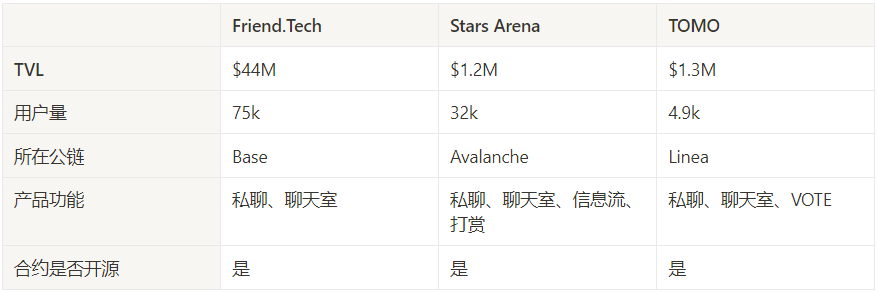

Friend.Tech带动的Socialfi狂潮席卷各个公链,每条链上基本都产生了仿盘,也都掀起了不错的热度,比如Avalanche上的Stars Arena,和Linea上的TOMO。这篇将从产品体验、数据等方面将FT与这两个仿盘进行对比。01Friend.Tech

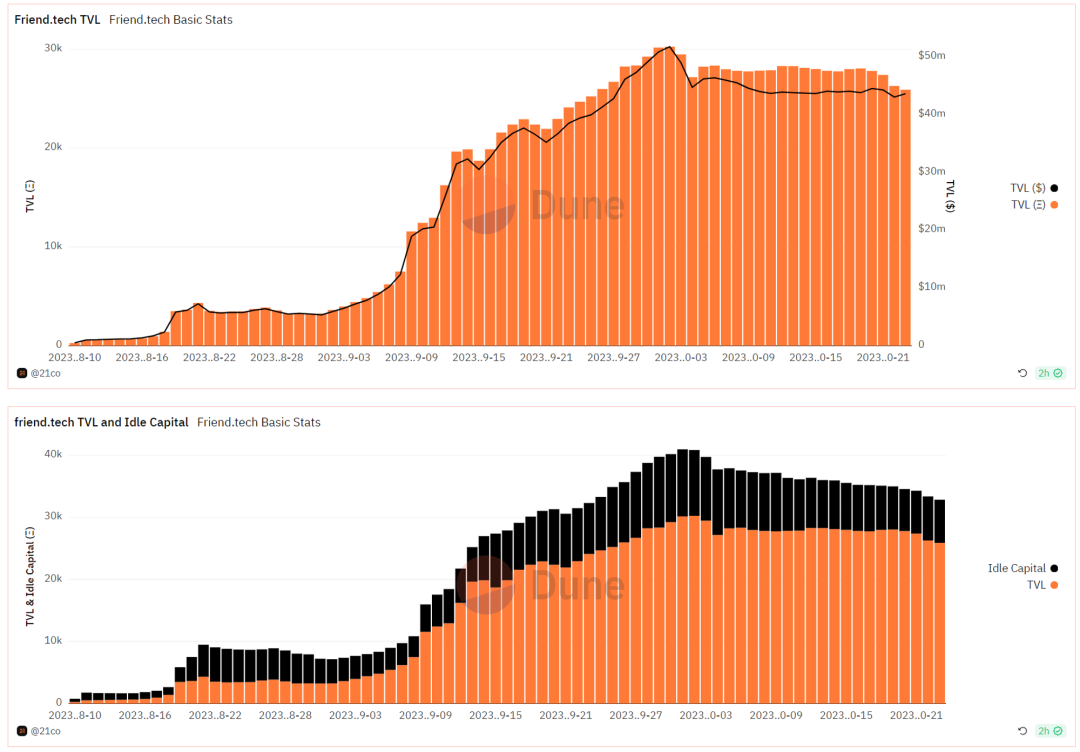

作为这波Socialfi热潮的开创者,给加密市场带来新叙事的同时稳坐龙头。上线三月,累计用户超过75k,TVL逾$44M。

(Source:https://dune.com/friendtechdatateam/friendtechdata)

尽管许多key都已经因为过于陡峭的定价曲线而颇为昂贵,成交量相比前两周已经大幅下滑,有趣的是新用户增长不断,日增长甚至创了新高,还是有许多新用户涌入。

(Source:https://dune.com/whale_hunter/friend-tech-ultimate-analytics)

同时,虽然最近有关于SIM SWAP导致FT用户资金被盗的情况发生,负面新闻似乎并没有对FT产生较大的影响。

获利的资金并未迅速离场,大量的闲置资金停留在Friend.Tech内,因此TVL并未因成交量或潜在的风险而大幅下滑。

(Source:https://dune.com/21co/friendtech-analysis)

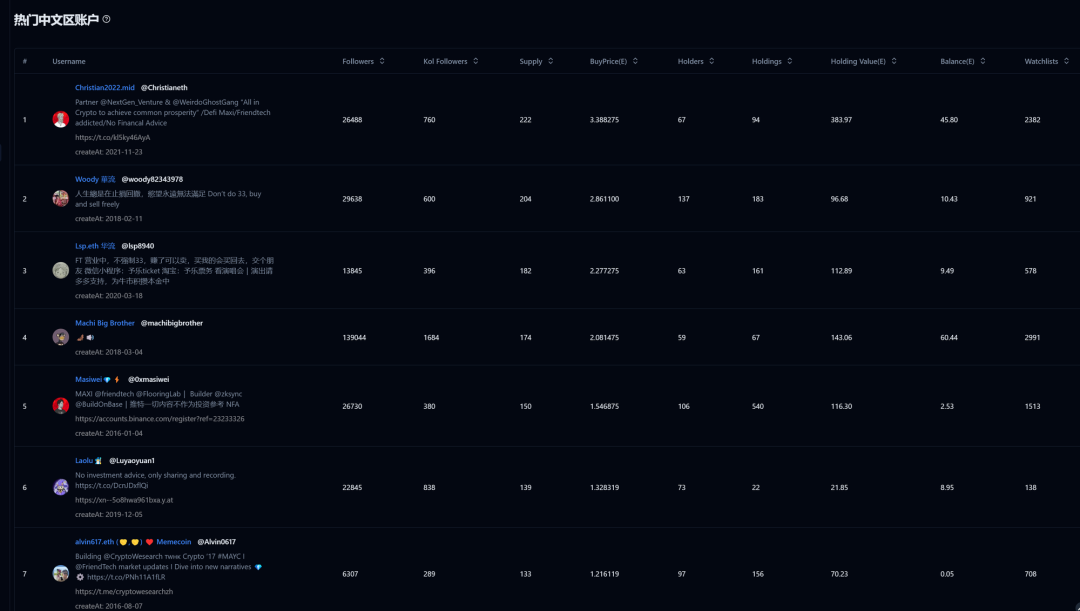

关于FT上热门的中文区账户,可以参考看板:

https://www.cryptohunt.ai/zh-CN/friendtech/topcn

02Stars Arena

Stars Arena是Avalanche上的FT类产品,与FT玩法类似,通过购买ticket进入对方的私聊房间。

一个明显的功能区别是,SA做得更像推特。可以发布内容,以信息流的形式呈现,用户的操作也更加多样。

除了房间聊天,还可以在对”推文“进行点赞、转发、评论甚至打赏,social的元素相比FT更加丰富,甚至有点像带私聊、群组功能的Farcaster。

(Source:https://www.techflowpost.com/article/detail_14130.html)

SA首发于PC端,在移动端和FT一样需要将网页添加的桌面,注册充值过程和FT差不多,用雪崩C链充值AVAX作为交易货币,整体体验比FT丝滑许多,在裂变方面使用邀请链接,有返佣机制,鼓励传播。

经济模型同样是交易抽成10%,但是分配比例与FT不同,SA将利润7%分配给房主,2%属于平台,另外1%用于返佣奖励,意味着交易量相同时,房主在SA上的收入会高于FT。

SA对于Avalanche来说有增加日活的正向引导作用,得到了Avalanche官方和创始人的大力支持,均已入驻SA。SA的TVL最高时超过$2.5M,拥有接近25k用户。

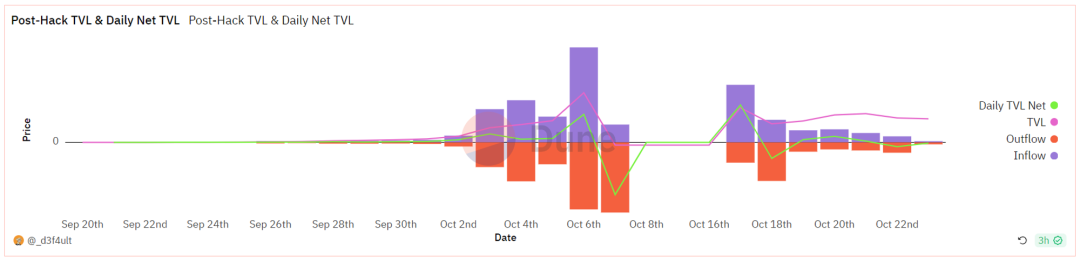

可惜好景不长,10月7日SA的合约遭到黑客重放攻击,盗取了所有用户在合约中的资产,价值约$2.9M的AVAX。

最终SA追回了90%的被盗资产,目前合约已经通过审计,产品于17日重新上线。上线后,用户需在App内进行钱包迁移才能进行交易之前拥有的资产。

(Source:https://dune.com/_d3f4ult/starsarena)

显然合约被盗对用户的信心损伤是巨大,资产恢复了$2.9M,当天就有1/3的资金流出,TVL一路下跌,目前维持在$1.2M。

03TOMO

用户对新L2上的仿盘都比较积极,错过FT的人都不想再错过仿盘,还有在新公链上增加交互撸空投,潜在的一鱼两吃的期待。

TOMO是Linea上的FT仿盘,不同于FT,它不是一个需要添加到主屏幕的网页,而是从需要从App Store下载的App。

整个注册流程和FT非常类似,需要绑定推特并充值,可以从主网充值也可以从Linea充值。

目前App内的钱包虽然支持提款,但是不能导出私钥,因为它使用的是ERC-4337标准的账户抽象钱包,这是4337在SocialFi的首次尝试。

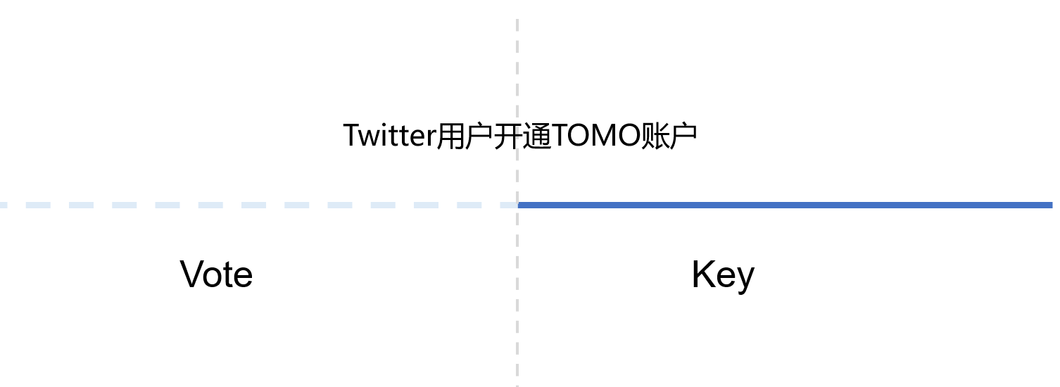

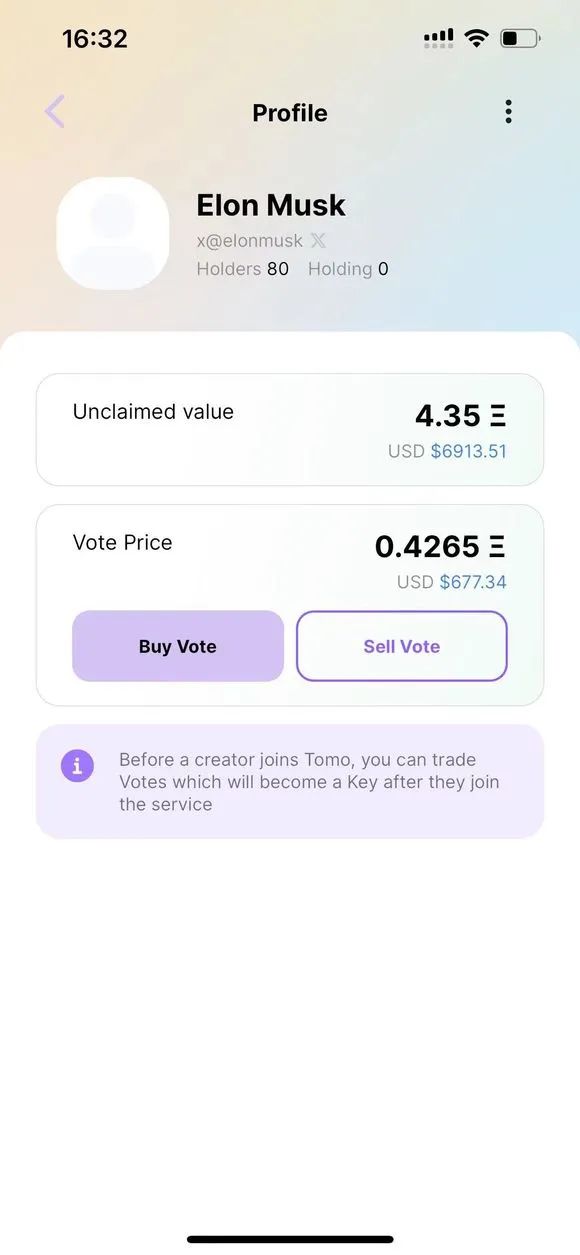

产品功能上来说也是类似的,通过购买Key进入私人聊天室。区别于FT,除了Key以外还有另一种资产,Vote,即那些尚未开通TOMO账户的推特用户。

用户可以购买他们key的“期货”,一旦他们开通TOMO账户,Vote就可以转换成Key。

经济模型上vote和key遵循相同的规则,即买卖会有5%给到平台,5%给到房主,这点和FT一致。

对于还没入驻,但是vote已经被交易产生费用的情况,交易费会累积保留在未开启的房间,成为待领取的费用,六个月内如果房主都没有入驻,该费用就会分发给vote持有者。

TOMO遵循的定价曲线是key price= x^2/43370,价格曲线相比FT更平滑,意味着相同的持key人数,TOMO的价格会是FT的37%左右,更利于小散户消费,等同于拓展了聊天室的容量。

这是一个非常有意思的微创新,在FT上有大量机器人在盯着刚开通账户的KOL,称为Sniper狙击手,企图尽早以低价购入这些KOL的key获利。

TOMO通过将未开通账户的Key期货化,来消除了机器人在这方面的优势。

在消除机器人影响方面,TOMO允许用户在应用前端一次性购买多个Key。

在FT上用户在应用中一次只能购买一个Key,而合约上并没有数量限制。有的用户会使用机器人一次购买多个Key,这样又快速又便宜(一个个买有人插在当中就会抬高购买成本),实际上会影响普通用户的体验。

通过这两个小的调整,TOMO上并无太多机器人发挥的地方,因此用户体验是相对纯净的。

类似于FriendTech,TOMO也有个积分,目前信息仅与邀请好友有关,后续很可能会与Linea的积分挂钩。

TOMO有Polychain、Ankr、Galex创始人们的深度参与,Linea官方也已入驻,品牌背书充足,同时Linea是大概率会空投的公链,适合早期参与。

目前,TOMO的TVL已经达到$1.3M,相比龙头FriendTech$44M的TVL还有40倍的差距,想象空间够足,不过TOMO上活跃的大多是华语区的KOL,英文区的KOL参与较少,用户增长速度有些停滞。

TOMO通过手续费已经赚取$414k,累计用户4.9k。

(Source:https://app.sentio.xyz/sentio/tomo/dashboards/mfqtRDSI)

04总结

本文对FT的近况,以及两款最有竞争力的仿盘产品进行了分析对比,如下图所示。

SA相比FT,社交功能拓展了许多,更高的创作者赏金以及丝滑体验都非常令人期待,可惜中道崩殂,合约被盗,给用户的信心打击非常大,即使现在恢复上线,TVL也直线下滑;

TOMO更像是一个升级版的FT,操作更流畅,以App形式呈现,同时非常注意解决FT中机器人带来的负面影响。

通过功能设计,尽可能地消除了机器人的不公平竞争,设计更成熟,也有巧思。

如果没有安全问题的话,它会是FT非常有力的竞争者,但是目前缺乏除华语区外的KOL更多参与。

相较于仿盘们的优异表现,FT在产品体验上处于下风,更新速度不够快,极可能很快成为被诟病的点,然而其开拓者的影响力,TVL资金池的深度,以及大量优质用户、KOL的早期参与投入、甚至赋能,刷积分的沉没成本等,都成为了其最深的护城河。

目前只有FT宣布了融资情况,其余项目全乘着FT给到的预期,下一波加速需要更多的融资、空投信息作为催化剂。

这波由FT带动起来的SocialFi热潮,是熊市中不多的热点,Key作为一类新型的Social trading资产,说不定是下一个ERC20,值得参与和期待。