JPMorgan analysts forecast that yield-bearing stablecoins could rise from the current 6% to as much as 50% of the stablecoin market cap in the future.

Yield-bearing stablecoins are attracting investors similarly to traditional money market funds, particularly in today’s high-interest-rate environment, the analysts said.

Yield-bearing stablecoins, including tokenized Treasurys, which offer interest returns similar to traditional financial products, could experience massive growth ahead, according to JPMorgan analysts.

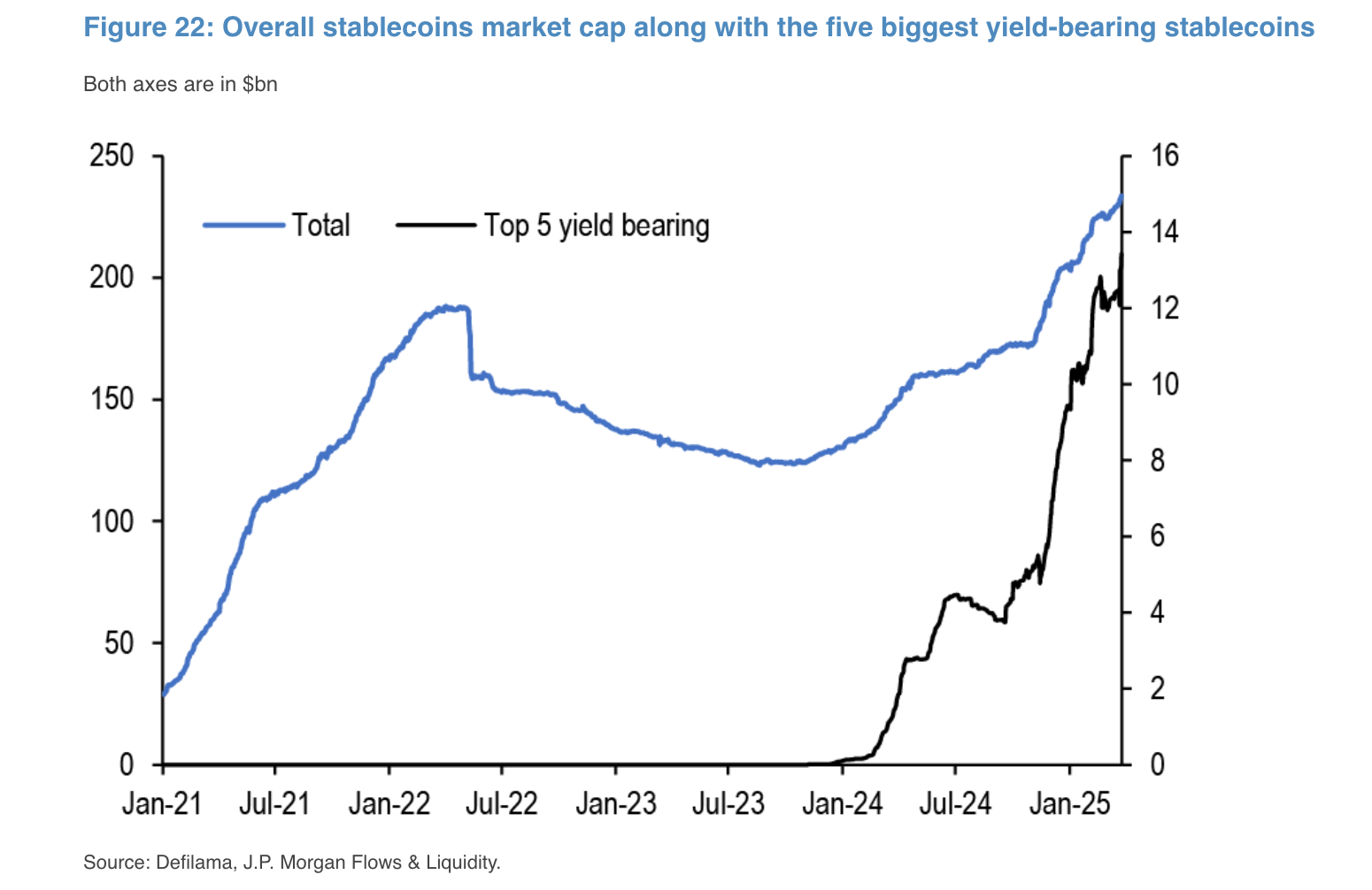

Yield-bearing stablecoins currently make up just 6% of the total stablecoin market cap but could expand significantly, potentially capturing up to 50% of the market unless regulatory changes intervene, JPMorgan analysts led by managing director Nikolaos Panigirtzoglou wrote in a report released Wednesday.

The top five yield-bearing stablecoins — Ethena's USDe, Sky Dollar's USDS, BlackRock's BUIDL, Usual Protocol's USD0 and Ondo Finance's USDY— have seen rapid growth since the U.S. election in November, rising from around $4 billion to over $13 billion in combined market cap, Panigirtzoglou told The Block.

According to analysts, this growth is expected to continue. They added that the U.S. Securities and Exchange Commission's recent approval of Figure Markets' application for a yield-bearing stablecoin, YLDS, which is registered as a security, provides further momentum to this segment.

Traditional stablecoins, such as Tether's USDT and Circle's USDC, do not share reserve yields with their users because doing so would classify these assets as securities, according to the analysts. Such a classification would also impose additional compliance requirements, hindering their current seamless use as collateral within the crypto ecosystem, they said.

Why yield-bearing stablecoins are on the rise

The JPMorgan analysts identified several factors driving the rapid growth of yield-bearing stablecoins.

First, investors prefer these assets because they offer interest without requiring holders to engage in risky trading or lending activities or give up custody of their assets.

Second, major crypto trading platforms such as Deribit and FalconX now accept tokenized Treasurys as collateral, enabling traders to earn yield on posted collateral.

Additionally, crypto investors are increasingly turning to tokenized Treasurys in decentralized finance (DeFi) to obtain higher yields, as typical DeFi yields have significantly decreased from their peak levels of 2022. Projects like Frax Finance are also adopting tokenized Treasurys as underlying assets, further fueling this growth.

Despite this positive outlook, the JPMorgan analysts noted barriers. Yield-bearing stablecoins are classified as securities, subjecting them to regulatory restrictions that limit their adoption, especially among retail investors. Moreover, traditional non-yield-bearing stablecoins continue to hold a notable liquidity advantage.

With a combined market cap of around $220 billion across multiple blockchains and centralized exchanges, traditional stablecoins offer efficient, fast and low-cost transactions, even at large volumes. In contrast, yield-bearing stablecoins are newer, smaller and comparatively less liquid.

However, "This liquidity disadvantage could potentially be lessened over time as yield-bearing stablecoins gain further traction in the future in crypto derivative trading as source of collateral, in DAO treasuries, liquidity pools, and idle cash with crypto venture funds," according to the analysts.

As a result, over time, yield-bearing stablecoins could attract much of the idle cash currently sitting in traditional stablecoins, the analysts said. While the exact amount of this idle cash is difficult to estimate, it's unlikely to represent the majority of the stablecoin market, according to the analysts.