原文作者:Coingecko

原文编译:Felix, PANews

近日,Coingecko 发布了关于美国加密执法行动的研究报告,该研究基于 2019 年 1 月 1 日至 2024 年 10 月 9 日的官方公告,研究了加密公司与美国监管机构在联邦和州法院案件中达成的货币价值和解,但不包括针对个人提出的指控。以下为报告详情。

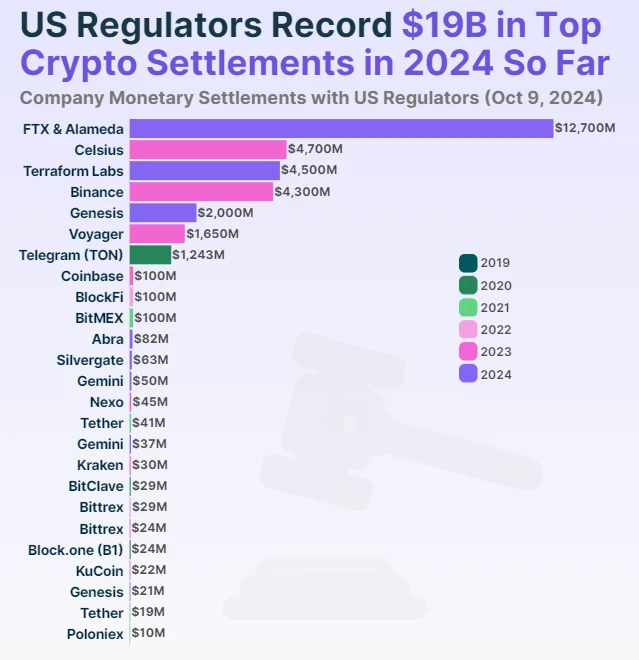

和解金累计近 320 亿美元,FTX 和 Alameda 占近四成

美国监管机构开展的最主要加密执法行动是针对破产的加密交易所 FTX 及其附属交易公司 Alameda,这两家公司共同支付了迄今为止最大的和解费用 127 亿美元。FTX 和 Alameda 的诉讼由商品期货交易委员会(CFTC)牵头,和解协议于 2024 年 8 月宣布,距离 FTX 倒闭不到两年。虽然这一判决不包括 CFTC 对个别公司高管的诉讼,但这笔 127 亿美元的和解金将用于偿还 FTX 客户和债权人(约 112 亿美元)。

美国监管机构第二大加密执法行动是针对破产的加密贷款机构 Celsius(47 亿美元)、前行业领导者 Terraform Labs(45 亿美元)和加密交易所 Binance(43 亿美元)。值得注意的是, 2022 年年中 Celsius 和 Terraform Labs 的倒闭是标志着加密市场牛转熊的关键事件,最终导致了 FTX 的下跌,引发了美国新一轮的监管审查。

币安的和解对美国监管机构来说是一项里程碑式的胜利,尽管在和解金额上仅排第四,但却是迄今为止唯一一家支付数十亿美元和解金的运营中的加密公司。这家全球领先的加密交易所于 2023 年 11 月同意认罪,以解决与包括司法部(DOJ)、财政部和商品期货交易委员会(CFTC)在内的多家美国监管机构的诉讼。

目前美国监管机构采取了 25 项加密执法行动,并且每次和解金额均超过 1000 万美元。总体而言,美国监管机构对加密公司的最高和解金额累计达到 319.2 亿美元。

过去两年执法行动激增,仅今年和解金超 194 亿美元

在美国 25 项主要的加密执法行动中,有 16 项是在过去两年内达成的和解,反映出自 2022 年底 FTX 崩盘以来监管审查力度加强。具体而言,美国监管机构在 2023 年解决了 8 起诉讼,总金额为 108.7 亿美元,创历史新高,与前一年相比,和解金额增长了 8327.1% 。

随后,美国监管机构已在 2024 年达成另外 8 项和解,价值 194.5 亿美元,几乎占和解总金额的三分之二。即使今年只剩几个月, 2024 年的和解金额也已经比 2023 年增长 78.9% 。鉴于美国监管机构没有放缓加密行业审查的迹象, 2024 年可能会比去年有更多的诉讼和解记录。

而在 2019 年至 2022 年期间,美国监管机构则赢得了 8 起加密诉讼和解。2019 年底,美国监管机构与 EOS 背后的公司 Block.one(现已更名为 B 1)达成了首起重大加密货币诉讼和解。美国证券交易委员会(SEC)与 Block.one 达成了 2400 万美元的和解协议。

SEC 在 2020 年又赢得了两起重大加密诉讼,其中IC0发行人 BitClave 在 5 月达成了 2934 万美元的和解,Telegram 就其子公司 TON Issuer 旗下的 Gram 代币发行达成了 12.4 亿美元的和解。12.4 亿美元的 Telegram 和解包括 12.2 亿美元的非法所得和 1850 万美元的民事罚款。

在 2021 年的牛市中,美国监管机构成功地对知名行业参与者采取了三次加密执法行动。稳定币发行人 Tether 在 2 月份与纽约总检察长(NY AG)达成了 1850 万美元的和解协议,随后在 10 月份与 CFTC 达成了 4100 万美元的和解协议,声称 USDT 完全由美元资产支持。CFTC 还与 Tether 的母公司 Bitfinex 达成和解,对非法交易的罚款较低,为 150 万美元。与此同时,加密交易所 Poloniex 和 BitMEX 在 8 月份分别以 1039 万美元和 1 亿美元达成和解。

2022 年,加密货币借贷机构 BlockFi 与美国 SEC 和北美证券管理员协会(NASAA)达成了 1 亿美元的和解协议,而加密货币交易所 Bittrex 与财政部达成了 2900 万美元的和解协议。