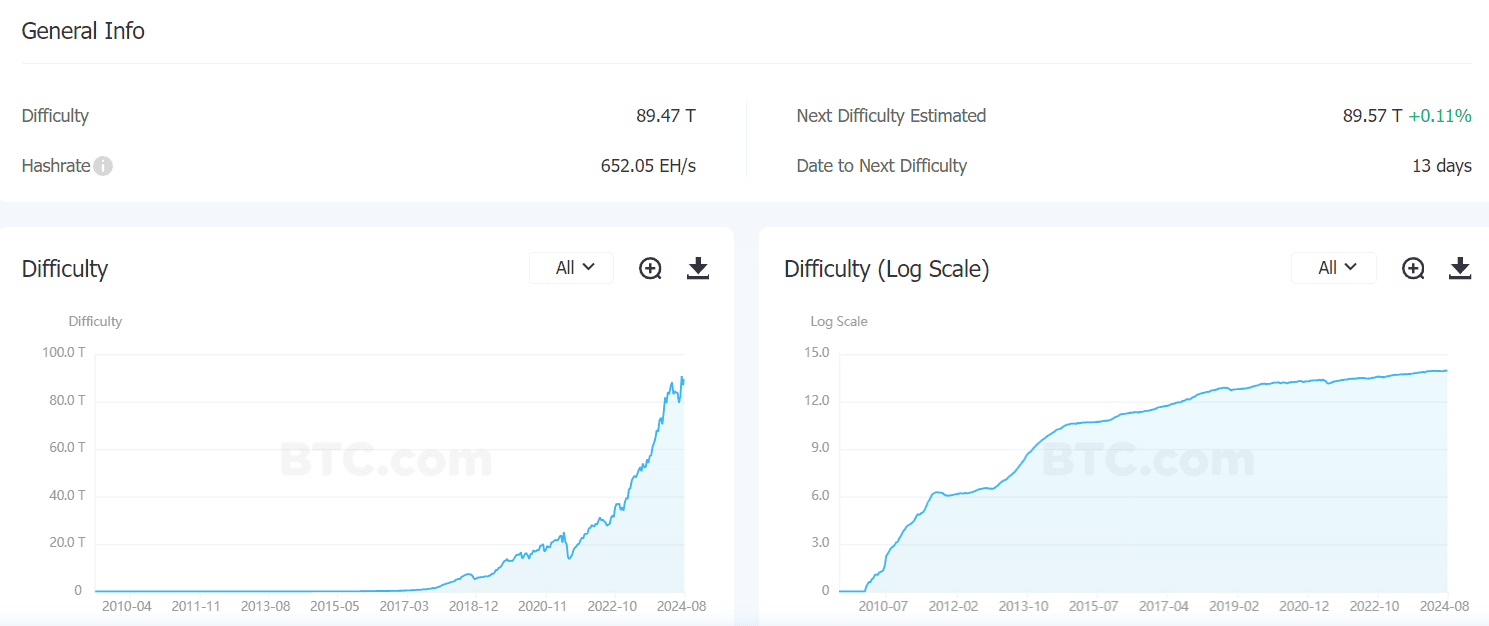

- 28 августа показатель сложности майнинга первой криптовалюты увеличился на 2,99%.

- На текущий момент он держится на уровне 89,47 T.

- Средний хешрейт в сети биткоина составляет 743,28 EH/s.

28 августа 2024 года сложность биткоин-майнинга достигла отметки в 89,47 T. Иными словами, показатель увеличился на 2,99%, по данным BTC.com.

Средний хешрейт в сети биткоина составляет 743,28 EH/s. При прошлом изменении сложности он держался на уровне 641.08 EH/s.

Согласно имеющимся данным, в следующий раз показатель сложности биткоин-майнинга может увеличиться до 89,57 T. Прирост в процентном выражении при этом составит 0,11%.

Напомним, что сложность майнинга — это определение необходимой совокупной мощности оборудования для добычи криптовалюты. Если она растет, это может свидетельствовать об увеличившейся активности среди майнинговых компаний. В случае падения показателя ситуация выглядит противоположным образом.

Увеличение сложности приближает дату следующего халвинга первой криптовалюты. В последний раз он состоялся в апреле 2024 года и стал четвертым по счету сокращением вознаграждения за добычу блока биткоина вдвое.

Следующий перерасчет показателя должен произойти через 13 дней — 11 сентября 2024 года.

Напомним, мы писали, что в секторе биткоин-майнинга началась фаза консолидации.