By | 字母AI

Seven months after announcing his return to an executive role and founding the AI startup Prometheus, Jeff Bezos rarely discusses how he feels about sitting back in the CEO chair.

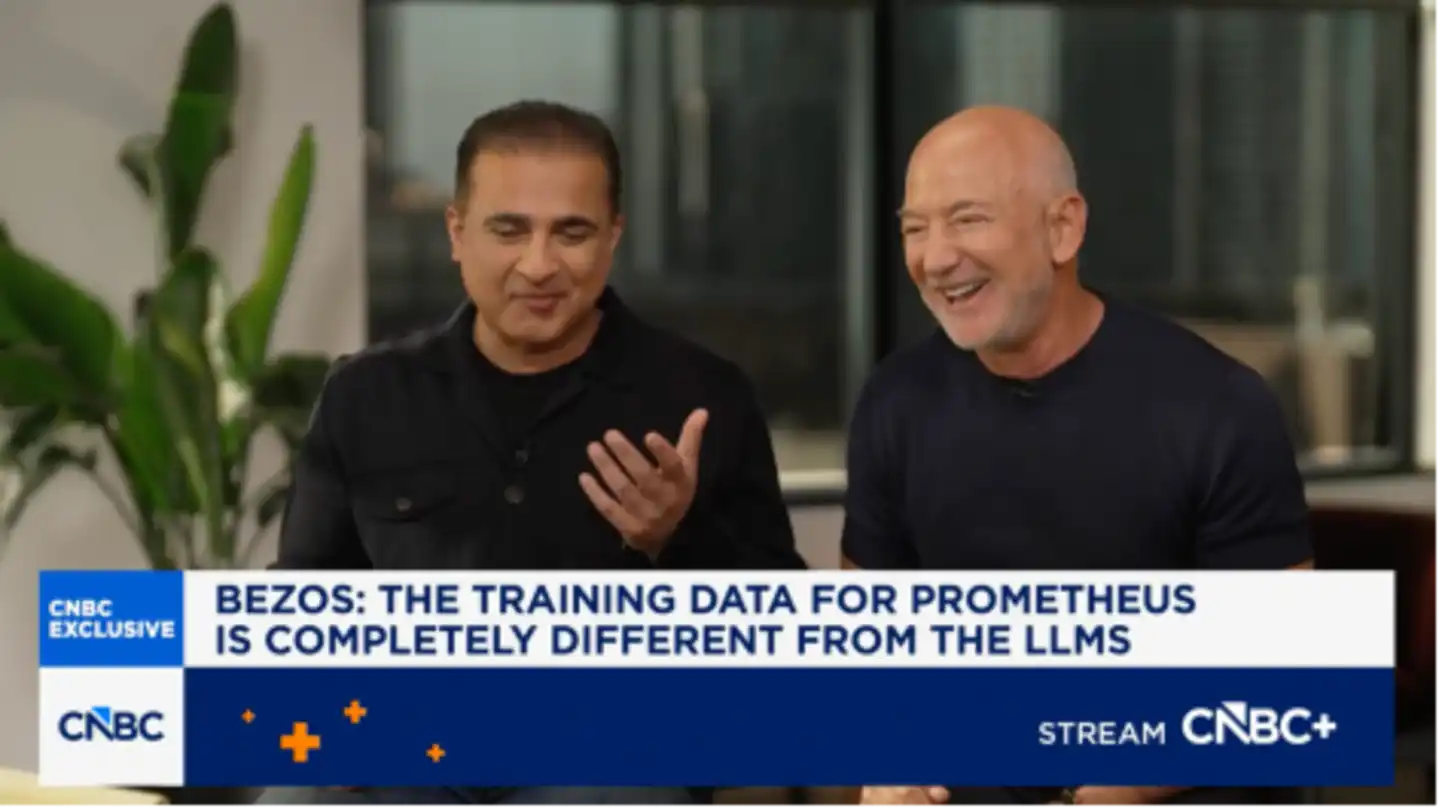

In a recent CNBC interview, Bezos admitted that he hadn't planned to be CEO again.

After stepping down as Amazon's CEO in 2021, Bezos handed daily management to Andy Jassy, taking on more of a role as founder, chairman, and investor.

He remained behind Amazon, Blue Origin, and The Washington Post, just no longer personally managing the day-to-day operations of a company as its CEO.

But for Prometheus, he returned to the front lines, resuming the life of a startup. Bezos described this state as "Type 2 fun"—the process is exhausting, but looking back, it feels worth it.

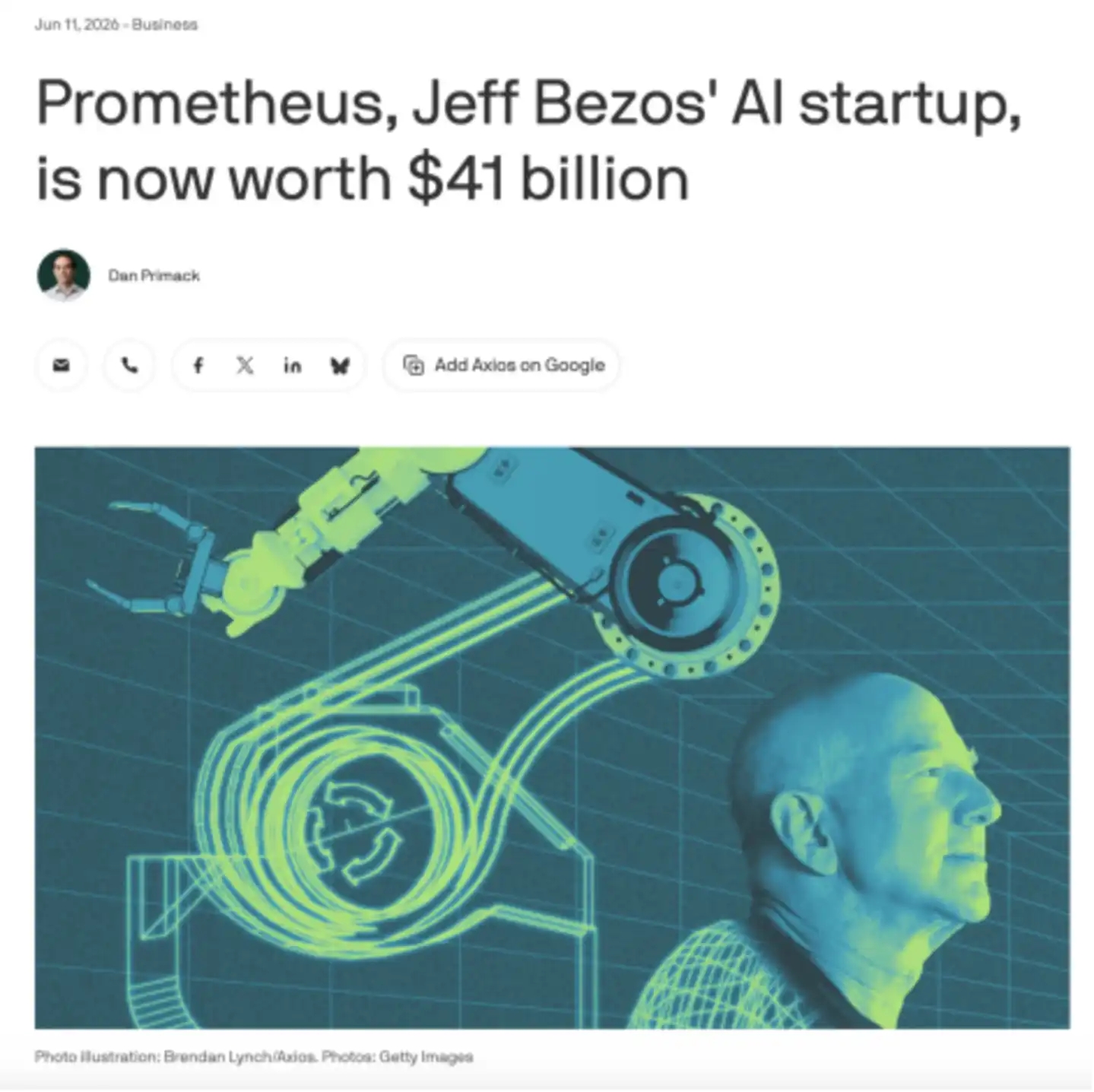

Prometheus has been in existence for less than a year with only about 150 employees, but its valuation has already reached a staggering $41 billion.

This is Bezos's first hands-on venture into a completely new future since leaving Amazon.

Although, this future still revolves around his old rival, Musk.

Prometheus

In Greek mythology, Prometheus is the Titan who brought fire to humanity. He is not only associated with "fire" but is often interpreted as a symbol of craftsmanship, creation, civilization, and foresight.

On June 11, Axios reported that Prometheus had completed a $12 billion Series B funding round, valuing the company at $41 billion. The investor lineup almost encompasses Wall Street and top global venture capital firms, including JPMorgan Chase, BlackRock, Goldman Sachs, internet investment giant DST Global, and life sciences and hard tech investment firm Arch Venture Partners. Bezos himself also participated in the investment.

Last November, the company raised $6.2 billion in Series A funding upon its launch; just seven months later, it completed a $12 billion Series B, with the single-round funding amount almost doubling, and cumulative funding exceeding $18 billion across the two rounds.

In other words, it stepped onto the valuation peak of physical world AI as soon as it went public.

Humanoid robot company Figure AI announced over $1 billion in Series C funding in September 2025, with a post-money valuation of $39 billion;

Robot "brain" company Skild AI announced $1.4 billion in Series C funding this January, with a valuation exceeding $14 billion;

Another robot general intelligence company, Physical Intelligence, has a confirmed valuation of $5.6 billion, with reports suggesting its new funding round valuation may exceed $11 billion.

But Prometheus, in less than a year, has surpassed the valuations of these embodied AI star companies.

According to Bezos, Prometheus is not building robots but a kind of Artificial General Engineer AI.

Simply put, Prometheus aims to have AI participate in the design, simulation, testing, and manufacturing of complex real-world products.

Jet engines, spacecraft, chips, cars, medical devices, pharmaceuticals, consumer electronics, robots... The R&D cycles for these products often take years. A design goes through repeated simulation, prototyping, testing, failure, modification, and starting over.

What Prometheus wants to compress is this process—it aims to accelerate not a single task, but the entire "invention cycle": from design to simulation, from testing to manufacturing, and back to the next round of design.

More importantly, industrial AI remains a largely unexplored ocean, a blue ocean full of potential.

This direction is not without players. Robot companies are working on embodied intelligence, engineering software companies on simulation and design optimization, NVIDIA is pushing its physical AI platform, and manufacturing giants are also integrating AI into their production processes.

But it hasn't yet produced a truly benchmark product.

This relates to the complexity of industrial AI itself. It deals not with text and code on a screen, but with real-world materials, structures, temperature, energy consumption, cost, supply chains, and safety margins.

Here, AI can't just give an answer that looks plausible.

It must withstand simulation, pass testing, and ultimately be manufactured in reality.

Prometheus's $41 billion valuation is not buying a proven, mature company. It's buying an as-yet-unverified but potentially enormous possibility.

Prometheus stole fire, giving humanity the tools to change the world.

Bezos's Prometheus wants to hand the fire of AI to engineers in the real world.

Bezos's Third Hands-On Venture

If we exclude asset-type investments like acquiring The Washington Post, Prometheus counts as Bezos's third truly hands-on venture.

The first was Amazon.

In 1994, he left Wall Street and founded Amazon in Seattle. It started as just an online bookstore. Later, the company grew into one of the world's largest e-commerce platforms. In 2024, Amazon's annual revenue exceeded $630 billion; its AWS also became one of the most important players in the global cloud computing market.

Bezos built a set of infrastructure supporting modern commerce: warehousing, logistics, cloud computing, advertising, membership systems, and the operational machinery built around these systems.

The second was Blue Origin.

In 2000, Bezos founded Blue Origin. If Amazon belonged to the digital world, then Blue Origin faces the physical world. There is no "fail fast" here, only repeated design, manufacturing, testing, and launching.

Blue Origin isn't a paper-based space dream either. New Shepard has completed multiple suborbital flights and sent tourists to space; the BE-4 engine became the main engine for ULA's new Vulcan rocket; New Glenn is Blue Origin's core product for entering the heavy-lift orbital launch market.

Rockets aren't pure software products. They must ignite, undergo test fires, launch, and be tested for physical stability and manufacturing precision in the real world.

Amazon gave Bezos the experience of "turning complex systems into platforms," Blue Origin gave him the experience of "doing complex engineering in the physical world." With Prometheus, these two lines of experience converge.

Bezos mentioned in the CNBC interview that he was initially just a founding investor. Later, seeing the project's progress, he realized "I couldn't sit on the sidelines" and took on the co-CEO role himself.

Because Prometheus isn't a business suitable for remote betting. It's not building a lightweight application, but a complex system for the real industrial world. It requires both AI capabilities and engineering understanding; it needs to understand both models and manufacturing; it needs software speed but also respect for the constraints of the physical world.

And this falls precisely at the intersection of Bezos's experience over the past three decades.

Prometheus has Amazon-style platform ambitions and Blue Origin-style engineering difficulty. Bezos's return to the CEO role isn't just because he saw a new AI trend; it's more like he saw a familiar problem finally having a new solution.

Moreover, this time Bezos isn't diving in alone.

Prometheus's other co-CEO, Vik Bajaj, was an early core figure in Google's life sciences business, co-founding Google Life Sciences, later Verily; he later served as Chief Scientific Officer at cancer early detection company Grail.

In other words, Bajaj's past work has always been at the intersection of science, engineering, data, and real industry.

This co-CEO duo is interesting: Bezos brings Amazon-style platform capabilities and Blue Origin-style engineering experience; Bajaj brings experience in life sciences, hard tech, and complex R&D systems.

Two people, one better at turning complex systems into large-scale platforms, the other more familiar with pushing scientific problems into real industry.

Bezos said in the CNBC interview that Prometheus now occupies most of his time, followed by Blue Origin, and then AI-related work within Amazon.

In a sense, this is somewhat abnormal—over the past year, many well-known CEOs have chosen to step back, citing precisely that the AI era has arrived and the company needs someone more suited to lead the transformation.

But Bezos went in the opposite direction, and not to manage a mature giant like Amazon, but to invest most of his time in an AI startup less than a year old.

For a 61-year-old billionaire to return to the office, there must be a special reason. Perhaps he has already seen that the next opportunity to change the world is right there.

From "Blue Sky" to "Blue Ocean"

Blue Origin still exists. But it must be admitted that the "blue sky" of commercial space has been captured by SpaceX.

Last week, SpaceX completed its IPO, initially raising $75 billion. Subsequently, underwriters exercised the over-allotment option, increasing total fundraising to $85.7 billion, making it the largest IPO in global history. On its first trading day, SpaceX's stock rose about 19%, with its market cap breaking $2 trillion, pushing Musk to the position of "the world's first trillionaire."

SpaceX captured not just the launch market, but also the sexiest story in commercial space: reusable rockets, satellite internet, the Mars vision, massive valuation, employee wealth creation, and an IPO record-breaking enough to rewrite capital markets.

In contrast, while Blue Origin has New Shepard, BE-4, and New Glenn, these achievements aren't enough to change the seating at the table. The definition of commercial space has already fallen to SpaceX.

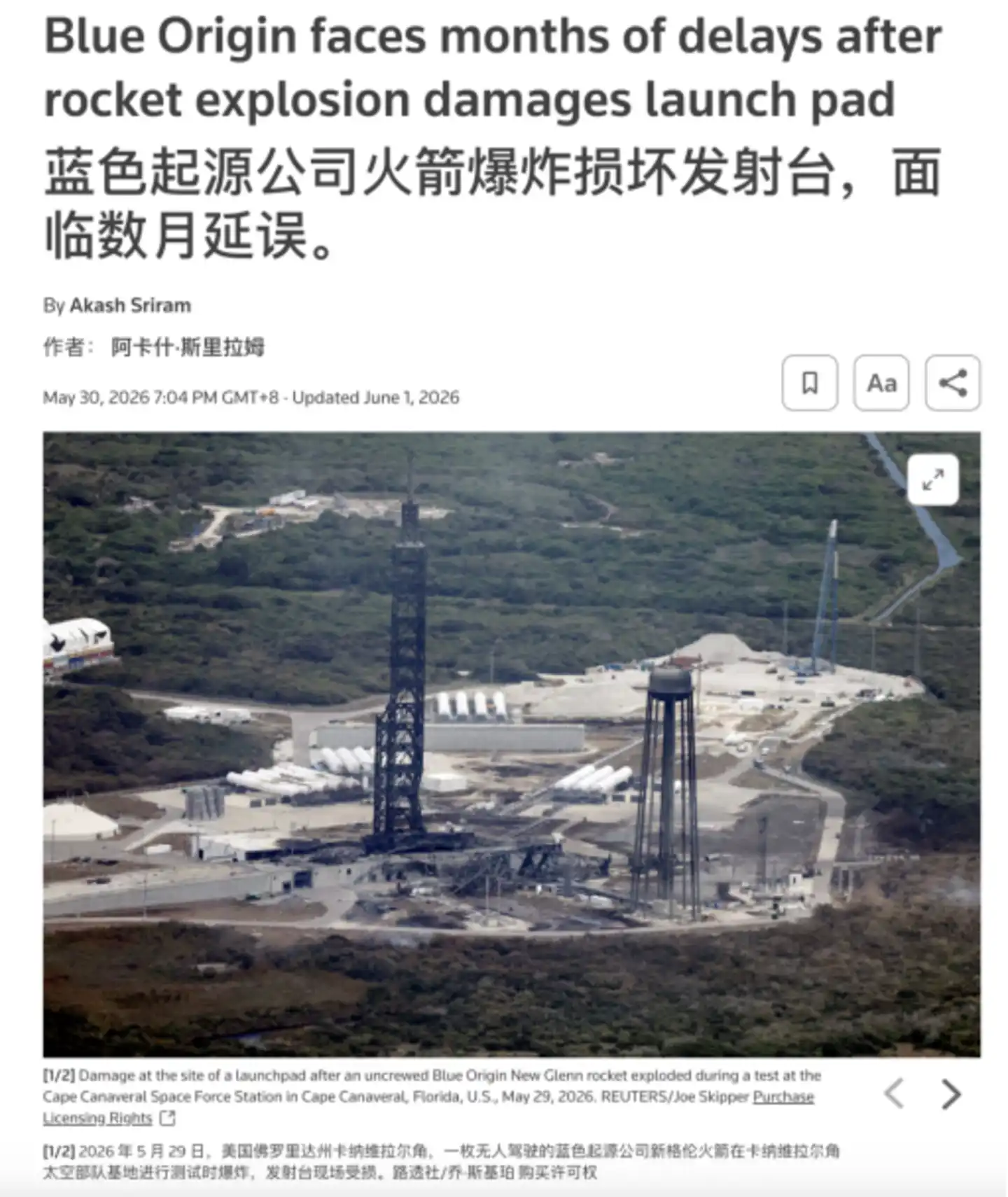

Moreover, Blue Origin was recently sharply reminded by the physical world.

On May 28, the New Glenn rocket exploded during a static fire engine test at Cape Canaveral, Florida, damaging the launch pad and potentially delaying subsequent launch plans by months.

Space is harsh. Even if a company has money, patience, vision, and a founder like Bezos, rockets won't fly on schedule just because of that.

Reuters' latest report on June 16 shows SpaceX's stock continued to rise, closing at $201.80, with a market cap reaching approximately $2.655 trillion, already surpassing Amazon and briefly exceeding Microsoft. In other words, Musk not only won the definition in commercial space but also let SpaceX step on Amazon, the company Bezos built, in the capital markets.

This gives Bezos a somewhat "being overshadowed everywhere, might as well forge a new path" vibe.

Unfortunately, Musk seems to be "capable of everything from heaven to earth," making it hard to avoid him even after switching battlefields, as if the old rivals are just opening a new game.

Tesla works on autonomous driving, the humanoid robot Optimus; SpaceX works on highly engineered rocket manufacturing; xAI tries to integrate model capabilities into Musk's own company ecosystem... It can be said that Musk's AI path was never just about staying on the screen from the start. He wants AI to enter cars, robots, factories, and rockets, ultimately taking over more physical labor in the real world.

But there is a difference. If Musk is betting on "how AI executes tasks in the real world," then Bezos is betting on "how AI participates in real-world invention."

The industrial AI track is not short of players. OpenAI is supplementing robotic capabilities, Anthropic is entering industrial scenes, NVIDIA is building the Physical AI foundation—it's truly a time of fierce competition. But who will become the gateway to the industrial AI era remains unknown.

Prometheus wants to seize this position. It's not treating industrial AI as just a business direction, but as the entire company's proposition. What it wants to compete for is the human engineering of the AI era.

This time, Bezos doesn't want to chase behind Musk again.