强化这一网络并依托其备受信赖的品牌,西联汇款有望解决一项关键的金融基础设施问题:在实体现金和全球数字经济之间提供无缝的连接,而这项服务正是许多新兴市场迫切需要的。

这一战略转型可以通过两种方式来实现。首先,自有流量。

西联汇款可以将现金到稳定币的转换功能直接整合到其备受好评的移动应用中。用户可以走进一家值得信赖的西联汇款代理点,交付波动性较大的本地货币,并在几分钟内将美元稳定币存入自己的数字钱包。这对于那些希望通过美元稳定币保护财富的用户来说,尤其是生活在货币波动较大的地区,是一个极具吸引力的解决方案。

第二种更强大的方法是通过平台流量。

更具潜力的方式是通过 API 将其代理网络开放给第三方钱包和金融科技公司。这些合作伙伴可以直接在其应用中嵌入“使用西联汇款支付”或“通过西联汇款提现”的按钮。市场对此的需求已经显现出来。McGranahan 在公司财报电话会议上透露,他们对入金和出金服务的“意外高需求量”感到惊喜。这种方式将西联汇款从一个封闭的汇款服务转变为开放的基础设施,成为快速增长的数字生态系统与实体世界之间的关键“最后一英里”连接。

仅通过入金和出金服务,西联汇款便可实现可观的财务回报。根据当前的手续费率和代理经济模型(考虑其在现金交易中的定价能力),仅 10 亿美元的入/出金交易量就可能带来约 8000 万美元的营业利润,这对公司目前约8亿美元的总利润来说是一个显著的提升。作为对比,数字竞品 Remitly 在最近一个季度的交易量相较去年增加了 50 亿美元。

除了交易费用外,西联汇款通过其数字钱包切入点,还能提供更多金融服务,例如在线消费的借记卡、信贷产品,以及储蓄和投资服务。西联汇款甚至正在考虑发行自己的稳定币,其数字钱包与广泛的现金入/出金网络将构成一个极具吸引力的服务组合和便捷的分发渠道。更重要的是,与西方消费者不同,这些服务的目标用户对利率的敏感度较低,这可能使西联汇款能够保留更多的收益。

这些新功能将从根本上重新定义西联汇款代理的角色。代理点将不再只是一个领取一次性汇款的场所,而是成为数字时代的高效银行网点。对于数百万未被银行覆盖或银行服务不足的人群来说,西联汇款的本地代理将成为通向全球数字钱包的实体桥梁,最终兑现“为未被银行服务的人群提供银行服务”的承诺。

必要的转型,充满风险

这一战略转型充满挑战,从一家拥有 172 年历史的公司所面临的巨大执行风险,到现金使用的长期下降以及非正式 P2P 网络的威胁。然而,正是其核心业务的结构性衰退,使得这一转型显得尤为必要。

西联汇款在捍卫传统业务的同时,迫切需要通过入金/出金战略为公司注入新的增长动力。这一策略不仅让公司更深入地参与快速扩张的数字资产经济,还凭借其全球实体网络这一强大的差异化优势,为其赢得了宝贵时间,以成为未来不可或缺的现金桥梁——前提是能够成功执行。

西联汇款近期宣布以 5 亿美元收购专注于拉美地区现金汇款业务的 Intermex,这表明公司更倾向于通过整合衰退业务的协同效应,并将低成本获取的用户转化为数字用户。虽然收购可能会耗费大量时间和精力,成为阻碍西联汇款转型的另一大风险,但新增的零售网点也可能成为战略资产,与其未来作为现金桥梁的潜在角色相契合。

结论

西联汇款的未来无法通过新技术对旧商业模式的微调来保障。如今,战略选择已然明晰:要么继续以防守姿态在数字优先的竞争者设定的规则下苦战;要么果断转型,成为连接实体世界与快速发展的数字资产经济的不可或缺的现金桥梁。稳定币无法拯救传统汇款经济,但它们是打开未来平台经济大门的关键。一条路引向优雅的落幕;另一条路,则通往存在的崭新意义。