综编:Felix, PANews

原标题:特朗普签署行政令:美国退休金可投资加密货币,近9万亿美元市场或迎巨变

美国总统唐纳德·特朗普于周四(8 月 7 日)签署了一项行政命令,允许美国人将 401(k) 退休储蓄投资于加密货币、私募股权和房地产等其他另类资产。签署的行政命令中指示:

-

在 180 天内,劳工部重新评估《雇员退休收入保障法》(ERISA)管辖的 401(k) 计划和其他固定缴款计划中的另类资产投资方面的义务的指导意见。

-

劳工部长澄清劳工部对另类资产的立场,以及与提供包含另类资产投资的资产配置基金相关的适当的受托流程。

-

劳工部长与财政部长、美国证券交易委员会(SEC)和其他联邦监管机构协商,以确定是否应在这些机构进行类似的监管改革。

-

美国 SEC 通过修订适用的法规和指导意见,为参与者导向的固定缴款退休储蓄计划提供获取另类资产的便利。

在特朗普的行政命令中,明确将加密货币与另类资产归为一类,并纳入 401(k) 退休储蓄投资计划。此前美国劳工部曾发布指导意见,要求受托人“在考虑将加密货币添加到 401(k) 计划参与者的投资菜单中之前务必格外谨慎”。今年 5 月,该指导意见已被完全撤销。

受此消息影响,行情数据显示,比特币过去 24 小时上涨近 2%,以太坊上涨超 7%。

近9亿美元美国退休金将开放加密货币敞口

美国的养老金分为三个部分:第一部分是国家层面的社会保险金,保证就业者退休之后的基本的养老生活。第二部分是企业的养老金计划,401(k) 计划是其中重要组成部分,只应用于私人公司的雇员,是美国最为普遍的就业人员退休计划。第三部分是私人年金计划。

401(k) 计划是一种由雇主提供、享受税收优惠的退休储蓄计划。该计划以雇员供款为主,即员工从自己的税前工资中提取一部分存入 401(k)账户,雇主通常也会提供一定比例的匹配供款。例如员工存入工资的 6%,雇主也额外存入 3%或 6%(具体比例和规则由雇主设定)。

2025 年美国国税局设定员工自愿供款的上限为 23,500 美元,50 岁及以上者可额外追加 7500 美元。员工通常可以从雇主提供的一系列投资基金中选择进行投资,自行承担投资风险。但是雇员在 59.5 岁之前提取资金,通常需缴纳 10% 的额外罚款税,并补缴所得税。

目前美国 401(k) 平台提供商市场集中度较高,据估算,前五大提供商(Fidelity、Empower、Vanguard、Principal、ADP)合计掌握了超 60% 的 401(k) 市场资产。

在商业模式方面,Fidelity、Empower、Principal 和 Voya 偏向综合型,同时提供记录保管、投资管理、自有基金产品。Vanguard 和 BlackRock 主要擅长投资管理。

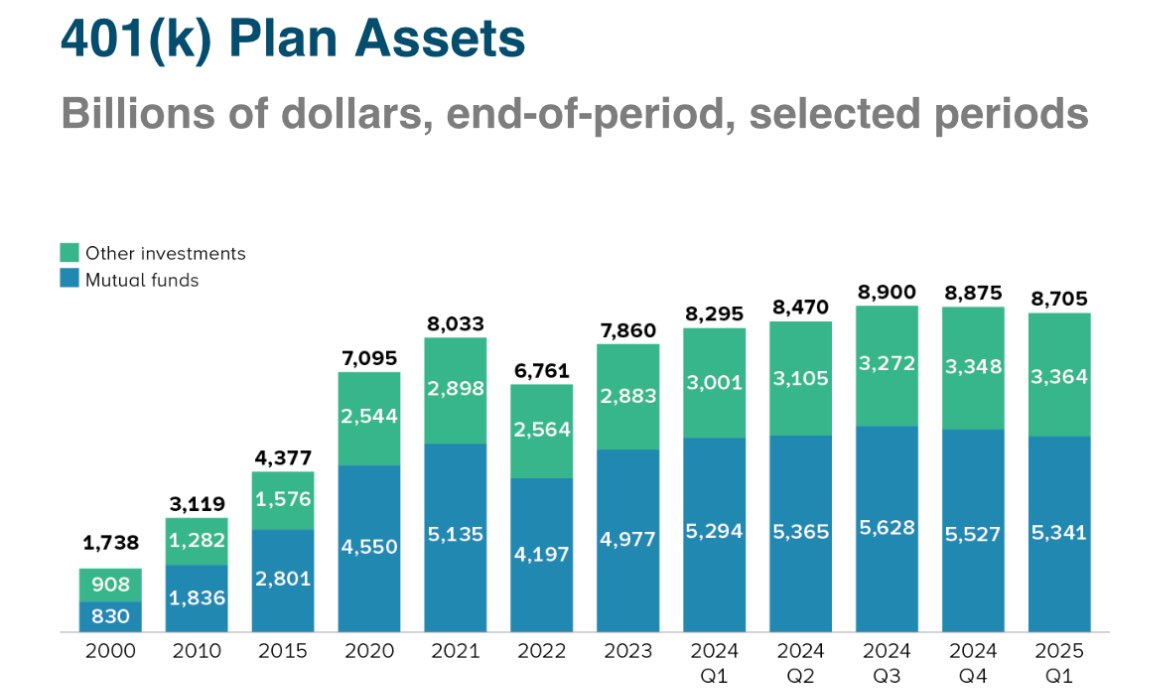

根据 Investment Company Institute(ICI)于今年 6 月发布的报告,401(k) 计划持有 8.7 万亿美元资金,超过 9000 万美国人参与了雇主赞助的固定缴款计划。在 401(k) 中,共同基金管理资产为 5.3 万亿美元,占比 61%;其中权益基金占 3.2 万亿美元,为最大类;其次为混合基金,持有约 1.4 万亿美元。

各方褒贬不一,对加密货币利好

虽然将加密资产引入401(K)加大了退休基金的风险,但这对于新兴的加密行业无疑是一种利好。

分析师 Geiger Capital 发推称,“401k 养老金持有约 9 万亿美元的资产。如果仅将 5% 的资金投入比特币,那么价值将达到 4500 亿美元。比特币的总市值为 2 万亿美元。”

投资机构 Varys Capital 合伙人 Tom Dunleavy 分析指出, “大多数美国人每两周从雇主那里收到工资时,都会将其中的一部分(通常在 1% 到 10% 之间)分配到他们的 401(k) 退休账户中。通常情况下,股票占比 60%,债券占比 40%。如果突然间加密货币的配置比例变成 5%,那么未来几年,你会看到上千亿美元的资金涌入这一资产类别。”

Bitwise 研究主管 Ryan Rasmussen 表示: “特朗普 401(k) 行政命令的短期影响在于,它向投资者发出了另一个信息,即加密货币的监管觉醒将持续下去。” “这显然会推高市场。” “从中期来看,行政命令和 401(k)计划提供商的回应将把数百亿(甚至数千亿)的资金引入加密资产。”

相对于加密圈的一片喝彩声,传统金融领域也发出了理性的声音,提醒此举也伴随着一定的风险和挑战。

首先投资费用可能会蚕食收益。私募股权基金一般每年会向投资者收取 2% 的管理费,外加基金利润的 20%。晨星分析师 Jason Kephart 表示,这项行政令为资产管理公司带来了“巨大的机遇”,但也引发了个人投资者的担忧。“由于增加了额外费用、增加了复杂性,而且透明度降低,情况就变得不那么明朗了”。

其次,相应的诉讼案件也会增加。Stifel 首席华盛顿政策策略师 Brian Gardner 预计,劳工部将需要审查其关于计划受托责任的指导意见,因为 401k 计划参与者在私人投资中亏损可能导致针对经理的诉讼。

再次,缺乏流动性也是一大弊端。401(k)允许投资私募股权,但这类资产往往缺乏流动性,投资者的资金通常会被套牢数月甚至数年。这可能意味着,401(k) 计划中的私募股权基金持有者可能难以快速出售股票,无论是为了筹集现金还是购买其他投资产品。

最后值得一提是,尽管行政命令已签署,但 Fidelity 和 Vanguard 等提供商需要开发合适的产品,而这些产品的普及可能需要数年时间。

Twitter:https://twitter.com/BitpushNewsCN

比推 TG 交流群:https://t.me/BitPushCommunity

比推 TG 订阅: https://t.me/bitpush