Снижение количества пользователей блокчейна биткоина, на которое обратил внимание аналитик Тимоти Петерсон, указывает на падение курса криптовалюты.

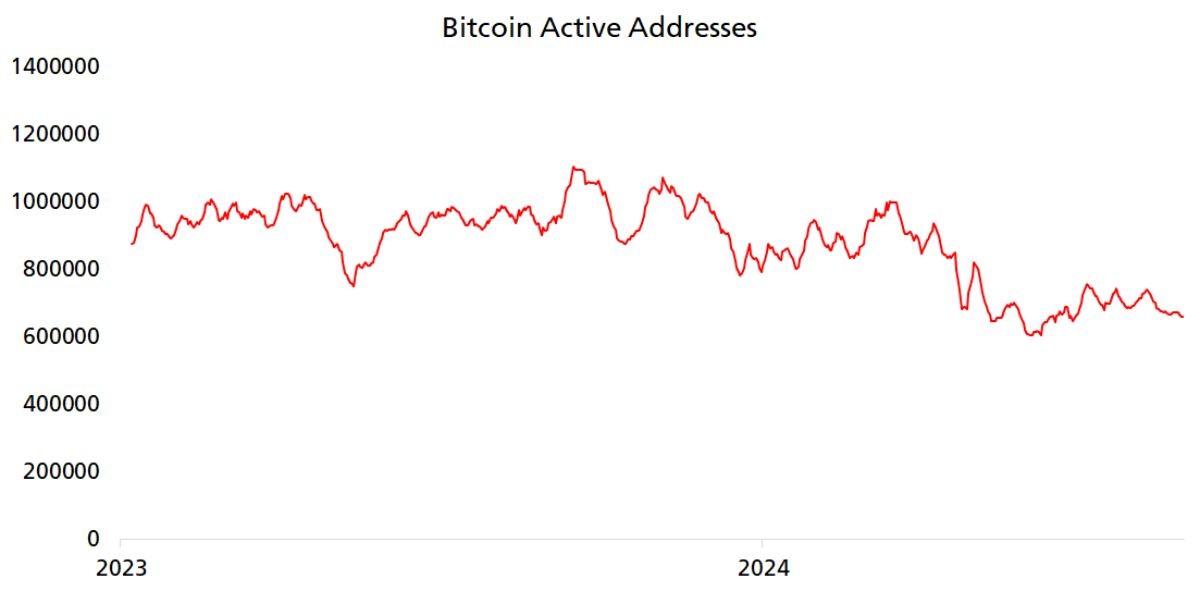

Петерсон опубликовал график, на котором видно, что число активных адресов в сети BTC резко пошло вниз в начале весны после того, как цена монеты обновила исторический максимум на отметке $73 794 и стала падать. К лету ситуация стабилизировалась, но на данный момент количество пользователей блокчейна примерно на 28% уступает мартовскому показателю.

Изменение количества пользователей сети биткоина в сутки

Как правило, снижение активности пользователей блокчейна сигнализирует о грядущем дампе на фоне падения интереса к криптовалюте.

Ситуация, возникшая в 2024 году, не стала исключением из этого правила. Как только количество криптокошельков, с которых отправляли монеты, начало уменьшаться, курс BTC тоже пошёл вниз и на протяжении последних пяти месяцев колебался в рамках нисходящего канала.

На основании этого можно предположить, что стоимость монеты будет колебаться в диапазоне от $50 000 до $68 000 до середины октября.

Нисходящий канал на графике изменения курса биткоина

Тимоти объяснил падение активности пользователей сети BTC выпуском биткоин-ETF в США. Он полагает, что вместо того, чтобы совершать операции с криптовалютой, некоторые инвесторы начали вкладывать деньги в деривативы, а эмитенты фондов копят монеты в криптохранилищах и не выводят их оттуда.