Editor's Note: For a long time, DeFi options have not become a mainstream trading category. Compared to perpetual contracts, they are more complex, have more fragmented liquidity, and find it harder to establish stable, organic demand.

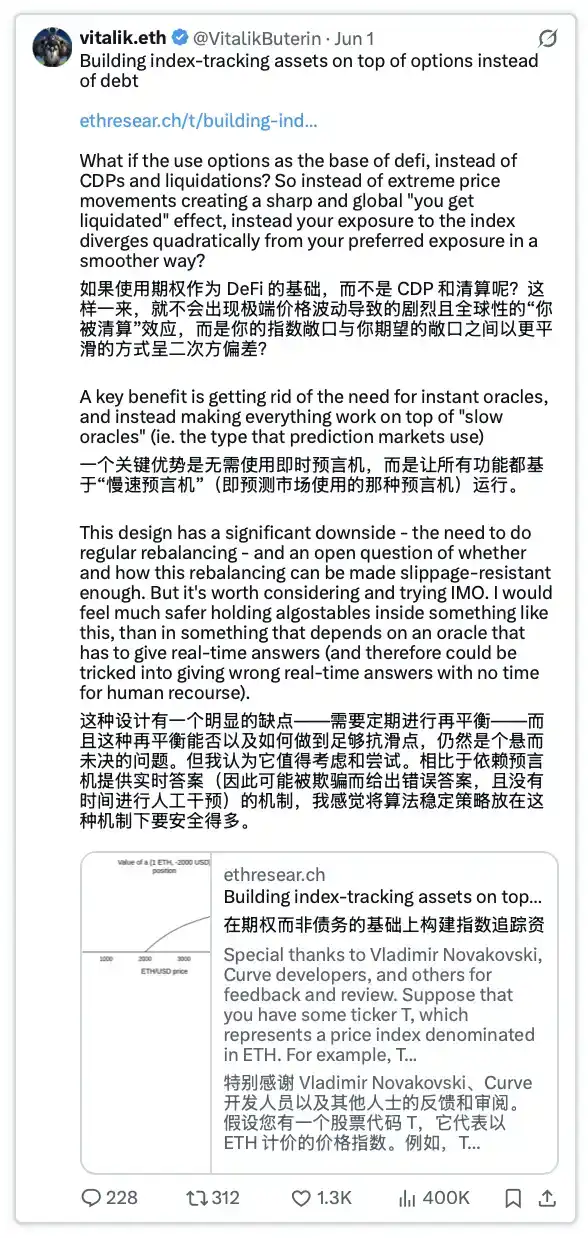

However, Vitalik's recent proposal for an algorithmic stablecoin opens up another possibility for options: they are no longer treated as an independent trading product, but rather become the foundational financial building blocks behind stablecoins, yield products, and structured assets.

The author of this article interprets this proposal from the perspective of options. He believes that the stable-side asset in Vitalik's design is essentially similar to a synthetic covered call: the user splits 1 ETH into two parts, one part obtains 'stable value' below a certain strike price, and the other part obtains the upside gains above the strike price. Since these two parts always add up to 1 ETH, the system does not need to introduce debt, margin, or liquidation mechanisms, thereby avoiding the core liquidation risk of traditional CDP stablecoins.

Yet, the difficulties of this design are equally apparent. For the stable-side asset to approximate a stablecoin, it requires continuously rolling deep in-the-money call options, which brings issues like rollover slippage, front-running of fixed trading paths, and insufficient liquidity. More importantly, behind every unit of stable asset, someone must continuously hold the corresponding upside-side asset, which is essentially a leveraged long ETH position without funding rates or liquidation risk. Whether this demand can exist long-term determines whether the system can truly expand.

Finally, drawing from Rysk's experience, the author points out that the reason DeFi options have struggled to scale in the past is because they are too complex as a direct trading product, and user demand is not sufficiently organic. But if you change its position, placing options at the underlying layer of more complex assets like stablecoins, structured yields, and index products, they might actually be more suitable as DeFi infrastructure. In other words, the opportunity for options in DeFi may not be to become the next perpetual contract, but to become the pricing and risk distribution engine behind the next generation of on-chain financial products.

The original article follows:

For years, I've heard the same line: "Options don't work in DeFi."

After working on Rysk, I admit there's some truth to that. Most DeFi options products have struggled to gain traction. Liquidity is fragmented, attracting organic trading flow is difficult, and traders consistently opt for simpler products. Perpetuals became the default tool for expressing directional views, while prediction markets offer a simpler way to trade event outcomes.

That's precisely why Vitalik's recent proposal caught my attention. He suggests using an option-like equity structure to build an algorithmic stablecoin without a liquidation mechanism.

What really drew me in was the angle: options not as a product to trade, but as infrastructure underlying a product.

This is the view I've been pushing for years, and the core idea behind building Rysk V12. For us, the product is yield; for Vitalik, the product is stability. The more I thought about it, the more familiar the design felt.

The stable side he describes is essentially a covered call.

Why It's a Covered Call

His design splits one unit of ETH into two types of equity. One side is P, which holds the value up to a certain strike price; the other side is N, which receives the appreciation above that strike. Together they always sum to one unit of ETH, so there's no debt, no margin, and nothing to liquidate.

Assume ETH price is $2,500, with a strike price of $1,500. As long as ETH stays above $1,500, P behaves like equity stable at $1,500; only if ETH falls below $1,500 does P start taking downside risk. N gets all the upside above $1,500.

This is exactly the payoff structure of a covered call.

The holder keeps the asset, sells the upside above a certain strike, and collects a premium. P replicates precisely this covered call payoff. N is equivalent to the call option held by the buyer.

More accurately, it's a synthetic covered call. No one externally sells an actual option; instead, the equity is split to reconstruct the same payoff.

This is the same thesis behind Rysk V12. Users hold ETH, BTC, or HYPE and earn upfront yield by selling covered calls. Vitalik points the same building block towards stability.

Same engine, different product.

The Problem: It's Deep In-The-Money and Must Be Continuously Rolled

Right now, most Rysk users sell out-of-the-money covered calls. They hold ETH and choose a strike above the current price: either betting price won't reach it, or being willing to sell and take profit at that higher price if it does, while keeping the premium regardless.

But the stable side in Vitalik's design needs a different structure. To behave like a stable amount, the strike must be far below spot, so the call would be deep in-the-money, with most of its value being intrinsic.

At a spot price of $2,500 and a $1,500 strike, there's $1,000 of intrinsic value the buyer must pay upfront. That makes the trade far more capital intensive.

But a call can only stay stable for a moment. Once ETH drifts towards the strike, it starts taking ETH downside, so it must be rolled down to a lower strike, again and again.

So, this stable asset is essentially a program of continuously rolling covered calls.

Vitalik points out this risk himself. The slippage from repeated rollovers is the biggest threat to the design, and how the roll is executed is the truly hard part.

Any mechanism that trades on a fixed, public schedule is easily front-run. This is precisely the problem DeFi Options Vaults (DOVs) faced: they sold the same duration, same strike options every week at the same time, so the market knew exactly what was coming and positioned ahead, extracting value from that flow.

Regardless, every roll needs a buyer. The question is: who buys it? And at what price?

The Hardest Part Is Funding It

In Vitalik's model, someone must deposit a full unit of ETH, split it, sell the stable side, and hold the upside side. This depositor is the person the whole system relies on.

The most obvious candidates are market makers.

But the position they end up holding is essentially leveraged long ETH. And anyone wanting leveraged long ETH can just buy a call option or go long a perpetual. That's simpler, more efficient, and more familiar. The depositor is taking a harder path to get a position they could get more easily elsewhere.

The upside side does have one real advantage: it offers real leverage without funding rates or liquidation risk, which a perpetual cannot.

But it still needs to find buyers, and not just once. For every unit of stable asset that exists, someone must hold the corresponding upside side.

To scale, this model needs a persistent set of people who, in any market environment, are willing to hold ETH leveraged longs in this specific form continuously.

And market makers are resource optimizers by nature. Without a clear reason, they won't adopt something new, capital intensive, and with heavy integration costs. "Speculators and market makers will provide liquidity" is the assumption the whole design rests on. But that behavior doesn't happen in a vacuum.

What We Learned at Rysk

We learned this the hard way at Rysk. Earlier versions of the protocol struggled to expand, lacked organic demand, and never found product-market fit.

In the current protocol, Rysk V12, both sides of the trade have strong reasons to participate. So, Rysk starts with two parties who already want in. Holders want yield from assets they already hold, and their assets are the collateral.

Market makers compete to buy this flow via an RFQ (Request-for-Quote) mechanism. They only pay the premium, don't need to post collateral, end up with the option exposure they actually want, and can price and hedge it on their own books. This is the more capital-efficient side of the trade, which is why trading desks integrate spontaneously.

No one is asked to hold a position they could get more easily elsewhere.

The system also doesn't rely on incentives or token emissions.

Worth Building

I'm glad to see this design being seriously explored. The challenges are real, but they're the interesting kind. This is exactly the design space DeFi should explore.

What feels validating is that this proposal reinforces the same choices we made at Rysk: fully collateralized, no liquidation, no counterparty risk, and physical settlement requiring an oracle only at expiry.

Different use case, same foundation. That foundation is live and proven on HyperEVM, with market makers competing for flow. We've also deployed to Ethereum mainnet and will open to the public soon.

If you're exploring stablecoins, structured products, index products, or anything with optionality under the hood, feel free to reach out.

Options are building blocks. The truly interesting stuff is what gets built on top.