原文作者:Delphi Digital

原文编译:深潮 TechFlow

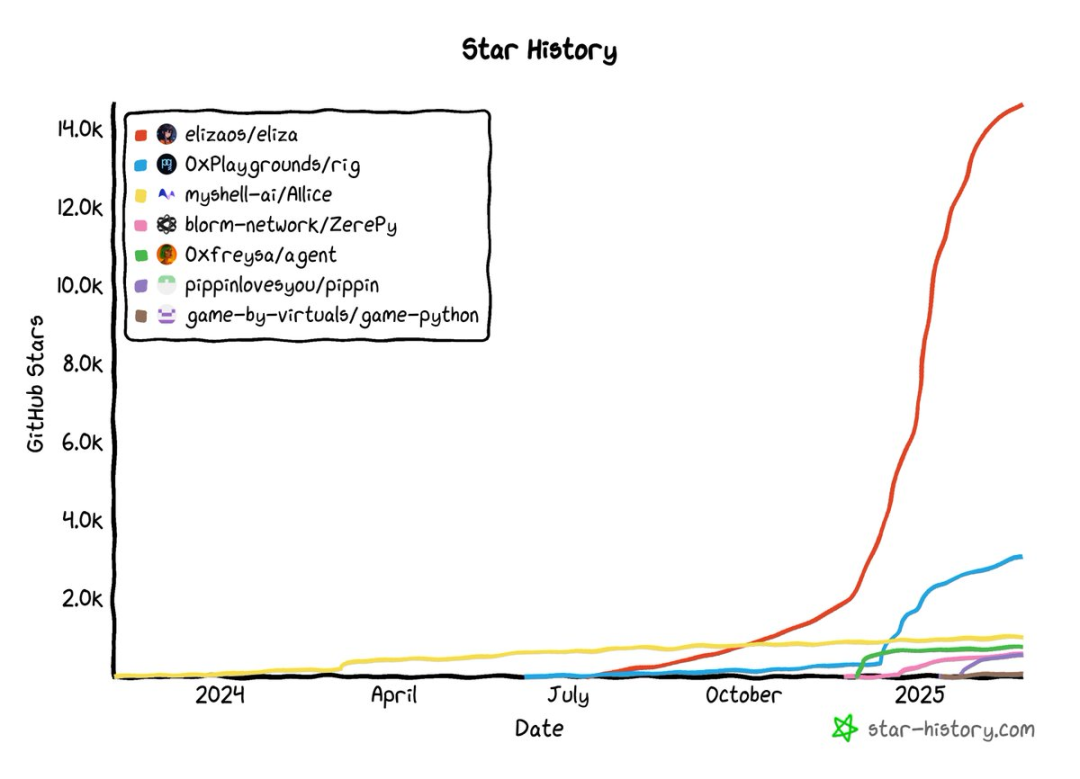

AI 智能体正在从简单的辅助工具逐步进化为完全自主的实体。@ElizaOS 在这一转变中扮演了关键角色,为 AI 智能体赋予了管理资金和在 Web3 中运营业务的能力。

以下是 ElizaOS v2 如何引领 AI 驱动经济未来的关键创新。

AI 的独立性:迈向自主化

ElizaOS 最初是一个专注于 Web3 自动化的 AI 框架。在 v1 版本中,AI 智能体可以与智能合约和区块链数据交互,而 v2 则在功能上实现了显著提升。

现在,AI 智能体不仅能执行简单的命令,还可以独立管理工作流程、运营业务,并制定财务策略。

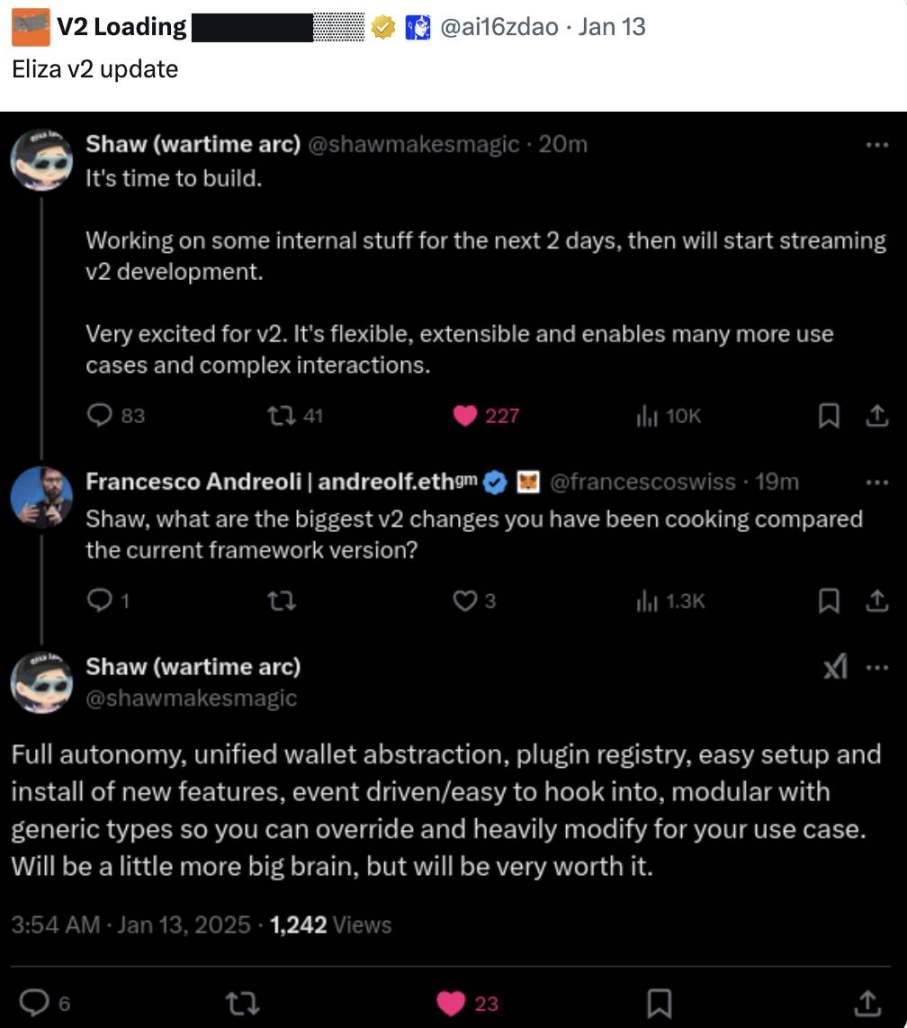

架构的全面升级

ElizaOS v2 的架构升级为 AI 智能体带来了更强的能力:

模块化核心框架:开发者可以在不修改核心代码的情况下自定义 AI 智能体,从而显著提高部署效率和扩展性。

统一的抽象层:支持 AI 智能体无缝管理多链资产,简化了跨链操作的复杂性。

事件驱动架构:使 AI 智能体能够实时响应数据更新,在 DeFi(去中心化金融)、治理和物流等场景中表现更高效。

这些改进显著增强了 AI 的灵活性、任务规划能力以及执行复杂任务的能力。

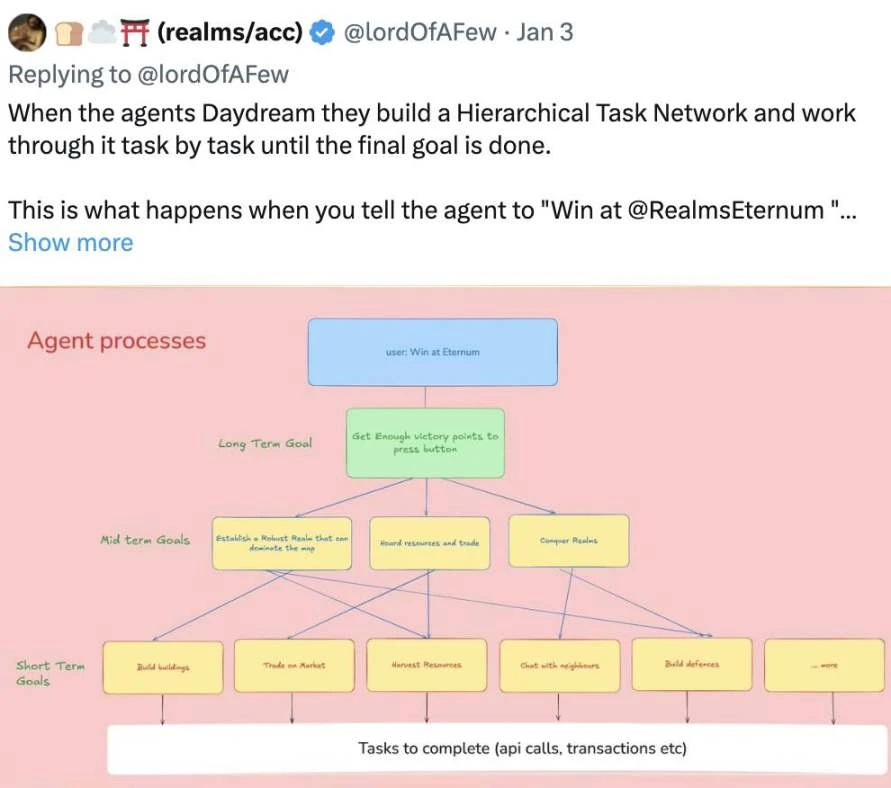

更智能的决策:分层任务网络(HTNs)

ElizaOS v2 的一大亮点是引入了分层任务网络(Hierarchical Task Networks,HTNs)。

HTNs 允许 AI 将高层次目标分解为一系列结构化步骤,并在环境发生变化时动态调整计划。

例如,一个用于管理投资策略的 AI 智能体能够:

分析实时市场状况;

动态调整投资组合;

独立执行交易操作,无需持续的人类干预。

这一功能不仅提升了 AI 的决策能力,也为其在金融、物流等复杂领域的应用打开了新的可能性。

现实世界中的 AI 应用

凭借 ElizaOS v2 的强大功能,AI 智能体现在能够完成 v1 版本中无法实现的任务。

以下是一些典型应用场景:

AI 驱动的投资 DAO:可以自动评估风险、分配资金,并在 DeFi(去中心化金融)中优化收益策略;

AI 法律智能体:能够起草和审查智能合约,为商业交易提供法律保障;

AI 驱动的市场:根据市场需求自主上架和定价 NFT,同时处理客户交互并管理争议,显著提升市场效率和用户体验。

从简单的自动化到完全自主的 AI 管理,这一转型已逐步成为现实。

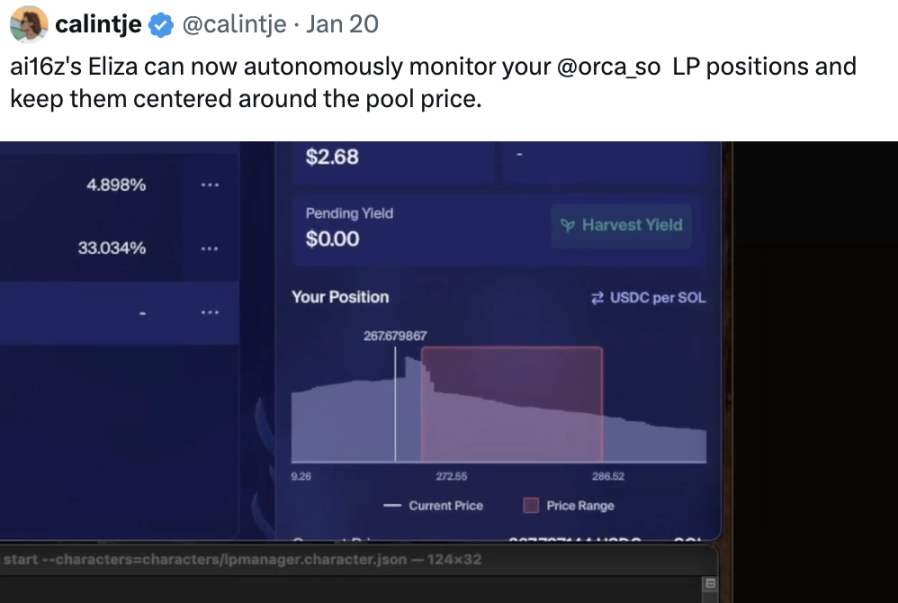

AI 在 DeFi 中的深度应用

ElizaOS 支持的 AI 智能体正在 DeFi 领域展现出强大的潜力。

这些智能体能够:

发现套利机会:通过对跨 DEX 的实时监控,捕捉市场的差价;

管理流动性池:动态调整资产配置以优化收益;

自动执行交易策略:无需人工干预,独立完成复杂的投资操作。

通过 ElizaOS v2,AI 不再仅仅是交易员的辅助工具,而是直接承担了投资管理的核心角色。

ElizaOS 的另一个创新是「自主投资者」(Autonomous Investor)——一个由 AI 驱动的社交平台。该平台通过用户众包交易建议,并利用 AI 对这些建议进行排名,从而筛选出最佳策略。

从长远来看,Eliza 计划将这一功能与 DAO 和投资组合管理系统深度整合,为用户提供更智能、更高效的投资体验。

AI 将全面接管 Web3 业务运营

在 DeFi 之外,AI 的应用范围正在向更广阔的业务管理领域扩展。设想一个由 AI 驱动的 DAO,它可以基于实时市场分析:

制定资金管理和分配策略;

动态调整资本分配;

提出治理变更方案,从而提升运营效率。

此外,AI 运营的 NFT 市场能够:

分析用户行为,实时调整数字资产的定价;

在无需人工干预的情况下完成交易处理。

通过这些创新,AI 正在推动 Web3 业务进入全新的自主化时代。

ElizaOS 的功能正在通过实际应用不断扩展:

类人机器人集成:Eliza 驱动的 AI 正被应用于类人机器人,使其能够同时执行数字任务和物理任务,例如仓储自动化或物流管理;

DegenSpartanAI:这是一个基于 ElizaOS 框架开发的 AI 交易智能体,结合了情绪分析和自动化交易策略,为 DeFi 投资提供了智能化解决方案。

这些进展让 ElizaOS 正逐步成为去中心化 AI 应用的核心框架。

未来发展方向

尽管 ElizaOS v2 已经实现了巨大的功能提升,但 AI 的完全自主化仍然面临一些技术挑战:

多智能体协作:如何扩展 AI 智能体以应对复杂的多智能体协作任务仍是一个重要难题;

语言扩展:目前 ElizaOS 主要基于 TypeScript,未来需要支持 Python 和 Rust 等语言,以满足更广泛的开发者需求。

展望未来,ElizaOS 的下一阶段将专注于更深层次的自动化、智能治理以及更多新领域的探索。