Is the market underestimating the potential impact of the upcoming Morgan Stanley spot Bitcoin ETF? Well, Strategy CEO Phong Le thinks so.

According to him, the wealth management segment of the investment bank could easily flip BlackRock’s IBIT.

He added,

Morgan Stanley Wealth Management oversees about $8 trillion in AUM and recommends 0–4% bitcoin allocation. A 2% allocation would represent $160 billion, ~3X the size of IBIT. $MSBT: Monster Bitcoin.

For perspective, BlacRock’s iShares Bitcoin ETF (IBIT) currently leads the segment with a cumulative net inflow of $63 billion and assets under management (AUM) of $55 billion. Hence, the $160 billion projection would be three times bigger than IBIT’s current AUM.

‘Still early?’ – Why Morgan Stanley is betting on BTC

Since the first wave of U.S. spot BTC ETFs debuted in early 2024, Morgan Stanley has mainly been a distributor, allowing advisors to recommend third-party offerings such as BlackRock’s IBIT. For this, it captures commissions for the access.

As of Q3 2025, BlackRock’s IBIT was printing nearly $191 million in management fees and was the third-highest revenue-generating product in its ETF line-up.

A few months later, Morgan Stanley applied to directly offer its BTC ETF product (MSBT). It refiled the application and could soon begin trading. This would eventually help it capture both the distribution and management fees.

As the U.S. spot BTC ETFs enter their third year, and IBIT’s dominance continues, one would wonder why Morgan Stanley is suddenly making its bold bet in the space now.

According to Amy Odelnburg, the firm’s head of crypto, the adoption was ‘still early,’ adding that current demand is mostly from self-directed investors rather than wealth-advisor-managed accounts.

Even the distribution of these ETFs, about 80% of what we see on our platform, is coming through the self-directed business.

The firm is eyeing BTC lending, trading, and even custody, and would be the first U.S. bank to directly offer a BTC ETF.

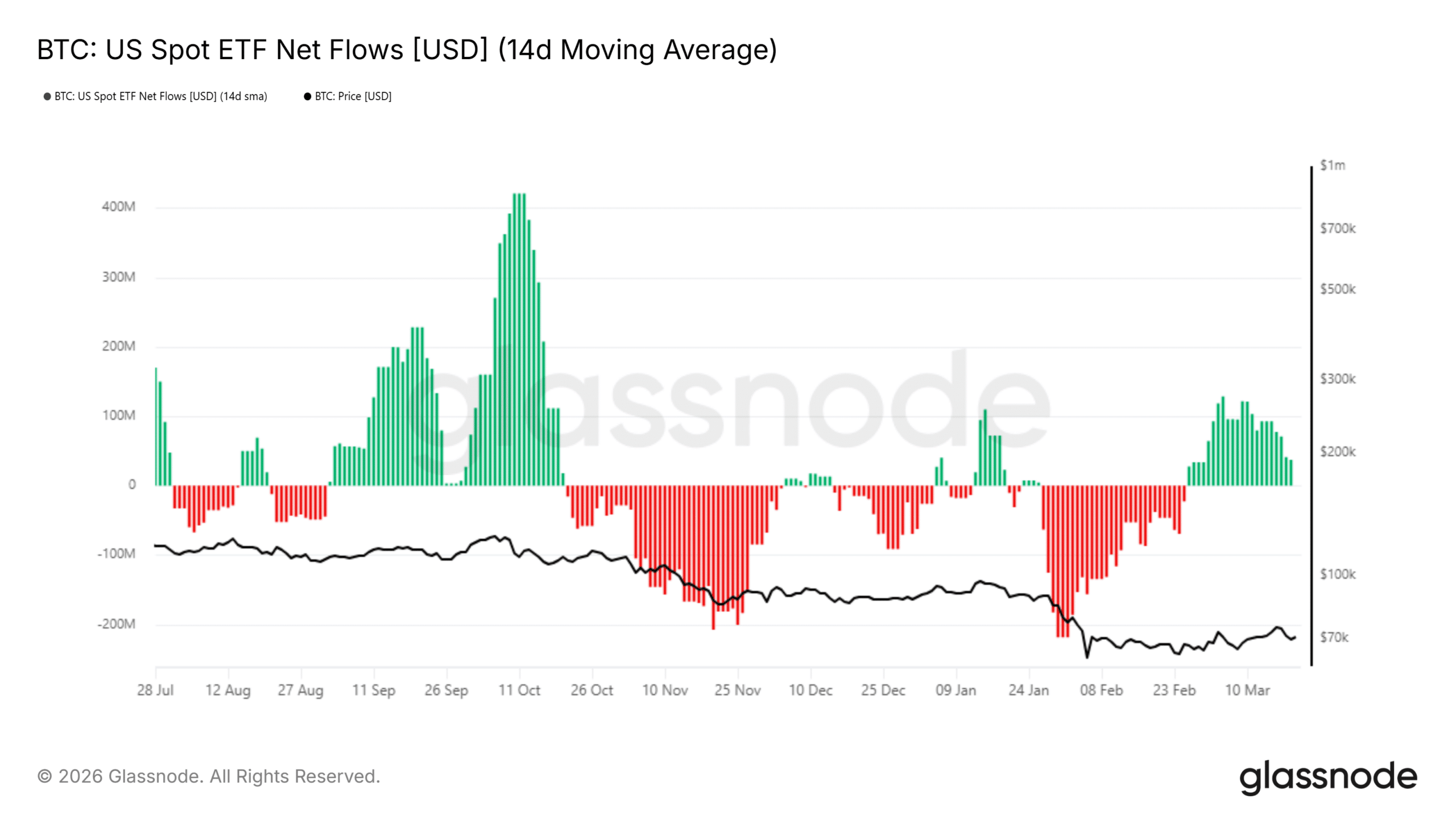

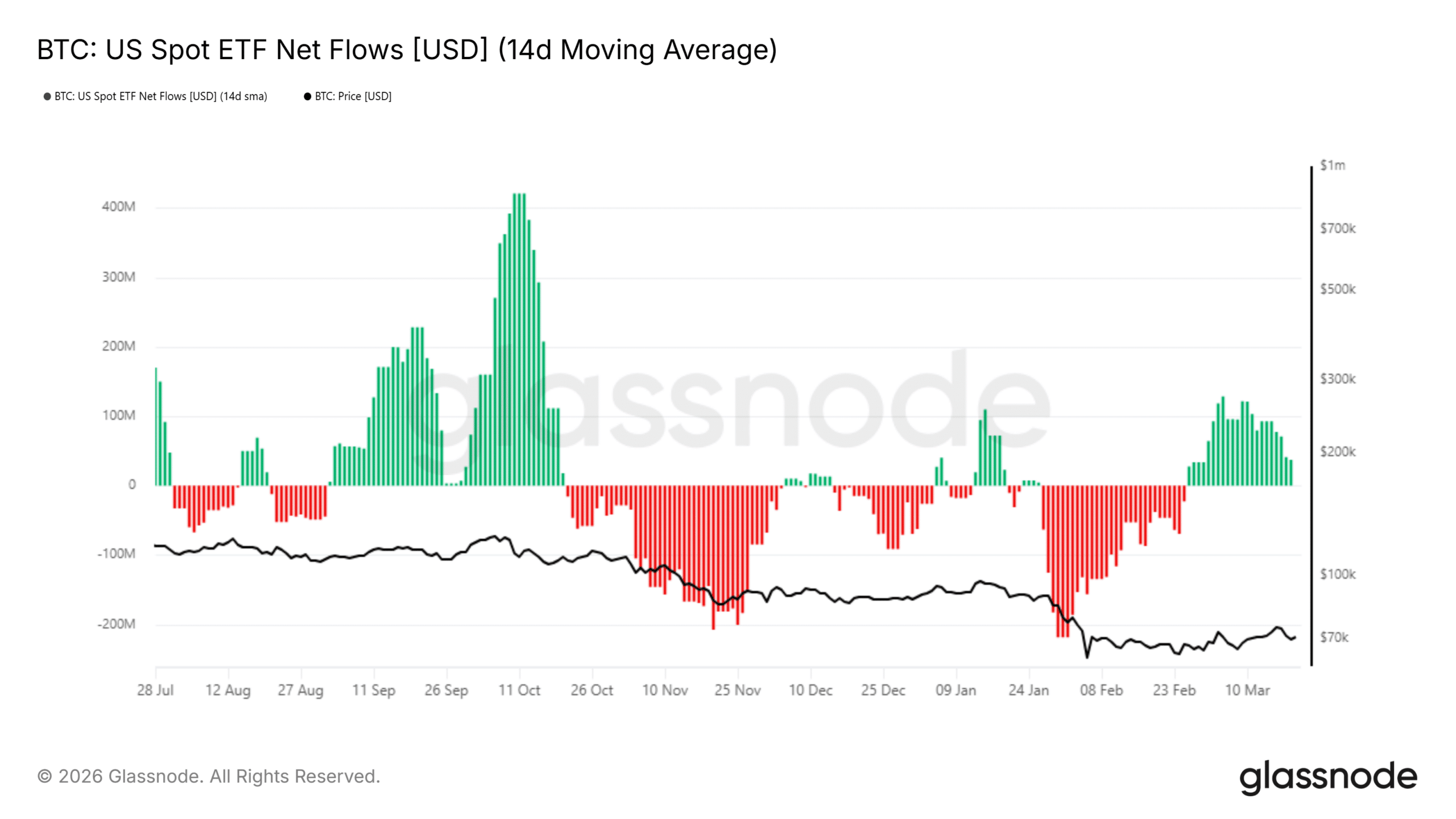

That said, Joe Takayama of Backpack cautioned that the $160 billion projected demand could still be unrealistic, as allocation could be below 2% or even close to zero. Meanwhile, the strong recovery in BTC ETFs seen in early March has reversed, with consecutive daily outflows over the past three days of trading.

Amid the ongoing macro uncertainty, a sustained risk-off mode by ETF investors could derail BTC’s recovery. At the time of writing, the asset traded at $70K.

Final Summary

- Strategy CEO Phong Le projected that the Morgan Stanley BTC ETF could easily trigger $160 billion in demand.

- Morgan Stanley said that institutional crypto adoption is still early, with current demand primarily driven by self-directed investors and not advisor-managed accounts.