香港《稳定币条例》(以下简称条例)已于 2025 年 8 月 1 日正式生效,该条例为稳定币的发行和运营制定了严格的规则,明确禁止在无牌照情况下的稳定币要约、推广与售卖,并未提供过渡期。

作为以稳定币、法币互兑为主营业务的机构,香港本地的加密货币找换店首当其冲,在条例生效后,多家场外交易服务商宣布暂停与稳定币相关的业务,等待申请牌照。

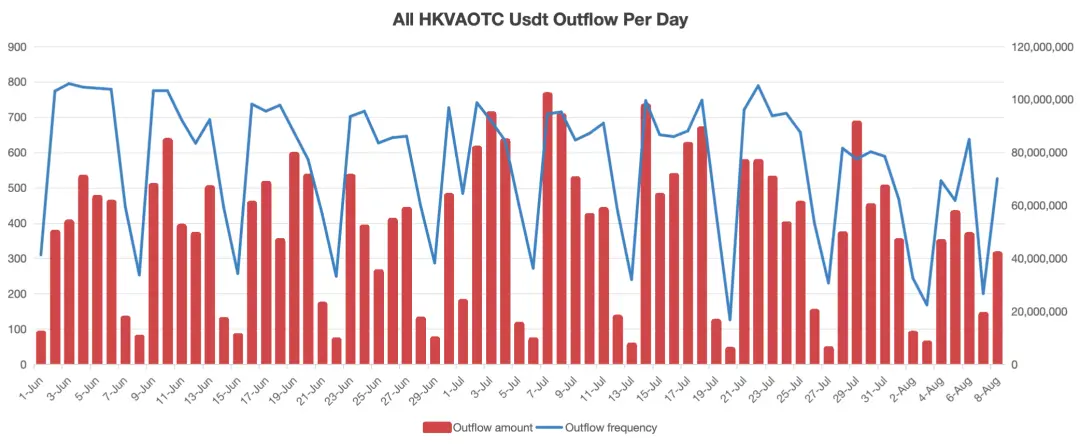

本文旨在通过披露香港场外交易服务商(HKVAOTC)地址在最近 70 天的 TRC20-USDT 流出数据,为监管部门提供考察条例影响力的链上视角。

数据说明

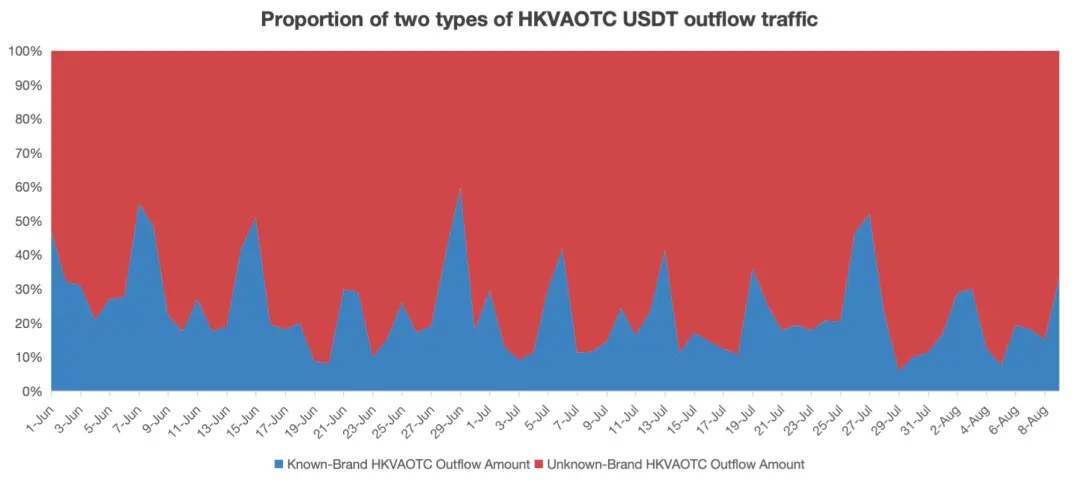

Bitrace 长期对位于香港或主要服务香港客户的 VAOTC 实体进行业务地址流量监测,后者分别归属于主要服务线下客户或实名客户的门店类型服务商,以及主要服务线上客户或匿名客户的非门店类型的服务商。

本次调查数据披露,将囊括所有服务商在北京时间 2025 年 6 月 1 日至 7 月 31 日、8 月 1 日至 8 月 8 日两个时间段内的 TRC20-USDT 转出数据。

以下数据均已剔除业务地址之间的非经营性质中转活动。

场外交易市场稳定币交易规模下降 32.94%

6 月 1 日至 7 月 31 日之间,全部业务地址共转出 3.17B USDT,日均 52.04M USDT;8 月 1 日至 8 月 8 日之间,全部业务地址共转出 279M USDT,日均 34.90M USDT。

相比于条例生效前,8 月 1 日后稳定币找换市场整体规模降低了 32.94%,这一敏感度表明条例对香港本地加密产业的影响程度之深远。

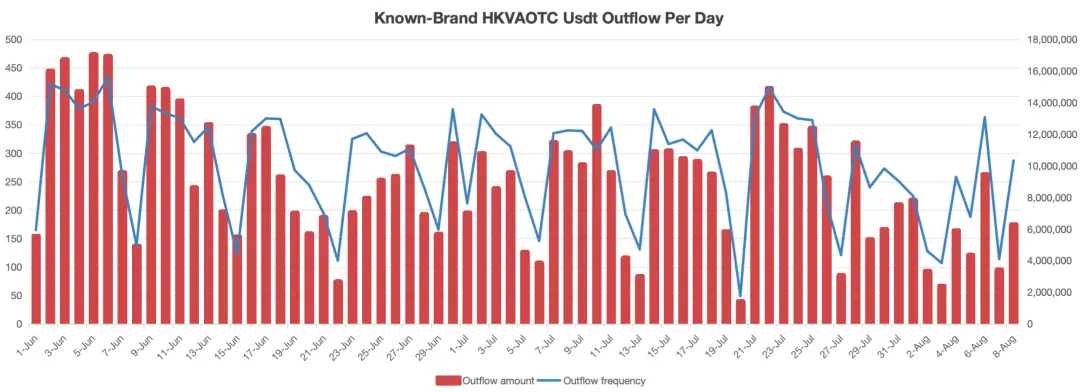

门店类型服务商降低规模更大

对门店类型与非门店类型的服务商业务地址分别进行流量统计。

门店类型服务商业务地址在条例生效后,日均 USDT 转出规模减少了 43.20%(9.47M -> 5.38M),非门店类型服务商业务地址则减少了 30.65%(42.57M -> 29.52M)。

门店类型服务商遭受的影响显著高于非门店类型,表明条例生效后,香港场外交易服务行业部分商家在短时间内出现转入地下的趋势。

写在最后

《稳定币条例》的出台标志着香港加密行业合规的重要进展,短期内对当地场外交易服务行业产生显著影响。在相关从业者中,部分选择遵循监管申请牌照,部分则转向地下运营,呈现差异化选择。