原文作者:深潮 TechFlow

2024 年 12 月 3 日,韩国总统尹锡悦突然宣布实施「紧急戒严」,这一决定不仅震惊韩国政坛,更引发了严重的宪政危机。

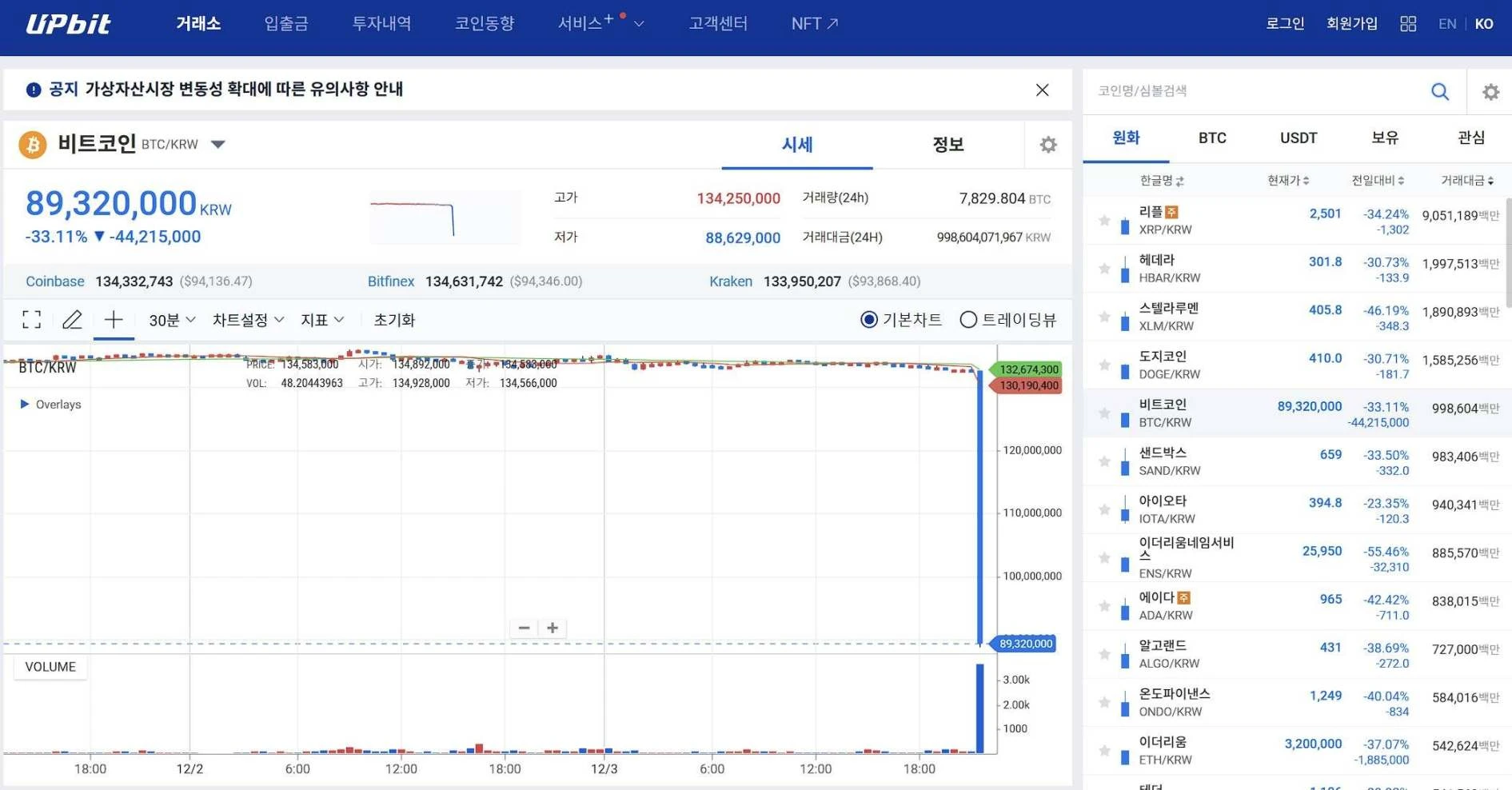

当然,受伤的一如既往有加密货币投资者,韩国最大的交易平台 Upbit 上比特币价格一度插针跌至 6.5 万美元。

那么,问题来了,为何尹锡悦宣布突然戒严?

尹锡悦宣布戒严的直接理由是「维护自由宪政秩序」,指责在野党「裹挟国会,搅乱国家」,要保护大韩民国免受朝鲜共产主义势力的威胁,并铲除亲朝反国家势力。

他口中的敌人是谁?

那就是尹锡悦在政坛的一生之敌——李在明。

在韩国政坛,尹锡悦与李在明的对立已成为近年来最引人注目的政治戏码。这场始于检察系统、延续至总统大选、最终演变为司法追责的恩怨,不仅是两位政治人物的个人较量,更折射出韩国社会的深层分歧。

2019 年,时任检察总长的尹锡悦开始对执政的共同民主党展开一系列调查。当时担任京畿道知事的李在明,也成为检方关注的对象之一。这种对立在 2022 年的总统大选中达到顶峰,两人在竞选过程中展开激烈交锋,互揭对方家族腐败和配偶问题等丑闻。最终,尹锡悦以微弱优势胜出,入主青瓦台。

虽然,李在明在 2022 年的总统选举中以微弱劣势败给了尹锡悦。然而,他的政治影响力并未因此减弱。

2023 年的戏剧性转折让这场恩怨更添火药味。3 月,李在明因涉嫌城市开发腐败案、违规汇款至朝鲜以及选举期间作伪证等多项罪名被起诉。到了 9 月,他被正式逮捕,这一举动立即引发其支持者的强烈抗议。

支持李在明的阵营认为,这是尹锡悦政府赤裸裸的政治报复。而执政党则坚持这是依法办事,强调司法程序的独立性和必要性。这场争议迅速演变为全国性的政治危机,在首尔街头掀起了一波又一波的示威浪潮。

为什么李在明多项官司缠身,依然获得大量民众支持?

不得不讲一下李在明的生平,他的崛起堪称韩国版的「美国梦」。

出身贫寒的他,父亲是一名普通矿工,家境并不富裕。更引人注目的是,他并未像多数韩国政治精英那样拥有显赫的教育背景,而是通过自学成功考取了律师资格,并在人权领域崭露头角。

在进入全国政坛之前,李在明在地方政府工作中展现出卓越的治理能力。先后担任城南市长和京畿道知事期间,他推行了一系列惠民政策,建立了良好的政绩口碑。

在传播方面,李在明在推特、Youtube、INS 发布日常动态,语言风格直白接地气,将个人政治主张与社会热点有效结合,这种沟通方式特别受到年轻选民的欢迎,帮助他突破了传统政治人物的刻板印象。

说到这儿,你是否想到了一个人?同样官司缠身却得到民众喜爱。没错,就是特朗普,很多人把李在明比做韩国的特朗普,作为韩国最大在野党共同民主党党首,背负 5 起刑事案件的李在明依然被视为角逐 2027 年韩国总统宝座的热门人选。

有韩媒近日发表题为《李在明能成为特朗普吗?》的观点文章,称美国当选总统特朗普能给李在明一些安慰,前者多项刑事案件缠身,仍然胜选。文章指出,在现代选举中,美国选民似乎越来越不重视道德、正义等价值观,在韩国也是如此。

11 月 25 日,李在明「教唆伪证」案在韩国首尔中央地方法院一审宣判,李在明被判无罪。

宣判前的周末, 11 月 23 日,在首尔光华门附近,「进步派」与「保守派」支持者唱对台戏。「进步派」集会要求「尹锡悦总统辞职」,「保守派」集会要求「逮捕李在明」,两边阵营相距不足一公里,集会人数逾万人。

与此同时,现任总统尹锡悦的支持率跌至仅 17% ,创下历史新低。

虽然韩国政府一直以来都因腐败传闻而备受质疑,但支持率跌破 20% 的情况极为罕见。这表明总统几乎已经失去了对政府的有效控制。

相反,李在明在被起诉并遭到逮捕后,他不仅没有失去民众支持,反而因为「政治迫害」的论述获得了更多同情和支持。

韩国加密投资者@Yusoff Kim 认为,虽然官方声明中提到「国家安全」作为主要理由,但许多人认为此举更多是为了巩固总统本人在当前危机中的权力地位。

对于尹锡悦宣布戒严,李在明表示,尹锡悦总统非法宣布戒严无效,从现在起,尹锡悦不再是大韩民国总统,他也呼吁韩国民众前往国会,保护国会。

这场政治较量的影响远超出个人恩怨的范畴。它加深了韩国保守派和进步派的对立,也暴露出韩国民主制度中的诸多争议性问题。尹锡悦代表的保守派国民力量党和李在明领导的进步派共同民主党,在政治理念和国家发展道路上存在根本性分歧。

当下的韩国社会,因这场持续发酵的政治争端而陷入更深的分裂?李在明案件的司法进程仍在继续,但其政治影响已然超出法庭范围,成为考验韩国政治文明和社会稳定的试金石。