- Цена ADA снизилась, но аналитики, такие как Али Мартинес, прогнозируют значительный рост, ссылаясь на прошлые ралли.

- В Хельсинки запущен новый биржевой торгуемый токен Virtune Staked Cardano ETP, предлагающий инвесторам доступ к ставкам и вознаграждение за стейкинг.

- Несмотря на падение цены, долгосрочный потенциал остается высоким благодаря технологичности Cardano и растущему принятию.

Cardano (ADA) привлекла значительное внимание растущими дискуссиями о ее потенциальной роли в секторе блокчейна. Были даже некоторые предположения о возможности использования Казначейством США сети Cardano для финансовой прозрачности.

What if #Cardano is the chosen network to bring the US Treasury onto the blockchain? https://t.co/jkWcpAp2b1

— Ali (@ali_charts) February 6, 2025

Цена Cardano (ADA): недавняя тенденция к снижению

На момент публикации Cardano торгуется по $0,7168, что отражает снижение на 3,23% за последние 24 часа. Актив также упал на 26,27% за последнюю неделю.

Несмотря на недавний нисходящий тренд, криптовалюта сохраняет сильное присутствие на рынке с общим оборотным предложением в 36 млрд ADA и рыночной капитализацией в $25,72 млрд. Эксперты отрасли считают, что ADA по-прежнему имеет большой потенциал роста в предстоящем рыночном цикле.

По теме: Cardano получает значительный импульс благодаря Dex Tools и листингу Dex Screener

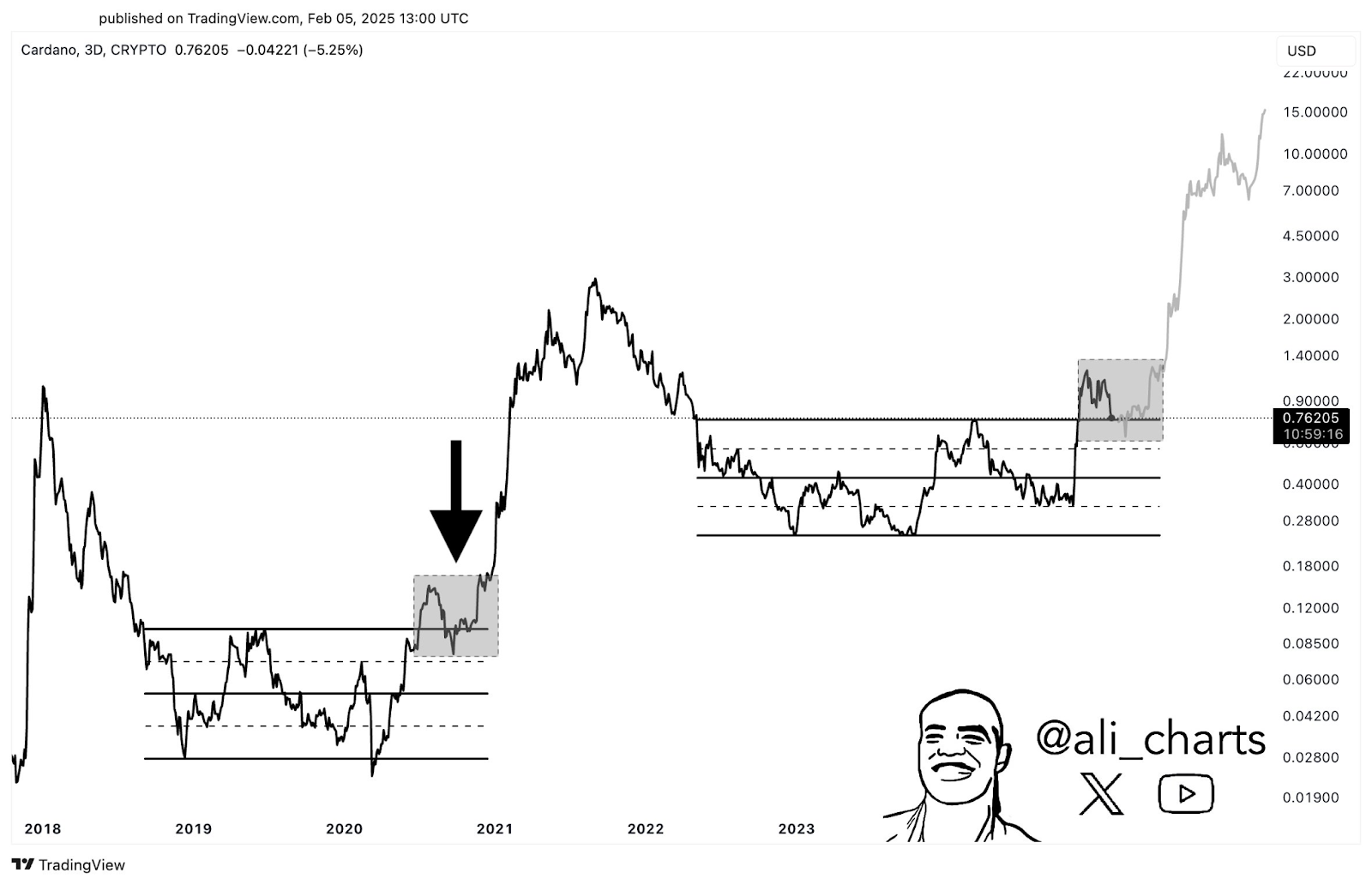

Аналитики предсказывают «чудовищный» рост ADA

Известный криптоаналитик Али Мартинес отметил, что ранее ADA подскочил с менее чем $0,10 до более чем $3 в середине 2021 года. Он предположил, что токен может находиться в начале еще одного значительного параболического ралли, и его цена может достичь $15, если история повторится.

CryptoRus поддержал это оптимистичное настроение, подчеркнув, что ADA, по всей видимости, готова к существенному росту цен.

Кроме того, Лаки, известный пользователь X с более чем двумя миллионами подписчиков, утверждал, что сильные фундаментальные показатели Cardano и растущее принятие могут подготовить почву для восходящего движения. Эти перспективы усиливают веру в то, что ADA остается надежной ставкой в текущем рыночном ландшафте.

В Финляндии запущен новый стейкинг Cardano ETP

В стремлении расширить инвестиционную доступность Cardano шведский управляющий цифровыми активами Virtune запустил Virtune Staked Cardano ETP на фондовой бирже Nasdaq Helsinki. Финансовый продукт, торгующийся под тикером VIRADAE, начал торговаться 5 февраля 2025 года.

По теме: Сообщество Cardano устало от мошенников, Хоскинсон реагирует

Недавно представленный Cardano ETP предлагает экспозицию 1:1 к ADA, позволяя как розничным, так и институциональным инвесторам получить прямой доступ к криптовалюте. Более того, инвесторы получают дополнительную 2% годовой прибыли за счет вознаграждений за стейкинг, которые постоянно добавляются и отражаются в ежедневной цене ETP.

ETP полностью обеспечен ADA и надежно хранится в холодном хранилище Coinbase с комиссией за управление в размере 1,49%.