最近两周加密市场下行,BTC 由 $30k 降至 $27k 上下。

前两周 BTC 行情,来源:CMC

在宏观方面,5 月 4 日美联储加息 25 个基点至 5%-5.25% 已经属于“强弩之末”。当天加密市场反应甚至还有所上扬。同时,此时的联邦利率已经为 2007 年以来新高,市场预期 6 月美联储将停止加息。

伪风险:银行危机

稍早一些的 5 月 1 日,摩根大通宣布收购已倒闭的第一共和国银行。为这一轮银行危机暂时划下休止符。但是目前来看,本年度的几次银行危机虽然导致市场的部分恐慌,但是今年总体而言,Nasdaq 上涨 20% 以上,BTC 涨幅更是将近 100%。

从稳定币的供给来看,同样不支持加密市场因银行危机“雪上加霜”的论点。以 USDC + USDT 来看(两者占据稳定币市场的绝大部分),稳定币在相当长的时间内都维持在 $110B 的水平上,唯一的变化只是资金从 Circle 向 Tether 的转移。

USDC 过去一年流通量,来源:CMC

USDT过去一年流通量,来源:CMC

真转变:加密行业的收缩

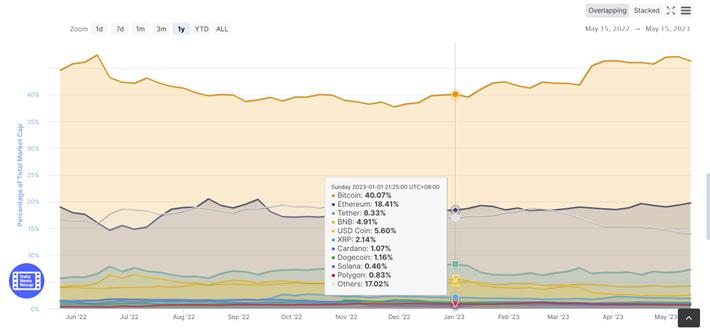

就今年来看,整个加密行业的市值向 BTC 集中确实正在发生。以 CMC 的 BTC Dominance 指数来看,今年初 BTC 市值占比整个加密市场约为 40%,目前升至47%。

再对比 BTC 的涨幅和整个加密市场今年的涨幅,结局可见:整个市场虽然正在上升,但是市场情绪却更偏向于加密行业中偏保守的避险资产 BTC。

收缩视角下的 BTC:

收缩视角其实也是一种聚光灯视角。对于 BTC 的关注也发掘出了在 BTC 网络上加载 NFT 和 Defi 的那一套愿景。但是以加密行业仅存的历史而言,BTC 代表的是整个加密行业的托底价值和最后抵押物,每一次向非支付应用层的 BTC 拓展(BTC的那些分叉)都失败了。

真正影响市场的却是 5 月 8 日,BTC 的两个矿池同时诞生两个分叉,而后在争夺最长链的过程中,失败链的交易需要重新上链,从而造成了网络拥堵。

并没有什么外部力量可以真正摧毁一个去中心化的网络,如果有,可能就是这个网络自身。

Meme币和 Altman的 WorldCoin

最近的市场中,Meme 币又很神奇地成为了趋势。虽然所有人都知道Meme 币并不能代表市场的基本面,但是 Meme 币却能从侧面反应市场情绪。

事实证明,大多数的 Meme 币都会昙花一现。但是也有例外,去年马斯克推广过的狗狗币就成为了主流。

而 OpenAI 创始人的 WorldCoin 看起来就像是新的狗狗币。支付,转账,为一个虚拟网络提供金融服务,首先提供钱包服务,并且寻求融资。

如果推行下去,WorldCoin 也很有可能成为新的主流代币。只是,马斯克没成功的事,希望Altman 能成。

总结

虽然在美联储加息和新一轮银行危机之下,加密市场前景似乎令人担忧。

但从事实来看,无论是加息还是银行危机,都无法支持市场萎缩的论点。从今年数据来看,美股和加密市场都出于上升趋势。今年的稳定币供应也并未出现萎缩。而所谓的加息和银行倒闭带来的也仅仅在于短期的回调,和资金在不同银行间的转移(从 Circle 到 Tether)。

真正改变的是加密市场对于 BTC 价值的重新凝练。在放弃了诸多“噪声”之后,加密行业再一次证明了自己的真正价值底层还是这个 BTC。就连一次 BTC 网络的拥堵都造成了远比加息至新高更大的市场影响,可见一斑。

从目前看,重视 BTC 的偏保守的市场情绪还将持续一段时间。但是市场也总不乏新的趋势,比如最近的 Meme 币,其中,最有希望的似乎是目前还处于 Meme 币阶段的 WorldCoin,希望Altman 可以带给这个行业惊喜。

毕竟加密跟 AI 一样,也是个超出当下现实的行业,希望现实可以快点赶上。