撰文:佐爷

Crypto 在做支付,Fintech 在做稳定币。

过去一年,加密货币的行业发展就是和传统金融企业、Web 2.0 巨头和全球政治家们双向奔赴,特朗普的空气币是加密流动性的结束,而媾和才刚刚开始。

巴基斯坦的顾问、不丹的加密矿场和中东的天价融资,最终都化身压倒散户的最后一根根稻草,那就都去许愿池当王八吧,也许还能获得几许痴情。

加密大停滞时代

人类是很奇怪的生物,以前都传统的时候追求自由,现在都自由的时候追求传统。

人类唯一学会的教训是学不到任何教训。

我还记得,Bitcoin Spot ETF 通过的时候,都以为比特币会改变这个世界,当然,现在都认为 Bitcoin 就是 M2 的映射资产,本身既起不到降低通胀保值增值的作用,被 ETF 抽离后也无法作为币圈牛市发动机的助燃剂,一根筋变成了两头堵。

人类唯一学会的教训是学不到任何教训 +1。

在特朗普抱着空气币降临他忠诚的币圈时,暴涨后的沉寂也不足为奇,PumpFun 的自救,币安钱包的出击,或是 Boop 到底是不是币安 CXO 都变成了闹剧本身,还是赚不到钱的那种。

图片说明:加密现有格局,图片来源:@zuoyeweb3

太阳底下没有新鲜事,加密货币只有大停滞。

先是「人类文明级别的创新」以太坊抵不过 4000 到 1500 的回落,要借助 Risc-V 重回 L1 战事,如果 EVM 都可以改头换面,不如一步到位,把 PoS 改成 PoW 得了,以太坊押注 L1 和新加 Risc-V 真的能解救自己吗?

被敌人指挥是最愚蠢的行为,可惜 Solana 这次是指挥者,Solana 押注 L1 是在 FTX 之前,也是在 FTX 之后。

本质上而言,SVM L2 或者扩展层也是对 Solana 的吸血行为,是鲸鱼身上的鲋鱼,不是鲸鱼有意为之,但是 ETH L2 是以太坊上的藤壶,还是以太坊自己招来的。

我们以前熟悉的市场范式一去不复返了,ETH is not Money, Stablecoin is Money.

其次是无效信息在侵染整个市场,KOL Summer 会迅速变成 KOL Agency Summer,然后是 CEX Summer,不信的话,看看这次迪拜音乐节的盛况吧,项目方、KOL 和交易所,最终都是交易导向,交易所本身就是交易行为的承接点,这是无解的局。

这不是对 KOL 的批判,而是对市场规律的认可,从最早的三点钟社群 AMA、社区化的币乎,再到千媒大战的往事,KOL 火热顶点也是终点,导向交易就是信任和影响力的出清时刻。

不过本次周期也有新分化趋势,虽然都是无效信息,一般分两类:

1. 垃圾喊单,下沉市场

2. 老钱站台,宣扬存在

再次是 VC 的破灭和坚守,依靠美元资本,硅谷、中东和欧洲 VC 都在布局下一阶段,而孤单影只的华人 VC,被 LP 和 ROI 持续拷打,已经和创新没有关系,都在快速的做市商化,反正都要导向交易,不如节约步骤自己干。

真正的创新在以前华清嘉园,以后会在深圳科技园,华人 Founder 要在硅谷和华尔街找钱,但是真正满足市场下一阶段的项目,不会被投资人按照现有框架认可。

币圈不需要 FA,Meme 无法做空。

原因无他,交易路径太短,交易所正在虎视眈眈,盯着任何流量,宁可浪费撒网,也不能错过风口,唯一的受益者变成了从互联网逃入 CEX 的前大厂『er,跳动的不止有字节,还有牛马的食槽。

2018 年的今日头条,平均在职时间只有 4 个月,而到了 2024 年的字节系,已经涨到了 7-8 个月,但是更多的人还是要被输送到社会,币圈大厂,他们只看得上头部 CEX。

今日份暴论:VC 获益人是顶校生,CEX 获益人是大厂淘汰人,他们带来的不止有专业和漂亮履历,还有更层级深化的运作标准,以及中介成本增多后的资本效率的下降。

币圈那种勃勃生机,万物竞发,一心只想搞钱的时代和人,都一去不复返了。

持续性的体制化,变成了币圈的紧箍咒,币圈更像互联网,互联网更像 XXX。

发明是需求之母

我没有 FUD 加密货币,更准确的心态是「对加密行业有信心,对自己的前途很担忧」,这不再是一个小众的、充满暴富机遇的行业,从业者正在被互联网、金融业大置换,加密 OG 和地推要么进大牢,要么当小弟,要么进完大牢当大佬小弟,Baby 今晚打老虎。

牢骚太盛防肠断,我们不该继续讨论 VC 和交易所,要么像以太坊从头来过,要么探索新的生态,在加密行业的每次危机中,都会诞生新的资产发行方式,比如 ERC-20 支撑 DeFi,NFT 支撑 BAYC,现在来到了稳定币阶段。

请注意,上轮链上活动的核心是以太坊和借贷,「乐高式」的放大资本效率,而本轮的以太坊和质押模式,并没复刻奇迹,在我们这个时间线,腾讯没有发明微信,而是小米米聊崛起。

生息稳定币(YBS)成为新的发明,他们会制造新的需求,不是因为大家对稳定币的需求无法满足,USDT 活的好好的,而是可以这样做 YBS,Ethena 才被发明,参考美元铸币税终结,稳定币超级周期。

YBS 会成为新的资产发行形式,这是一个预期,仿照心里史学,对于未来,我有三种预测,分别指向不同的未来:

-

YBS 成为新的资产发行方式,以太坊换「芯」成功。ETH 取代 BTC 成为新的加密发动机,Restaking ETH 成为真正的 Money;

-

YBS 成为新的资产发行方式,以太坊走入沉寂。YBS 会被国债等美元资产吞噬,Fintech 2.0 成真,Web 3.0 成为黄粱一梦;

-

YBS 不成为新的资产发行方式,以太坊暴卒无声。那么区块链会「去币存链」,Fintech 1.0 是 Paypal 对银行的替代,Stripe 是对收单的电子化革新,那么无币区块链最多是 Fintech 1.5。

总结一下,Fintech 2.0 是金融区块链,Fintech 1.5 是无币区块链技术。

稳定币正在成为新的资产发行模式,这是任何 VC 研报从来没有预测到的事,甚至是 Ethena 自己都没这么想过,如果我们认为市场本身就是最优解,VC 和交易所最大的问题不是学习 Vitalik 沉迷技术叙事,而是不尊重市场规律。

在现有的币圈格局下,交易所、稳定币和公链事实上三家独大,币安、USDT 和以太坊构成了主角团,其他的都是围绕三者的供货商和分销渠道,交易所和公链比较稳定,现在战火集中在稳定币,不仅 USDC、贝莱德等在进军,链上给出的答案就是 YBS,事关全局,责无旁贷。

PS,交易所稳定指的是币安一家独大,公链稳定指的是以太坊重新振兴,Solana 取代还在路上。

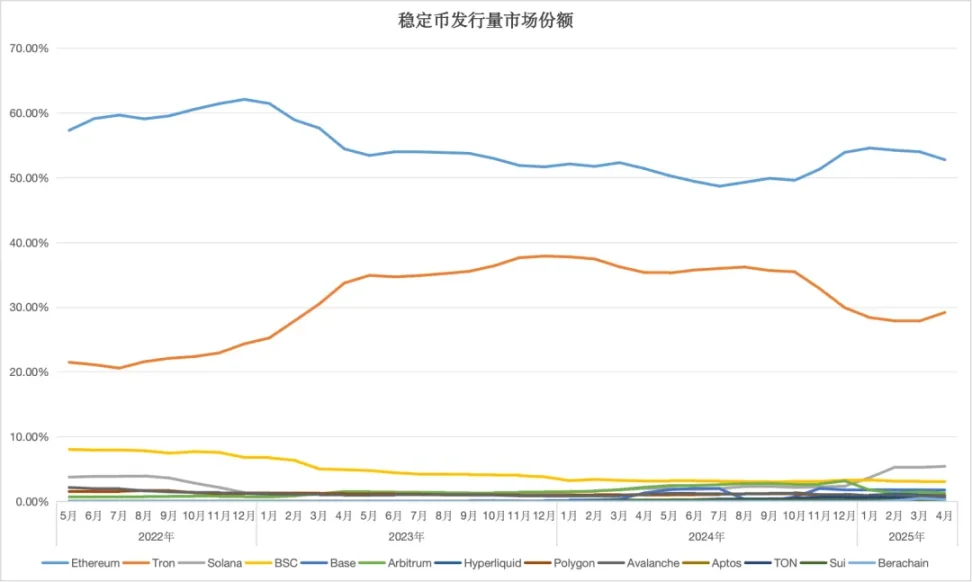

图片说明:稳定币市场发行量,图片来源:@zuoyeweb3

在如今的市场格局中,以太坊、Tron 两家独大,但是 Solana 并未放弃追赶,尤其是以太坊并未被彻底击败,总能听到 Solana DEX 交易量超越以太坊生态的消息,但是从真实的资产发行量上而言,ETH+ERC-20 USDT 仍然稳占鳌头。

这也是我认为以太坊基本面没有问题的主要原因,大家对 ETH 的价格期待是 1 万,对 SOL 的期待是 1000,基点完全不同。

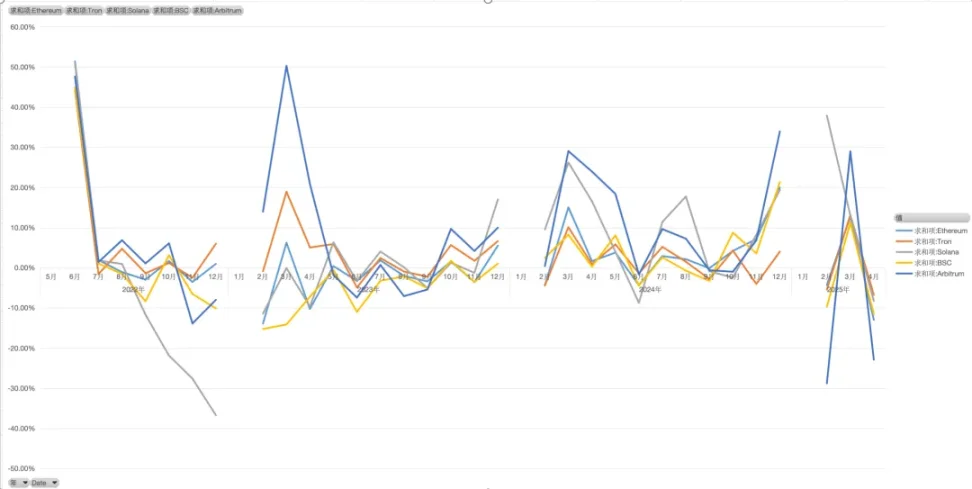

图片说明:稳定币增长速率,图片来源:@zuoyeweb3

尤其是对比各链增长速率,我们可以发现基本同频,除了 Solana 在 2022 年接近死亡外,其余时间大家跟以太坊保持一致,我们可以认为,在相关性上,各链稳定币没有走出独立行情,仍然是以太坊的外溢。

据此,说明了以太坊和稳定币配对的重要性,而 YBS 的重要性在于换锚,2300 亿的稳定币市值,USDe 等 YBS 仍然只是 others。

还是那句话,YBS 必须成为新的资产发行方式,才能将 ETH 的资产属性传导到货币层面,否则,RWA 的春天就是币圈的寒冬。

结语

以太坊只有技术叙事,用户只拥抱稳定币。

我们希望用户拥抱的是 YBS,而不是 USDT,这是目前的现状,也是我们和市场的分歧。

追求小众是很大众的事,看看贯穿式尾灯和遍布世界的 LABUBU 吧,浅浅提一下区块链支付,支付没有任何问题,但是在加密原生资产支撑的 YBS 主流化之前,强推区块链支付是「结果早于原因」,即支付应该是 YBS 的方向。

加密货币不要成为 Fintech 2.0,路不能越走越窄。