原创 | Odaily星球日报

作者 | 夫如何

2023 年第四季度会是新牛市开始的时间点吗?

宏观层面,美联储的利率维持稳定,并时有 2024 年降息的消息传出,为市场提振;美 SEC 对比特币现货 ETF 批准预期不断加持投资者的信心,让 2023 年Q4的加密市值不断走高。

从加密市场内部来看,美 SEC 和币安的和解,为整个加密市场走向主流提供一定的基础;比特币生态的崛起,头部生态铭文 ORDI 不断突破新高;铭文浪潮接二连三的到来,逐渐从 MEME 性质走向功能性,同时各大公链的打铭文热度居高不下,铭文成为检验公链知名度的标的之一。

从数据上来看,比特币突破 42500 大关,ETH 和 BTC 的汇率也有一定的提升。

可以说, 2023 年第四季度为新一年打下一个良好的基础。

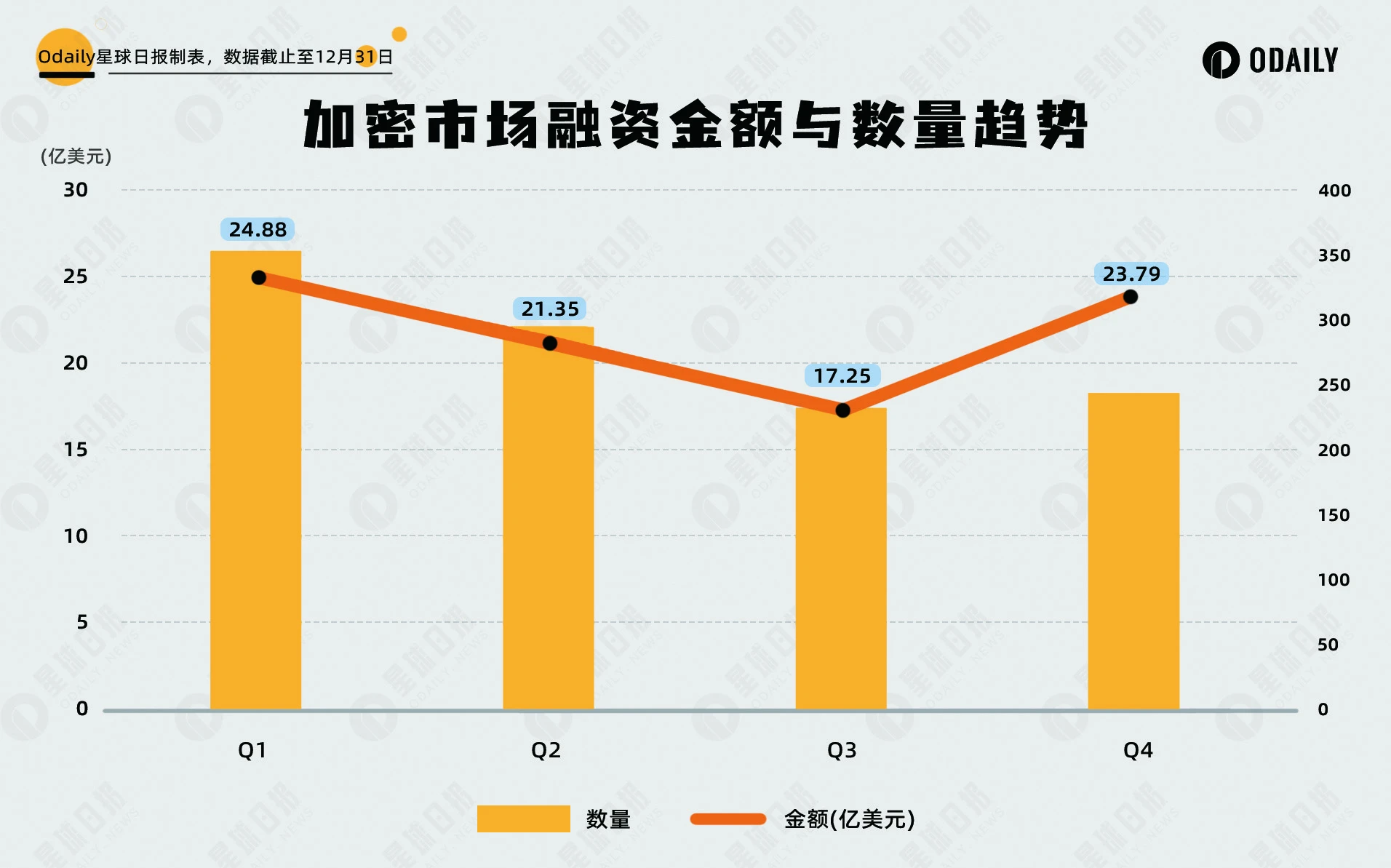

综合因素影响下,一级市场也迎来了拐点,Q4的投融资从数量和金额上都有一定幅度的上涨。但正逢年尾,各大知名机构出手减少。

回看 Q4 一级市场投融资活动,Odaily星球日报发现:

● 加密市场融资情况走好,拐点显现;

● Q4 融资数量为 243 笔,已披露融资总金额为 23.79 亿美元;

● 底层设施受 DePIN 板块的热度成为Q4投融资的赢家;

● 10 次以上投资为 OKX Ventures、Hashkey Capital 和 Waterdrip Capital。

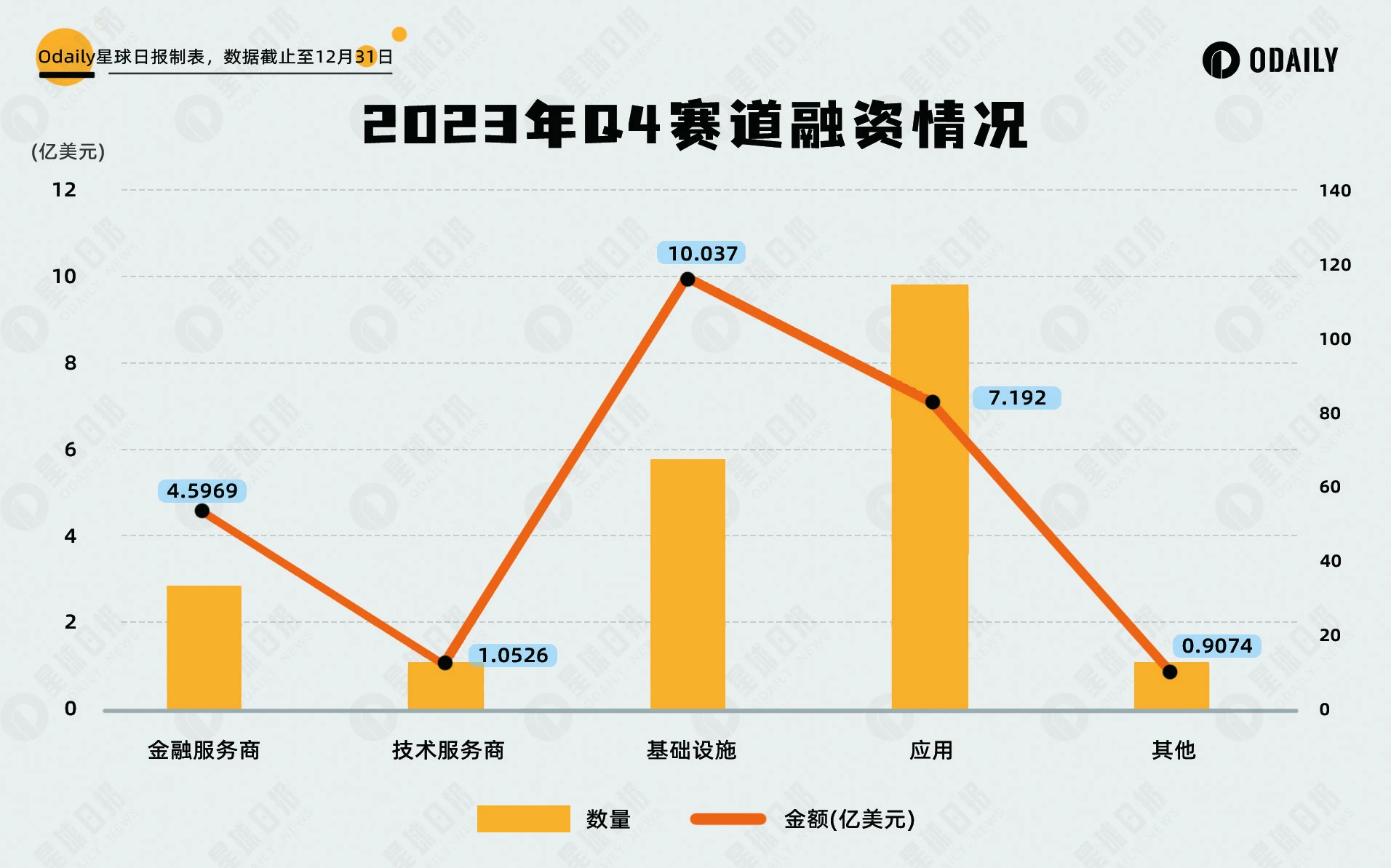

注:Odaily星球日报根据各个项目的业务类型、服务对象、商业模式等维度将 Q2 披露融资(实际 close 时间往往早于消息宣发)的所有项目划进 5 大赛道:基础设施、应用、技术服务商、金融服务商和其他服务商。每个赛道下又分为不同的子板块包括 GameFi、DeFi、NFT、支付、钱包、DAO、Layer 1、跨链以及其他等。

加密市场融资情况走好,拐点显现

如上季度报告所述,从 2022 年 1 季度到 2023 年 3 季度,全球加密市场融资事件及融资金额总体成下降趋势(不含基金募资及并购),但 2023 年Q4将整体趋势改变,环比 2023 年Q3融资金额增幅近 37.91% ,融资数量也有一定的提升。加密一级市场的融资情况的拐点似乎已经显现。

Q4 融资数量为 243 笔,已披露总金额为 23.79 亿美元

据 Odaily星球日报不完全统计, 2023 年 10 月至 12 月全球加密市场共发生 243 起投融资事件(不含基金募资及并购),已披露总金额为 23.79 亿美元,分布在基础设施、技术服务商、金融服务商、应用和其他服务商赛道,其中基础设施赛道获得的融资金额最多,约为 10.04 亿美元;应用赛道融资笔数最多,为 115 笔。

从上图来看,基础设施和应用依旧是机构投资最重要的板块,同时也为Web3提供多样化的选择;基础设施吸金能力显著提高,应用赛道的融资次数较上季度也有一定的上涨。

底层设施受 DePIN 板块的热度成为Q4投融资的赢家

据 Odaily星球日报不完全统计,Q4 细分赛道中融资事件集中在底层设施、DeFi 和 CeFi,占据总融资事件近乎一半比重,其中底层设施赛道为 43 笔,DeFi 赛道为 42 笔,CeFi 赛道为 33 笔。

从子赛道融资数量分布来看,投资风向趋于多元化,但 DeFi 和底层设施依旧是资本布局的重要地带。

从子赛道融资数量分布来看,投资风向趋于多元化,但 DeFi 和底层设施依旧是资本布局的重要地带。

Q4投融资从数量和金额两个角度来看,底层设施无疑是最大赢家,随着 DePIN 板块走入大众视野,机构也将重点放在底层设施赛道,据了解,机构和做市商将在明年重点关注 DePIN 赛道,将虚拟现实结合,才更符合Web2的用户习惯。

其次 DeFi 赛道,随着新链以及二层的不断推出,DeFi 的配套数量不断增多;launchpad 项目收到大多数机构的关注;铭文生态的 DEX 数量增长,预示着铭文作为新型资产模式正逐渐走向大众视野。

DeFi 赛道在Q4投融资数量增加,归功于比特币生态和二层生态的发展。

此外,CeFi 赛道的融资消息也很活跃,共有 33 笔,位列第三。CeFi 赛道的项目融资增多在一定程度上反应,传统市场的老钱正在加密世界布局,最适合他们的投资标的无疑是 CeFi。

单笔获投金额最大为 2.25 亿美元( Wormhole)

据 Odaily星球日报不完全统计,Q4细分赛道融资金额以底层设施为首,CeFi 为辅,其他赛道趋于平缓。底层设施赛道融资金额为 6.75 亿美元。

现阶段,总体融资量相对较低时,单一项目的融资金额对细分赛道的融资趋势产生较大影响,为了避免产生较大误差分析,Q4 融资金额分析将重点放在 TOP 10 项目介绍。下图各项目依照细分赛道划分,也囊括涉及加密业务的传统公司。

Wormhole 是一个去中心化的通用消息传递协议,使跨链应用的开发者和用户能够利用多个生态系统的优势。

LINE NEXT 由两家公司组成,韩国的 LINE NEXT Corporation 专注于全球 NFT 平台的战略规划,而美国的 LINE NEXT Inc.则负责开发和运营 NFT 平台业务。

Arkon Energy 是一家数据中心基础设施公司,使用过剩的可再生能源来运行比特币挖矿业务。

Blockchain.com 是一个数字资产平台,提供加密货币交易、区块链浏览器和加密货币钱包服务。Blockchain.com 还为机构提供一系列解决方案,如资产托管和贷款服务。

MapleStory(冒险岛)是一款免费、2D、横向卷轴大型多人在线角色扮演游戏,由韩国游戏巨头 Nexon 开发,该游戏 IP 已经拥有超过 38 万的稳定在线玩家群。

Fnality 成立于 2019 年,但起源于瑞银领导的区块链项目。它正在构建主要货币的数字版本,用于涉及数字证券的批量支付和交易。

YouTrip 主要为消费者提供多币种数字化钱包,为中小企业提供支持公司卡的商业账户服务。

Andalusia Labs 是数字资产风险基础设施提供商。它拥有三个主要的数字资产技术解决方案,其中包括一个名为 Karak 的第二层区块链、一个名为 Subsea 的加密风险管理市场和一个以安全为中心的机构平台 Watchtower。

Prove 是一家全球数字身份解决方案提供商,提供了一个身份验证和身份验证平台,致力于为用户提供商业支持和反欺诈相关服务。

Blockaid 是一个Web3安全工具,可以在恶意交易发生之前停止它们,保护Web3用户免受诈骗、钓鱼和黑客攻击。

OKX Ventures、Hashkey Capital 和 Waterdrip Capital 成为Q4出手最多的机构

在整体市场走好的环境下,知名机构的出手次数似乎并没有增多,或受年尾的原因,上季度出手较多的 Binance Labs 和a16z仅有 5 次左右的出手,反观 OKX Ventures、Hashkey Capital 和 Waterdrip Capital 出手达到 10 次。

纵观知名机构在Q4投融资的项目中着重偏向于底层设施和 DeFi 赛道。虽然占比有些许不同,但总体上和上文描述的情况一致。