下周, 8 个项目迎来代币解锁事件。ARB 将解锁约 23.9 亿美元代币,此外 APT、CYBER、APE 将有高比例解锁,其余项目解锁比例与金额均较小。

具体解锁详情如下:

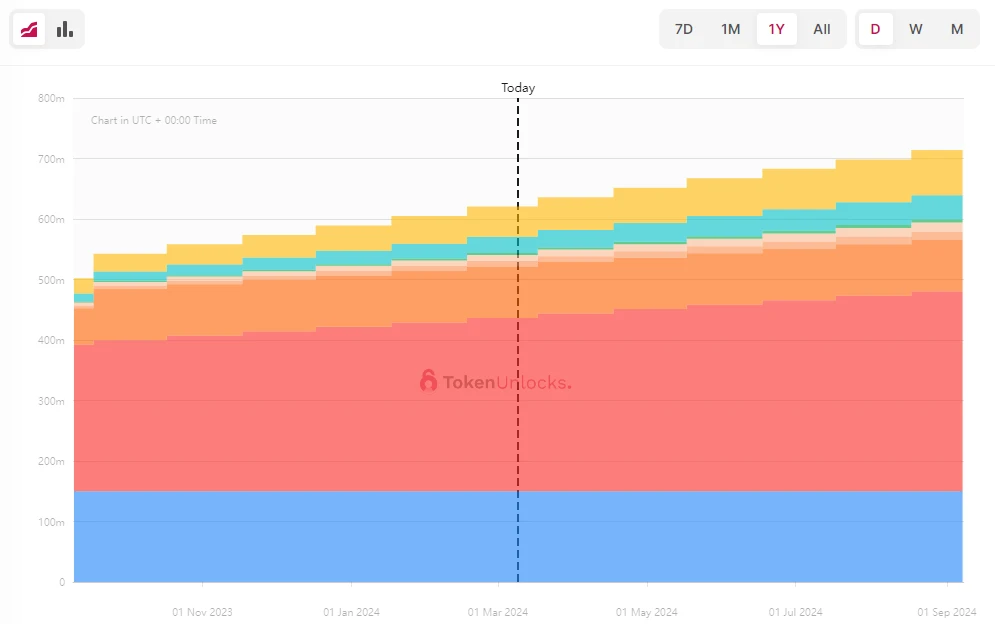

Arbitrum

项目推特:https://twitter.com/arbitrum

项目官网:https://arbitrum.io/

本次解锁数量: 11.1 亿枚

本次解锁金额:约 23.9 亿美元

Arbitrum 是以太坊 Rollup ,旨在提高以太坊的可扩展性,它在向以太坊主网提交单个交易之前聚合和处理链下交易。这意味着用户可以享受更快、更便宜的交易,同时仍然受益于以太坊网络的安全性和去中心化。Arbitrum 的原生代币为 ARB。 ARB 持有者可以参与决策过程,例如对协议升级或变更提出提案和投票。

本轮解锁将面向两类对象,分别为团队和顾问的 6.735 亿枚,价值约 14.5 亿美元,以及投资者的 4.38 亿枚,价值约 9.42 亿美元。

具体释放曲线如下:

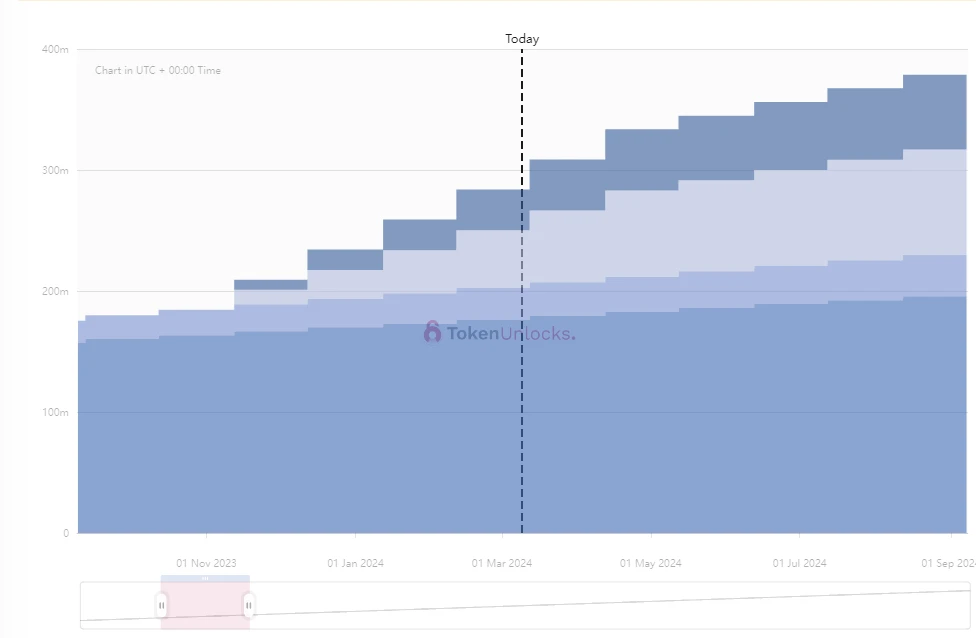

Aptos

项目推特:https://twitter.com/Aptos_Network

项目官网:https://aptosfoundation.org/

本次解锁数量: 2481 万枚

本次解锁金额:约 3.36 亿美元

Aptos 是 Layer 1 公链项目,其目标是建设一个可扩展、安全、可信任和可升级的智能合约平台。Aptos 团队由前 Meta 成员独立出来的。APT 为 Aptos 主链的原生代币,用于支付交易手续费、验证抵押及治理。

本次解锁主要面向核心贡献者和投资者,将向前者分配 1188 万枚 APT,价值约 1.57 亿美元,向投资者分配 842 万枚 APT,价值 1.11 亿美元。其余部分为社区的 321 万枚和基金会的 133 万枚。APT 初步进入膨胀加速期,今年仍将有持续相似量级的解锁。

具体释放曲线如下:

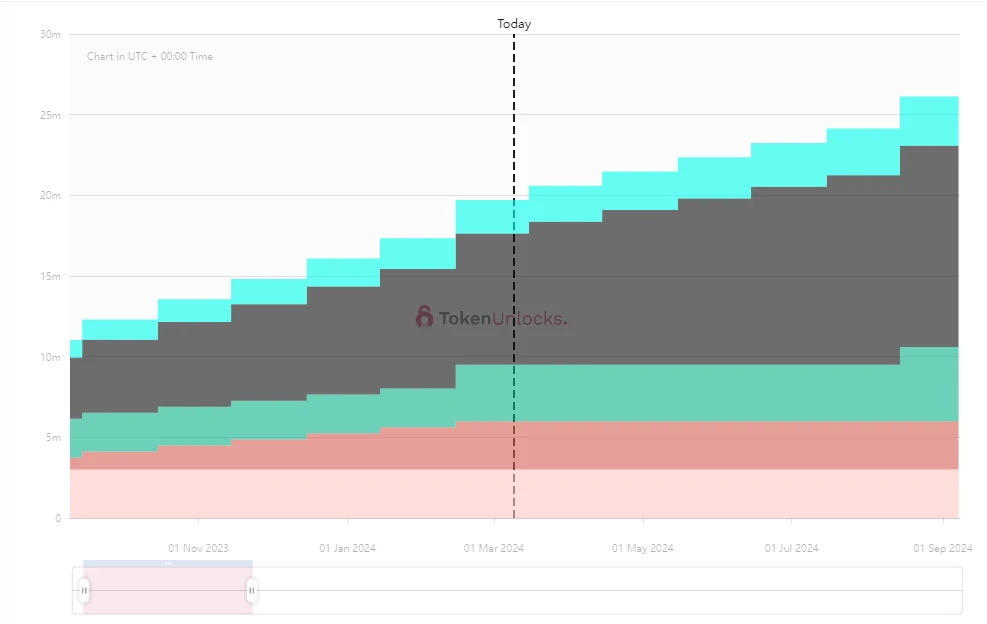

CyberConnect

项目推特:https://twitter.com/CyberConnectHQ

本次解锁数量: 88 万枚

本次解锁金额: 1061 万美元

CyberConnect 是一种基于区块链技术的去中心化社交图谱协议。CyberConnect 构建了一个统一的社交图谱,用户可以将自己的身份信息、社交关系等迁移到不同的网络和平台,同时这些个人数据也完全归用户所有,从而为用户创造价值。CyberConnect 协议的治理代币是 CYBER,用例包括投票治理,支付 Gas 费等。

本次释放主要面向生态发展基金,释放金额为 821 万美元,其余为面向社区财库的 185 万美元。CyberConnect 今年将保持相同的释放速率解锁,因当前已流通代币占比仅 20% ,故或将带来持续性的抛压。

具体释放曲线如下:

ApeCoin

ApeCoin(APE)是 APE 生态系统的 ERC-20 实用与治理代币,用于支持去中心化的 APE 社区的建设。

APE 由 ApeCoin DAO 管理,得到 APE 基金会的支持。借助 APE,代币持有者可以对 DAO 中的治理提案投票,并使用 APE 生态系统的独家功能(如游戏、活动和服务)。

项目推特:https://twitter.com/apecoin

项目官网:https://apecoin.com/

本次解锁数量: 1560 万枚

本次解锁金额: 3463 美元

本轮释放面向较多,包括创始人、贡献者、慈善贡献、财库等共 6 类对象。Aptos 当前已解锁量占总量的 62.05% ,本年将保持类似的速率持续释放,构成小量抛压。

具体释放曲线如下: