Source: Cailian Press

On Monday Eastern Time, the eagerly awaited Q1 US stock portfolio adjustment report (13F) for the fund "Situational Awareness LP," managed by the much-watched Wall Street newcomer, 24-year-old Leopold Aschenbrenner, was finally released. (Related Reading: Liquidated NVIDIA, Frenzied Buying of Fuel Cells: The 'Physical Arbitrage' Logic of a 24-Year-Old Investment Prodigy)

As described in our previous report, as the world's youngest manager of a mega-fund, Leopold Aschenbrenner foresaw the importance of AI infrastructure "logistics" as early as 2024, making significant investments in power, land, and infrastructure, propelling his fund to massive expansion in less than two years since its inception.

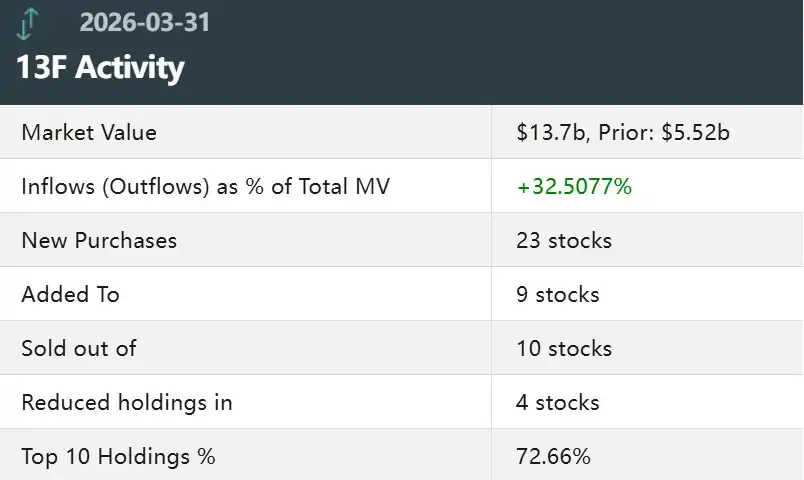

This belated report shows that the market value of the fund managed by Leopold Aschenbrenner has surged from $5.52 billion in the previous quarter to $13.7 billion—and just under two years ago, the fund's initial AUM was only $255 million.

Such a rocket-like surge in assets under management indicates that the "Situational Awareness" fund has clearly become a star fund highly sought after on Wall Street—in fact, Leopold Aschenbrenner's portfolio moves have already become one of the most closely watched sources for "copying homework" among Wall Street institutions and retail investors in recent quarters.

Let's take a closer look at what this Wall Street star has done in the first quarter of this year.

Heavily Buys Short Positions in Chipmakers

From this adjustment report, the most significant move made by Leopold Aschenbrenner in Q1 was heavily shorting chipmakers.

As of the end of Q1, the fund aggressively purchased put options with a notional value of up to $8.46 billion, covering numerous chipmaker stocks, including a $2 billion put option on the VanEck Semiconductor ETF (ticker: SMH) and a $1.6 billion put option on AI giant NVIDIA.

Massive Purchase of Chip Put Options

Additionally, the fund established put option positions on Broadcom, Oracle, AMD, Micron Technology, ASML, Intel, Corning, and TSMC.

These bearish options are not only among the fund's top five purchases for Q1 but also rank among its top five holdings. This undoubtedly highlights Leopold Aschenbrenner's pessimistic outlook on the prospects of chip stocks.

However, Leopold Aschenbrenner is not bearish on all chip stocks.

In Q1, the fund slightly increased its holdings of memory giant SanDisk by 80,000 shares and established a SanDisk call value option position worth $380 million, possibly hinting that it expects the memory boom to continue and that the fund is making selective bets within the semiconductor industry.

Still Heavily Betting on Energy and AI Infrastructure

As of the end of Q1, US biofuel company Bloom Energy (ticker: BE) remained Aschenbrenner's largest bullish bet on an individual stock. His fund holds 6.5 million shares of Bloom Energy, valued at $879 million, and holds 409,000 Bloom Energy call options with a notional value of $55 million.

Furthermore, Situational Awareness increased its holdings in cryptocurrency mining/data center operators CleanSpark (ticker: CLSK), Riot Platforms (ticker: RIOT), Applied Digital (ticker: APLD), and IREN Limited (ticker: IREN).

As we previously analyzed, Aschenbrenner's bet on Bitcoin miners is not for cryptocurrency speculation but for the ready-to-use land, power, and grid permits held by these miners. In the era of massive AI infrastructure expansion, these resources are equivalent to "ready-made" AI infrastructure, saving years of approval time.

A Belated 13F Report

It is worth noting that Aschenbrenner's 13F filing was originally due last Friday—according to regulations, all institutional investment management companies holding securities over $100 million must submit this disclosure document to the U.S. Securities and Exchange Commission within 45 days after the quarter ends—but Situational Awareness did not submit the report until Monday morning.

Typically, late or missed 13F filings can lead to civil penalties at the SEC's discretion, ranging from small fines to a maximum of $750,000.

However, investors' attention is certainly focused on Aschenbrenner's specific portfolio adjustments.

Overall, while he aggressively established semiconductor put option positions in Q1, his fund still holds a significant amount of highly volatile tech stocks and continues to make selective investments in computing, memory, and data center infrastructure. This adjustment trend might be worth investors' reference.