原文作者:xparadigms & wowitsjun_(hashed_official)

原文编译:深潮 TechFlow

* 这是四部分系列文章的第三部分,探讨当前扩展比特币生态系统的解决方案。

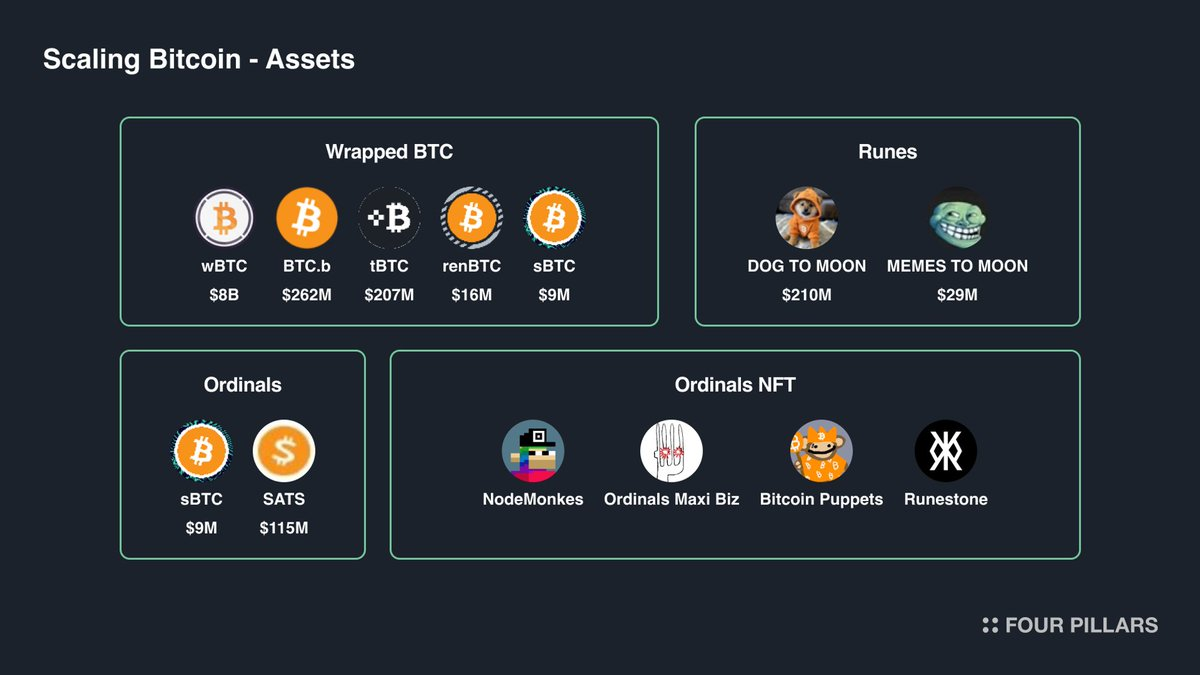

在整体加密货币市场中,比特币拥有最有价值的品牌和资产,其资产类别不仅限于其本土的 BTC。比特币不仅可以被包装并发送到其他区块链使用,还包括比特币铭刻资产,如 Ordinals 和 Rune 协议。此外,比特币还拥有一个不断扩展的 NFT 市场,NFT 是通过 Ordinals 协议发行的。

在这篇观点文章中,我们将探讨比特币生态系统中的资产类别以及每个资产类别的表现。

1. 背景 - 桥接 BTC 和比特币代币协议

1.1 桥接 BTC

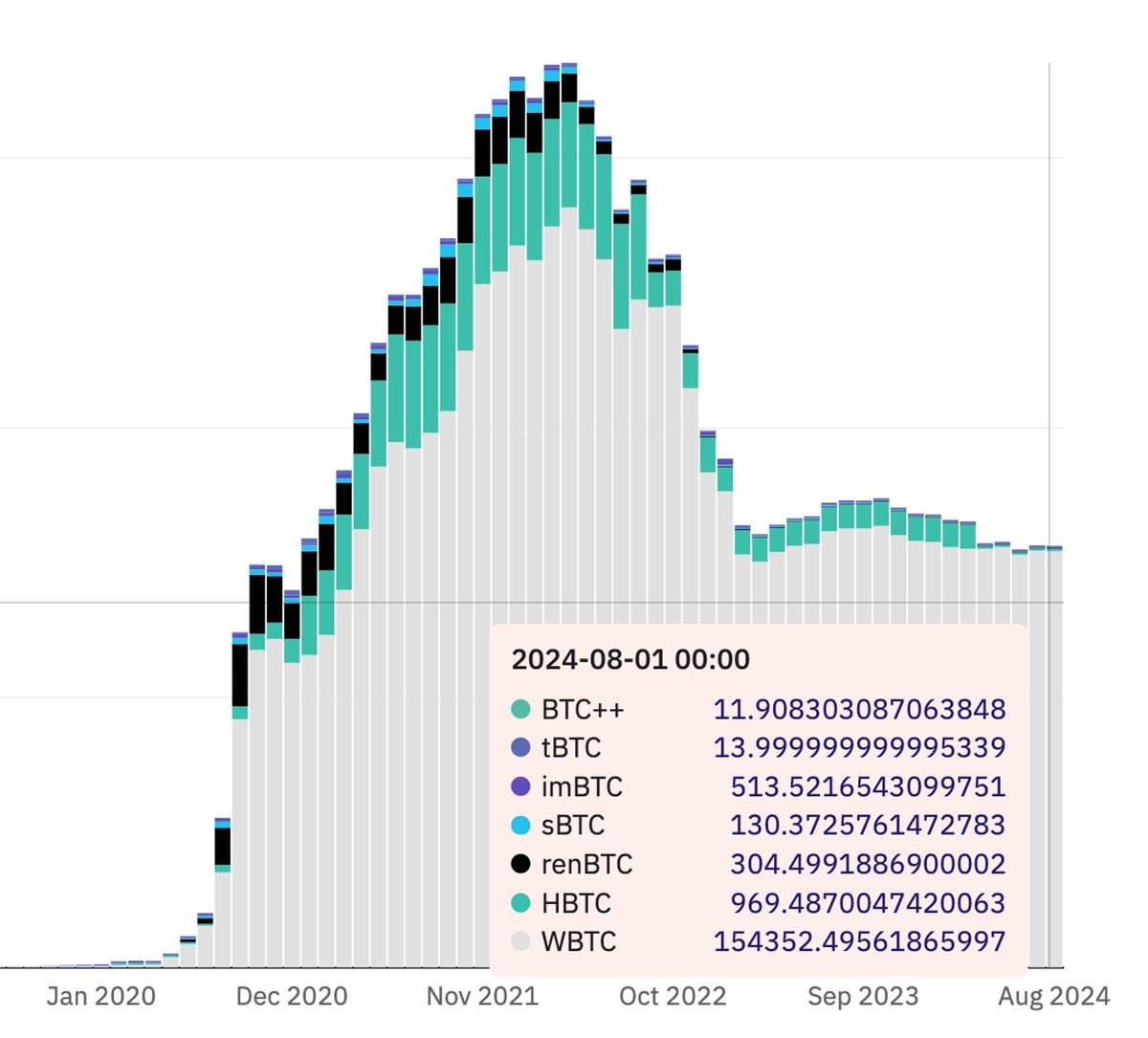

截至 2024 年,比特币仍然是市值最大的加密货币,总价值超过 1.3 万亿美元,占整个加密市场的 53% 。。然而,由于比特币在其本土生态系统中缺乏应用场景,因此它被桥接到其他基于智能合约的区块链上,称为桥接 BTC。桥接 BTC 指的是以 1: 1 比率包装或代币化的比特币,以便在其他区块链网络的去中心化金融(DeFi)中使用。

桥接 BTC 的例子包括 wBTC、tBTC 和 BTC.b:

Wrapped Bitcoin (wBTC):Wrapped Bitcoin 是以太坊区块链上的一种 ERC-20 代币,代表比特币。每个 wBTC 都由储备中的比特币以 1: 1 的比例支持,目前由 BitGlobal 操作。

tBTC:它通过一套智能合约和一个去中心化签名者网络来运作,这些签名者管理铸造和赎回过程。用户将比特币存入一个多重签名钱包,作为回报,他们在以太坊上获得等量的 tBTC。

BTC.b:这是另一种在 Avalanche 上的包装比特币,作为 LayerZero 的跨链代币标准。

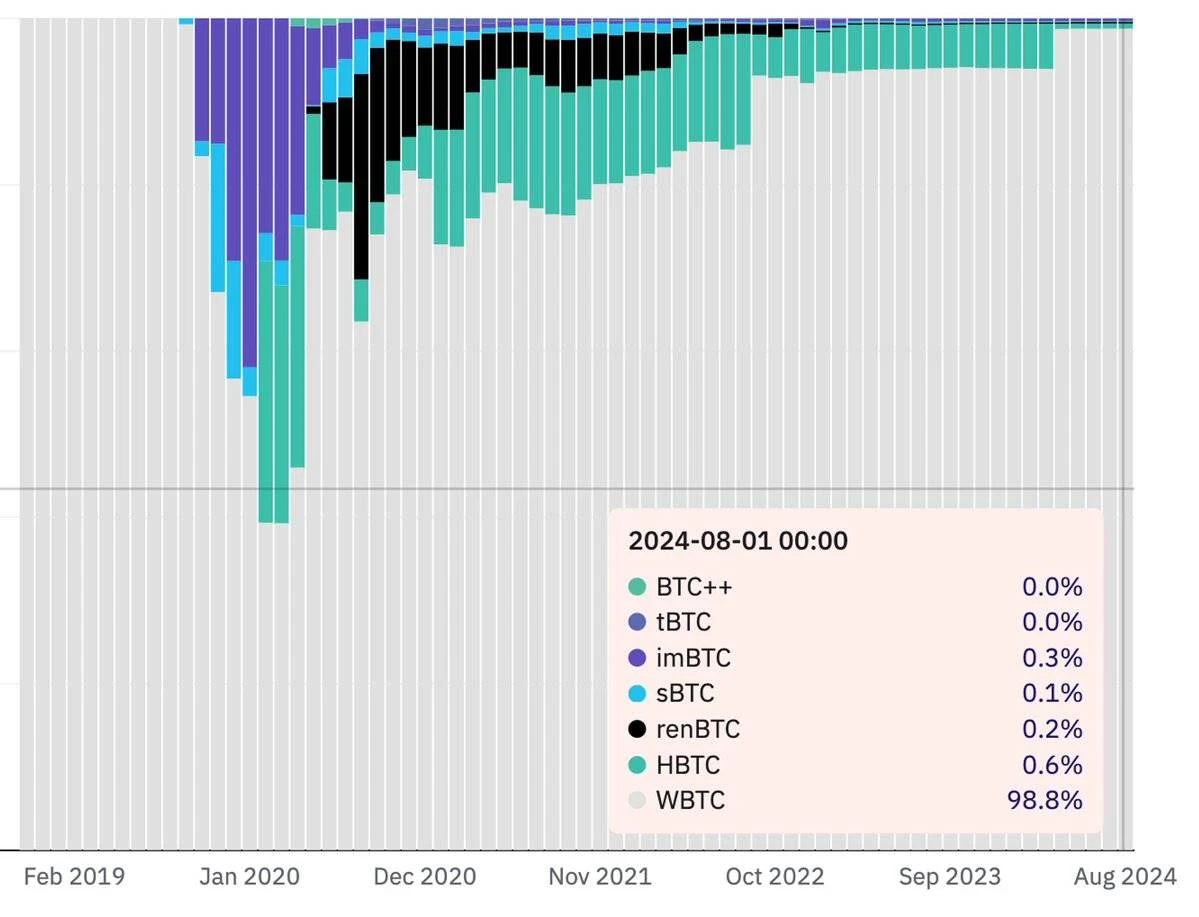

在这些桥接的 BTC 中,wBTC 占据了大多数供应,并已成为以太坊 DeFi 生态系统中的事实上的 BTC 资产。最近,BitGo 宣布与 Bit Global 在香港的合资企业,并计划将其支持 WBTC 的多重签名钱包的三把密钥中的一些分发给香港的 Bit Global。这引发了关于 wBTC 是否安全的辩论,并且正在讨论和潜在开发其他替代方案。

来源:btc on ethereum (WBTC, renBTC 等)

1.2 比特币代币协议 - Ordinals 和 Runes

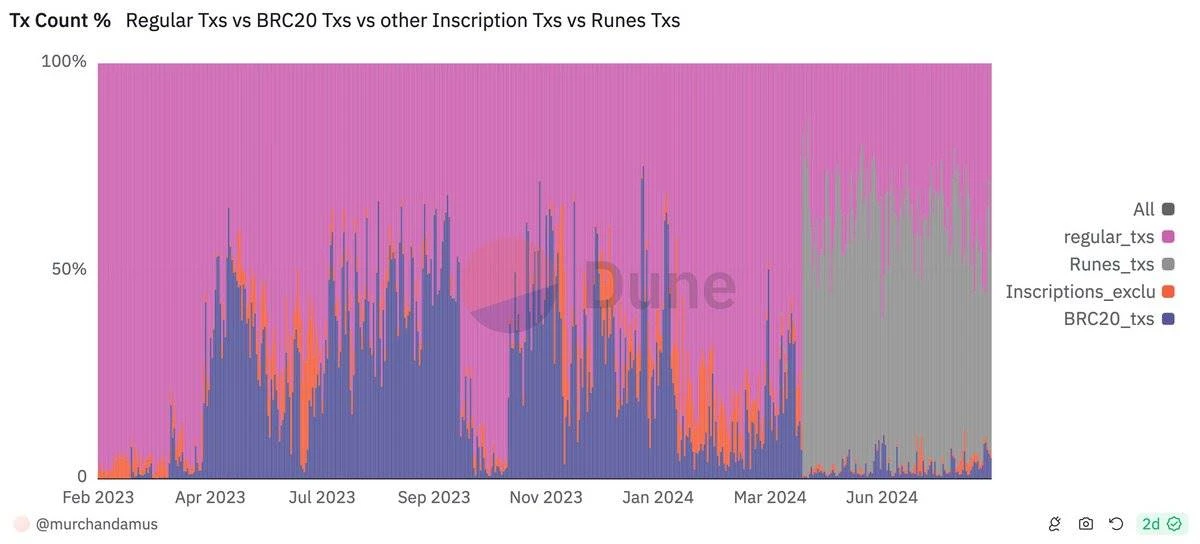

比特币铭刻资产,如 Ordinals 和 Runes,是直接在比特币区块链上铭刻的协议,利用其基础设施进行代币的创建和管理。这两个协议由 Casey Rodarmor 开发,突出了比特币区块链的不同用例,其中 Ordinals 专注于 NFT,而 Runes 则增强了比特币生态系统中可替代代币的可扩展性。

Ordinals 协议:Ordinals 协议于 2023 年 1 月推出,允许在比特币区块链上创建独特的数字资产,即 NFT,或可替代代币(BRC-20)。该协议允许用户将数据铭刻到单个 satoshi(比特币的最小单位)上,创造出一种新的数字收藏品形式。BRC-20 代币是一种类似于以太坊 ERC-20 的代币标准,但构建在比特币区块链上,而比特币 Ordinals 通常被视为 NFT 的一种形式。

Runes 协议:这是一个利用比特币 UTXO 模型的可替代代币标准。与 BRC-20 标准不同,后者由于“垃圾”UTXO 的激增导致网络拥堵,Runes 利用比特币固有的 UTXO 模型创建具有最小链上占用的代币。该协议使用比特币现有的 UTXO 模型,并结合一个允许在区块链上包含少量数据而不影响交易输出的脚本。嵌入在比特币交易输出中的专用结构称为 runestones,包含创建、铸造或转移代币的指令。这种方法允许更高效的数据存储,并减少网络膨胀的潜在风险。

来源:常规交易与 BRC 20 交易与其他铭刻交易与 Runes 交易

1.3 Ordinals NFT

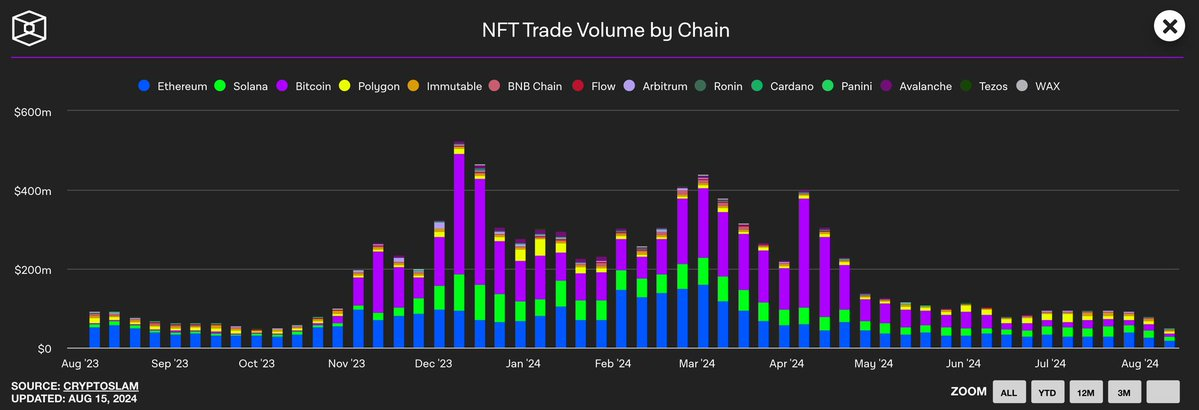

过去一年,比特币 NFT 市场经历了显著增长,尽管更广泛的 NFT 市场却在收缩。该领域正在成为比特币生态系统中一个显著的资产类别,形成了一个紧密的社区。

比特币 NFT 市场的扩展是由于对基于比特币的 NFT 日益增长的兴趣。根据 CryptoSlam 的数据,在按区块链划分的 NFT 历史交易量中,比特币位居第三,仅次于以太坊和 Solana。

2.总结 - 桥接 BTC 将面临激烈竞争,代币协议需要更好地发展

作者:xparadigms,来自 Four Pillars

2.1 关于桥接 BTC(例如 wBTC) - 新的桥接 BTC 将面临激烈竞争

比特币除了作为数字黄金以实现价格增值外,通常还作为桥接 BTC 被发送到其他区块链,以用作抵押或在 DeFi 协议中获得收益,尤其是在以太坊上。这使得 DeFi 用户能够轻松接触到 BTC。

本周,wBTC 的运营方宣布计划将部分控制权交给 Bit Global,这是由 Justin Sun 共同创办的合资企业。在三把多重签名密钥中,两把将由 Bit Global 处理,一把将由 BitGo 处理。由于 Justin Sun 在过去的项目(如 TUSD 和 stUSDT)中并未完全透明,公众对由于 Justin Sun 的“声誉风险”而产生的“保管风险”表示担忧。由于 wBTC 占据了以太坊中超过 95% 的比特币资产,这可能对生态系统产生负面影响,如果处理不当,可能导致与其他桥接 BTC 相比出现折扣。

现在这个问题已经被识别,更多项目可能会尝试进行市场宣传(例如 tBTC、BTC.b),并创建新的包装比特币(例如 Coinbase cbBTC)。

来源:btc on ethereum (WBTC, renBTC, more)

2.2 比特币代币协议 - “目前,这仅仅依赖于社区驱动”

大多数比特币铭刻资产,如 meme 币,缺乏产生收入或增值的方式,因此它们高度依赖于社区的兴趣。这意味着如果市场情绪下降,整体市场可能会遭遇崩溃。例如,ORDI 并不产生传统的收入,其价值主要来源于市场投机以及对 Ordinals 协议和 BRC-20 代币的关注。虽然 Ordinals 的使用增加了交易费用,从而使比特币矿工受益,但这并不会直接为 ORDI 本身带来收入。这种对社区热情的依赖使得这些资产变得非常不稳定,如果社区兴趣减弱,它们的价值可能会迅速下滑。

随着比特币二层(L2)技术的发展,改善用户在创建和交易比特币代币时的体验,可能会吸引更多的关注,就像在比特币上推出一个 pump.fun 版本一样。为了让这些比特币代币协议得以蓬勃发展,仍需进行进一步的开发。