纽约时间 3月8日下午,Silvergate Bank 的母公司 Silvergate Capital Corporation宣布将根据适用的监管程序结束运营并“自愿清算 Silvergate Bank”。

“”

自愿清算(voluntarily liquidate),顾名思义,即公司自行对其资产进行清算关闭公司,是指债务人与债权人达成协议,不经过正规破产处理程序,私下对公司进行的清算。自愿清算能够避免许多破产成本,而且债权人也能获得更高比例的偿还。

“”

Silvergate Capital Corporation 在公告中表示:“鉴于最近的行业和监管发展,Silvergate 认为有序结束银行业务和自愿清算银行是最好的前进道路……银行的清盘和清算计划包括全额偿还所有存款。公司还在考虑如何最好地解决索赔并保留其资产的剩余价值,包括其专有技术和税收资产。”

“”

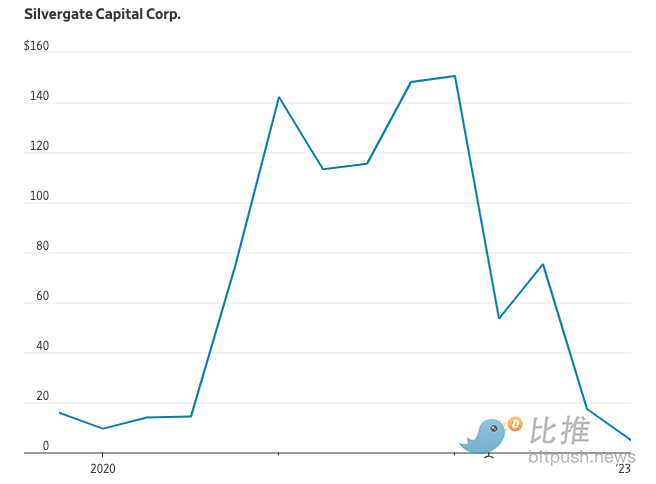

Silvergate 的股价在美股盘后交易中下跌超过 28%。根据道琼斯市场数据,周三收盘价为 4.91 美元,创下 2019 年 11 月以来的历史新低,较 2021 年 11 月创下的历史新高下跌了 98%。

摩根大通或与 Gemini 结束银行业务

“”

当天还有另一个利空消息,Coindesk援引一位知情人士的话报道称,美国银行业巨头摩根大通 (JPMorgan) 将结束与 Gemini 的银行业务关系,Gemini 是 Cameron 和 Tyler Winklevoss 拥有的加密货币交易所。据《华尔街日报》报道,早在 2020 年初,摩根大通就将 Gemini 和美国上市交易所 Coinbase 发展为客户,为他们提供现金管理服务,并为交易所的美国客户处理美元交易,它通过自动清算所网络(ACH,一种电子资金转账系统)处理电汇、存款和取款。

“”

Coinbase 交易所发言人表示,Coinbase 与摩根大通的银行业务关系保持完好。

“”

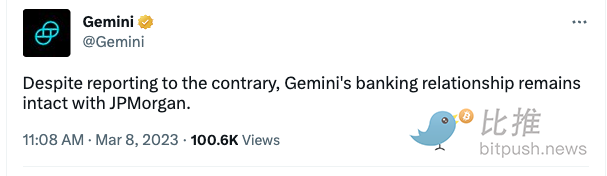

Gemini 在官推中回应了这一报道,称:“尽管有相反的报道,但 Gemini 与摩根大通的银行关系仍然完好无损。”

Gemini 于 2015 年获得纽约州金融服务部(DFS)颁发的信托执照。Coinbase 在金融犯罪执法网络 (FinCEN) 注册为货币服务企业,并且还拥有DFS颁发的加密业务许可证,即 BitLicense,两家公司都在多个州获得了汇款许可。

“”

摩根大通的决定很可能与Silvergate Bank、Gemini Earn 事件有关。

“”

比推此前报道,Gemini 已受到美国证券交易委员会 (SEC) 的审查,被控通过其“Earn计划”提供未注册的证券。Gemini Earn 计划一直存在争议,在该计划的重要合作伙伴和数字货币集团 (DCG) 的子公司 Genesis 停止运营后,用户无法从该平台提取资金。加密收益也是其他拥有相似业务的公司今年以来面临的最新监管挑战。

“”

Gemini 失去一个主要银行合作伙伴可能对其影响不大,根据该交易所的网站,该公司与其他银行有合作关系,例如 State Street,以及即将清算的 Silvergate Bank。

“”

出入金的负面影响

“”

Silvergate Bank 的陨落正在加剧美国监管机构之间关于银行是否能够防范加密风险的争论,并且令加密公司在美国的出入金业务面临阻碍。

“”

Silvergate 总部位于加利福尼亚州La Jolla,自 2013 年以来一直为加密货币公司提供银行服务,并推出了自己的内部支付服务 Silvergate Exchange Network (SEN)。SEN平台是Signature的旗舰产品,为客户提供全天候相互转移现金的能力,被视为加密客户服务的“心脏”,Silvergate 周五晚些时候宣布暂停 SEN。

“”

该公司在 2018 年 11 月申请上市时透露,它拥有近 500 个加密客户。其首次公开募股 (IPO) 于 2019 年完成,在纽约证券交易所交易,当时拥有超过 750 个加密客户。

“”

Silvergate 危机也让那些一直以来反对银行系统与加密公司交互的立法者更拿捏了证据。

“”

另一家远离加密货币的银行是 Signature Bank。2022 年 12 月,它宣布计划减少加密服务、向客户返还资金并关闭与加密相关的账户。由于与熊市和 FTX 破产相关的流动性问题,该银行还在 2022 年最后一个季度从美国联邦住房贷款银行系统 (FHLB)借款近 100 亿美元。

“”

加密银行业务转移至其他国家

“”

银行的举动也在影响加密公司。2 月,币安宣布暂停美元的银行转账。几周前,该交易所表示其 SWIFT 转账合作伙伴 Signature Bank将只处理超过 100,000 元银行账户的用户交易。

“”

Digital Asset Capital Management 联合创始人Richard Galvin 对彭博社表示,公司正在与位于瑞士的银行交谈,他没有透露银行名称。Galvin说:“有些银行处理加密交易,但他们并不专注于加密,这与 Silvergate 不同。我们已经在积极采取措施减少我们在 Silvergate 的存款并寻找新的银行客户,找到银行合作伙伴可能需要一些时间”。

“”

在瑞士,Sygnum Bank AG和SEBA Bank AG是与数字资产部门合作的银行之一,巴哈马的Deltec Bank & Trust Ltd.和Capital Union Bank也以专注于加密货币而闻名。

“”

Signature 的倒闭引起了美国关键立法者的注意,美国参议院银行、住房和城市事务委员会主席、资深参议员 Sherrod Brown在一份声明中表示:“今天,我们看到当一家银行过度依赖加密货币等高风险、不稳定的行业时会发生什么。当银行涉足加密货币时,它会将风险分散到整个金融系统,而付出代价的将是纳税人和消费者。”

“”

总之,美国银行系统与加密行业之间的未来关系存在不确定性,尽管美国以外的OTC可能会因此受益,但长期来看对整个行业来说影响仍是负面的。