来源:币界网

作者:Web3嗅观察

昨天新出的Meme“金狗”代币DOGS,疯狂传播刷屏,社群,推特KOL和TG到处是这个DOGS的bot 邀请链接。该项目到底什么来头?怎么领取空投?本文给您详细解读。

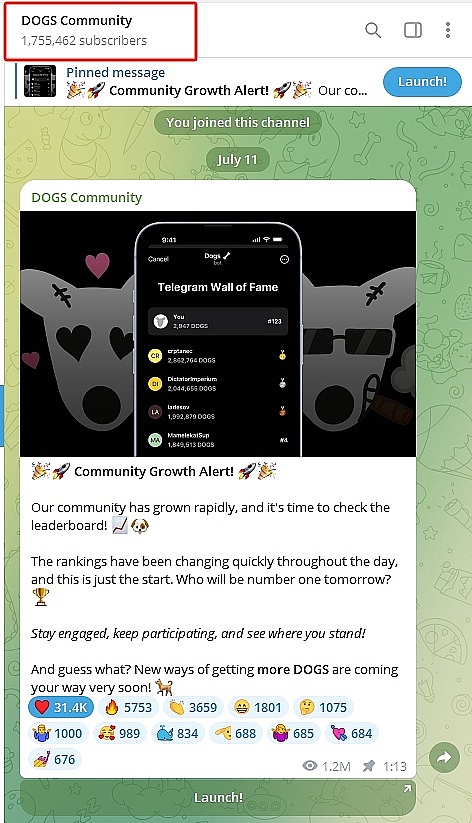

Telegram &TON生态新成员——Meme币DOGS通过电报领空投、邀请用户机制等,其上线不到24 小时,便迅速达到了一百万以上用户。截止目前,DOGS的TG频道已经突破175万人。这个搭载在TON 和Telegram 上的项目,用户增长速度惊人。

DOGS利用其强大的电报“病毒传播”空投模式,目前热度仍在持续升温中。DOGS的黑白狗形象灵感源自TON的创始人Pavel Durov制作的吉祥物Spotty。官方称,DOGS 是最具Telegram 本土特色的Meme币,旨在将Spotty 作为吉祥物代表的精神和文化,带入加密货币的世界中,创造出一个有趣、由社群驱动的、独特的新项目。

无成本、无门槛参与领取DOGS空投

DOGS 空投可以说是专门给电报用户准备的,只要有电报账号就可以领取,玩法简单粗暴。

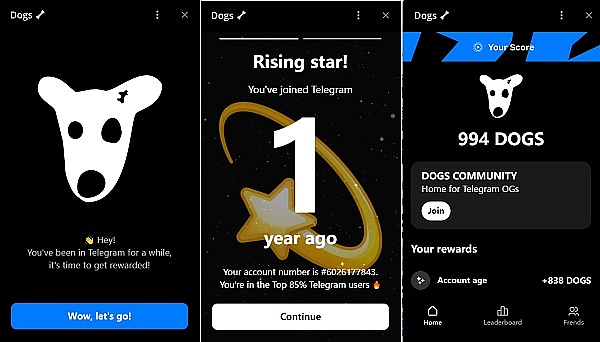

目前,参与DOGS空投非常简单,用户只需加入DOGS 的Telegram Bot频道,该Bot 会根据用户的TG 帐户资料(如使用年限、是否为Premium 会员等)空投DOGS 代币。

机器人会自动分析你的TG电报账号,根据注册时间、活跃度来给你账号评级,再根据等级分发积分。另外,开通了Premium 的账号还有额外积分奖励。通过邀请朋友加入也能获得额外的积分。

据小编实测,绝大部分用户都拿800-3000左右积分,例如,注册1年的电报账号,加入频道后可以获得990积分,注册 4 年的电报账号,可以获得 3000积分左右。

然而,这些代币积分目前还只是数字,未来是否会有价值还有待观察。如果想赚取更多的DOGS,可以通过邀请更多新人来获得,这也是其病毒传播迅速的原因之一。

需要提醒的是,目前这些只是积分,并不能立即兑换成代币,具体的兑换比例尚未公开。关于DOGS积分如何兑换成代币,以及更多的玩法细节,我们将持续关注。预计到时候电报用户可能需要注册一个TON链的钱包,然而充值TON以申领代币。目前这些细节未知。

TON生态Meme币的再度破圈

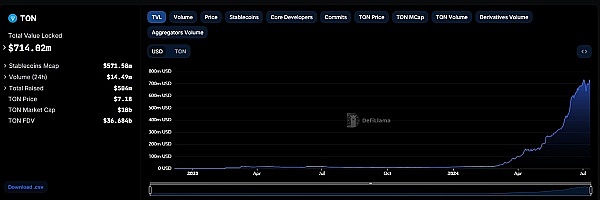

由于TON依托于Telegram庞大的用户基础(超过9亿活跃用户)和强大的社交网络效应,其社区和生态发展迅猛。今年以来,TON链的成长态势显著,其总锁仓量(TVL)不断创下新高。

据DefiLlama数据显示,截至7月11日,TON网络的TVL锁仓量已突破7.14亿美元。TON(Toncoin)代币的市值已达到179亿美元,全球市值排名第八。

近期,人们对TON生态系统再度破圈的期望主要集中在Memecoin上。在这轮行情中,Memecoin在市场动荡中的优质弹性,以及Notcoin引领的TON生态出圈效应,吸引了大量散户押注Meme+TON这一组合。今年,这两个强势概念的结合不断引发市场遐想。

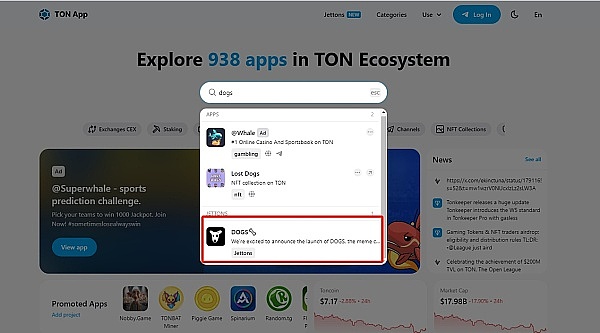

虽然TON生态系统中还有一些Meme项目,如FISH和REDO等,但它们尚未实现破圈和带来显著的财富效应。TON的基因和特色更注重小游戏、支付应用和跨境电商等Web2和Web2.5领域,而在DeFi和Meme领域则相对薄弱。

在TON生态缺乏代表性Meme项目的情况下,病毒传播的黑白狗DOGS似乎有潜力成为依赖Telegram快速传播的文化符号。在市场短期重新洗牌的时期,这样的Meme项目无疑值得每个玩家给予更多关注。