По словам Адама Ливингстона, автора книги «Эпоха биткоина и Великая жатва», правительство США может закупить больше биткоинов для стратегического резерва США, направляя часть профицита от пошлин на приобретение BTC.

Также он советует использовать безопасное географически распределенное холодное хранение с мультиподписью, подтверждение наличия резервов и ограничение бюджета.

Ливингстон предложил ежемесячно изымать часть профицита, создаваемого торговыми пошлинами, и направлять его в безопасное холодное хранение BTC, которое не будет торговаться, ставиться, продаваться, перезакладываться, использоваться для финансирования программ, обеспечения кредитов или предоставляться в качестве доходности.

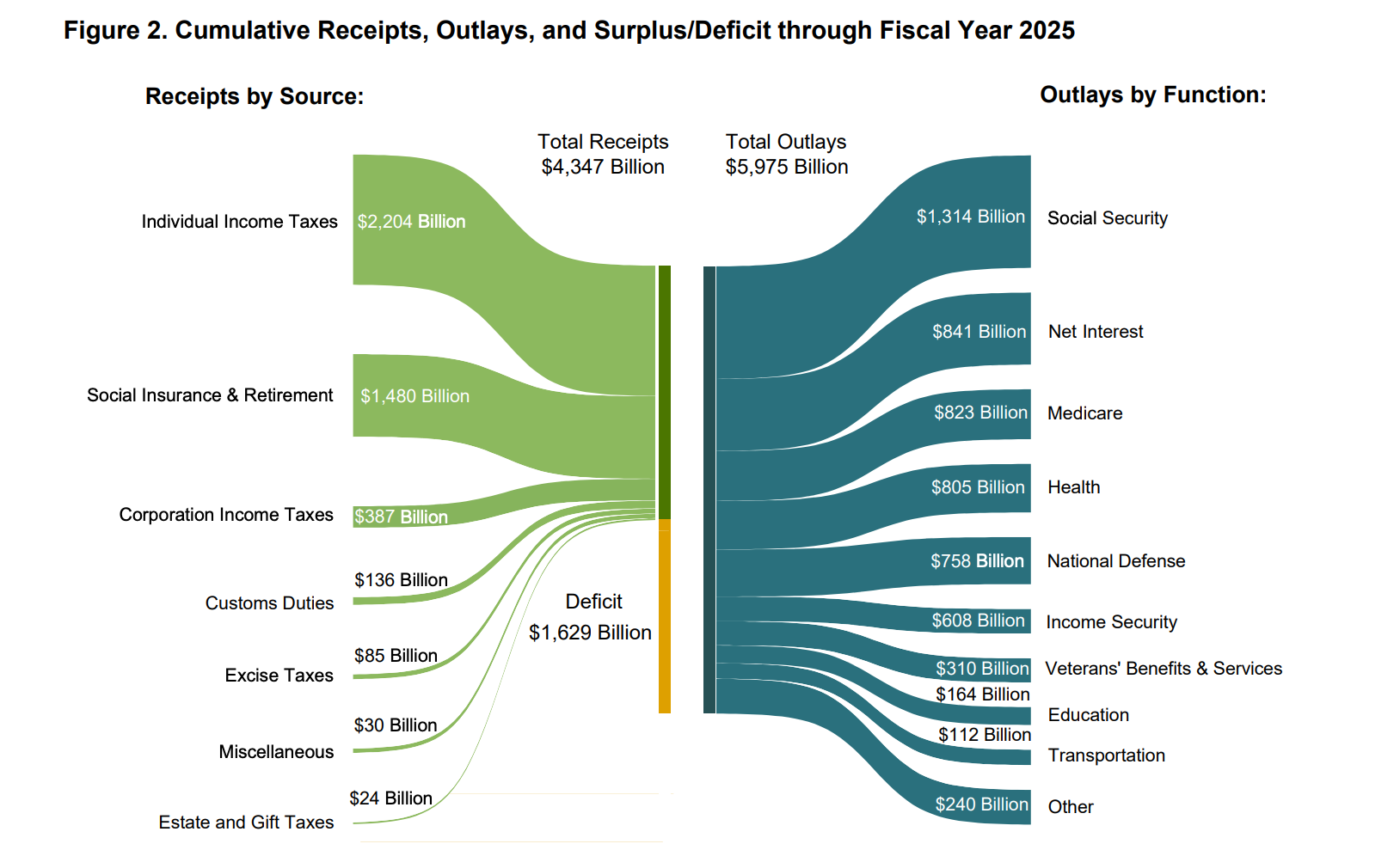

«По состоянию на июль мы собрали 135,7 млрд долларов таможенных пошлин — вдвое больше, чем в прошлом году. Повторюсь, у нас профицит от пошлин в размере 70 млрд долларов, и это при том, что финансовый год еще не закончился», — пишет он.

Этот излишек не распределен. Он не расходуется заранее. Он не связан с программой Medicare, социальными льготами или обслуживанием долга.

«Он просто висит в воздухе, ждет, ищет продуктивное применение», — продолжил Ливингстон.

Совокупные поступления показывают, что правительство США собрало около 136 миллиардов долларов таможенных пошлин за 2025 финансовый год. Источник: Министерство финансов США.

Предложение о финансировании стратегического резерва биткоина США за счет профицита пошлин может стать для правительства способом покупки большего количества биткоинов в соответствии с указом президента США Трампа, согласно которому дополнительные биткоины могут быть приобретены только в рамках бюджетно-нейтральных стратегий.

Министр финансов США подает неоднозначные сигналы о стратегическом резерве

Скотт Бессент, министр финансов США, заявил в четверг, что правительство США не будет покупать новые биткоины для стратегического резерва.

«Мы не будем покупать их, но будем использовать конфискованные активы и продолжать их наращивать», — заявил Бессент в интервью Fox Business.

Однако позже в тот же день Бессент уточнил свою позицию, пояснив, что правительство США все еще «изучает бюджетно-нейтральные пути» для накопления большего количества цифровой валюты.

Было предложено несколько бюджетно-нейтральных стратегий, включая переоценку золотых резервов Казначейства, которые в настоящее время оцениваются всего в 42,22 доллара за тройскую унцию, в то время как золото торгуется на спотовых рынках примерно по 3335 долларов за унцию.

Другие бюджетно-нейтральные пути включают перераспределение части других существующих резервных активов правительства, например, продажу нефти из стратегического нефтяного резерва для приобретения большего количества BTC.