Author: danny

When we talk about public blockchains in a bear market, what are we discussing? Price? Community? Or governance? The more fundamental question is: operating a public blockchain is essentially governing a digital country. Tokens are currency, developers are citizens, DApps are industries, and on-chain governance is the government. If we reexamine Solana's development history from the perspective of governance, many seemingly accidental decisions have clear logic behind them.

Introduction: No One Is Born Strong

On August 9, 1965, Lee Kuan Yew shed tears in front of television cameras. Singapore was "kicked out" of the Malaysian Federation, becoming a tiny island nation with no hinterland, no resources, and no military. No one believed it could survive.

On November 11, 2022, FTX filed for bankruptcy. Solana's TVL evaporated by over 75% in a week, and the price of SOL plummeted from $32 to $8. The entire crypto circle's OS: "Solana is finished."

The beginnings of these two stories are strikingly similar: a small entity abandoned, struggling to survive in a hostile environment. And the paths they later took—from dependence, to survival, to transformation and upgrading—can almost be compared frame by frame.

This article does not aim to discuss price or community, but a more fundamental question: operating a public blockchain is essentially governing a digital country. Tokens are currency, developers are citizens, DApps are industries, and on-chain governance is the government. If we reexamine Solana's development history from the perspective of governance, many seemingly accidental decisions have clear logic behind them.

Chapter 1: The British Military Era—SBF and FTX's Umbrella

Singapore's British Military Economy

In the early days of independence, one of Singapore's economic lifelines was the consumption and employment brought by the British garrison. The British military bases contributed about 20% of the GDP at the time. Singapore was not unaware of the fragility of this dependence, but for a newborn country, there was no qualification to pick and choose clients. Survival was the top priority.

In 1968, Britain announced that it would withdraw all its forces east of the Suez Canal by 1971. This was tantamount to pulling the rug out from under Singapore. But it was this "abandonment" that forced Singapore to seriously consider: if the protective umbrella is gone, what do I rely on to survive?

Solana's SBF Era (2020-2022)

The Solana mainnet launched in March 2020, but what truly made it stand out among the many "Ethereum killers" was Sam Bankman-Fried and his empire. FTX and Alameda Research were not only the largest sources of capital injection into the Solana ecosystem but also its credit endorsers. Early core ecosystem projects like Serum, Raydium, and Maps.me almost all had deep involvement from FTX-related capital.

The Solana ecosystem during this period was very much like Singapore during the British military presence: superficially prosperous, with good-looking data (TVL once exceeded $12 billion), but the foundation was fragile. A large amount of on-chain activity came from Alameda's market-making funds circulating within the ecosystem; the real organic demand was far less healthy than the data suggested.

Singapore relied on British military consumption; Solana relied on SBF's capital. The common feature of both is: the prosperity was real, but its source was exogenous, concentrated, and could disappear at any time.

The Collapse of the Umbrella

In November 2022, FTX went from the world's second-largest exchange to a pile of ruins in 72 hours. The impact on Solana was systemic: Serum's governance keys were controlled by FTX, paralyzing the project; treasury assets of numerous ecosystem projects were frozen within FTX; the high concentration of SOL staking was exposed; market confidence plummeted to zero, and developers began to leave.

This was Solana's "1968 moment." The protective umbrella wasn't slowly withdrawn; it was blown up overnight.

Chapter 2: How a Small Country Without Resources Survives—Solana's Underlying Endowments

Singapore's "Only Resource": Geographic Location

Singapore has no oil, no minerals, not even fresh water—it has to be imported from Malaysia. But it has one thing given by nature: the strategic location of the Strait of Malacca. About 25% of global maritime trade passes through here. Lee Kuan Yew figured out one thing early on: I don't need to have resources; I just need to be the best node for the flow of resources.

Solana's "Only Resource": Performance and Cabal

In the world of public blockchains, Solana also lacks Ethereum's first-mover advantage, Bitcoin's narrative myth, and Cosmos's modular flexibility. But it has one thing: extreme performance at the native layer. 400-millisecond block times, a theoretical peak of 65,000 TPS, and extremely low transaction fees (typically below $0.001).

This is not an optional technical parameter. Just as the geographic location of the Strait of Malacca determined that Singapore could become a trade hub, Solana's performance characteristics determine that it is naturally suited to carry high-frequency, small-amount, massive on-chain activities.

Geographic location is to Singapore what block speed and transaction cost are to Solana: this is the entry ticket that makes the cabal willing to come here to compete.

Chapter 3: The Wisdom of Survival in the Gray Zone—From Money Laundering Hub to Meme Casino

Singapore's "Less Glorious" Intermediate Stage

This is a period of history often glossed over in Singapore's official narrative. During the rapid development period from the 1970s to the 1990s, Singapore became a regional financial center not entirely due to its "clean and efficient" reputation.

A harsh reality is: in Southeast Asia during that era, surrounding countries—Suharto's regime in Indonesia, the Marcos family in the Philippines, the military junta in Myanmar—generated a large amount of funds that needed "cleaning." These funds needed a safe,不问来路的 (doesn't ask about the origin), predictable legal system to park. Singapore恰好提供了这样的环境: strict bank secrecy laws, efficient financial infrastructure, and an unspoken pragmatic attitude of "as long as you follow my rules, I won't追究你的钱从哪来 (pursue where your money came from)."

Business has no moral judgment, only survival strategies. A small country without resources, in its initial stages, must accept some "imperfect money" to accumulate sufficient capital stock for future transformation.

The key is: Singapore never let things slide. While attracting funds, it always maintained extremely high administrative efficiency and legal certainty (Temasek and GIC are among the world's top 10 sovereign wealth funds). You can bring gray money, but you can't cause trouble in my territory. This "orderly gray" is an extremely delicate balancing act.

Solana's Meme Season and Pump.fun (2023-2024)

After the FTX collapse, Solana faced survival pressure no less than Singapore in its early days of independence. TVL dried up, developers left, the narrative collapsed. What it needed at this time was not "correct" growth, but "any form of" growth—survive first.

From late 2023 to 2024, the Meme wave swept Solana. The emergence of Pump.fun lowered the barrier to Meme issuance to almost zero: anyone could create a token in minutes, no code, no audit needed. The wealth creation myths of Memes like BONK, WIF, and BOME attracted a flood of speculative funds.

From the perspective of traditional finance or technological fundamentalism, this was simply a disaster. The Solana chain was filled with Rug Pulls (project founders absconding), Sniper Bots (front-running bots), and countless zero-value shitcoins. But if you understand it through the framework of Singapore's history, you find it strikingly similar and full of rationality:

Meme is to Solana what gray funds were to early Singapore—it can't make it onto the big stage of tech geeks, but it brings three key things:

-

Capital inflow (foreign exchange reserves): Meme trading brought massive on-chain transaction volume and fee income, directly enriching the validators' economic model and stabilizing the basic operation of the network.

-

User base (population): Millions of new users touched a Solana wallet (Phantom's downloads soared during this period) for the first time, even if they initially came to gamble.

-

Infrastructure stress testing (urban construction): The extreme transaction load during Meme peaks exposed the real bottlenecks of the Solana network, forcing the accelerated development of key infrastructure like the Firedancer client.

Singapore's wisdom lies not in "accepting gray funds," but in "never stopping the construction of正规的制度基础设施 (formal institutional infrastructure) while accepting gray funds." Similarly, the key for Solana is not the Meme itself, but whether it is simultaneously advancing truly valuable underlying construction under the cover of the Meme frenzy.

Chapter 4: Currency as Sovereignty—The Governance Logic of Token Economics

Singapore's Monetary Policy Philosophy

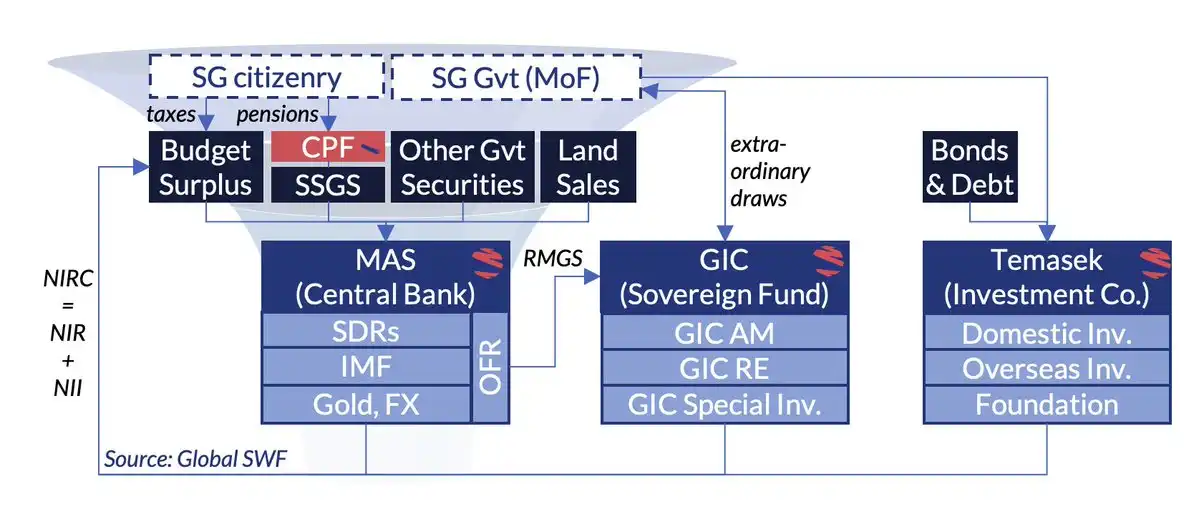

The monetary policy of the Monetary Authority of Singapore (MAS) is unique among global central banks: it does not use interest rates as the primary tool but manages the Singapore dollar's exchange rate fluctuation band to regulate the economy. An appreciation channel is used to curb inflation and attract capital; a depreciation channel is used to stimulate exports and maintain competitiveness.

The core logic is: currency is not static; it must be dynamic and responsive. How much money to print, whether to appreciate or depreciate the currency, depends on the needs of the current economic cycle. Excessive issuance dilutes national wealth and causes inflation; excessive tightening stifles economic vitality. Good monetary policy is a continuous balancing act.

SOL's Token Economics: The Dynamic Game from Inflation to Deflation

Solana's token economics have undergone a similar evolution.

Initial Inflation Phase (Quantitative Easing): At the launch of the Solana mainnet, an annual inflation rate of about 8% was set, decreasing by 15% each year, with a long-term target converging to 1.5%. These newly issued SOLs were used to pay staking rewards, essentially a "fiscal expenditure" subsidizing validators—just like emerging countries investing heavily in infrastructure early on, you must first pay the cost to attract "citizens" (validators) to stay and maintain network security.

Introduction of Burn Mechanism (Tightening Policy): In 2023, Solana introduced a partial burn mechanism for transaction fees—50% of the base fee of each transaction is permanently burned. When on-chain activity is sufficiently active, the amount of SOL burned may approach or even exceed the amount of new issuance, putting SOL into a de facto deflationary state.

This is like a country's central bank finally having the ability to "raise interest rates": when the economy (on-chain activity) is prosperous enough, it recovers money supply to maintain currency value.

But the problem is: Solana currently lacks a truly dynamic, responsive monetary policy framework. Its inflation rate decreases mechanically according to a preset curve, and the burn rate depends entirely on market activity; there is no "smart adjustment mechanism" like the MAS between the two.

This is a deep governance problem that Solana (and almost all public blockchains) has not yet solved: the issuance and burning of tokens should not be a fixed curve but should be dynamically adjusted according to the network's "economic cycle," like the monetary policy of a sovereign state. When the network is congested (economic overheating), the fee burn ratio should be increased to抑制投机 (suppress speculation); when the network is quiet (economic recession), perhaps the staking门槛 (threshold) for validators should be lowered and incentives increased.

A truly mature public blockchain economy needs not an inflation curve written dead in the code, but a set of on-chain "central bank" governance mechanisms.

only few understand, tokens do not only appreciate by being burned.

Chapter 5: HDB Politics—"People with Assets Will Defend the Country"

The Real Crisis in Early Singapore: Not Poverty, but the Sense of Division Between Ethnic Groups

When most people talk about the Singapore miracle, they focus on economic growth. But Lee Kuan Yew himself repeatedly emphasized that the most dangerous enemy in the early days of nation-building was not poverty, but racial division.

In 1965, Singapore's population was roughly 75% Chinese, 15% Malay, and 7% Indian. The three ethnic groups spoke different languages, had different beliefs, and distrusted each other. One of the triggers for Singapore's expulsion from the Malaysian Federation was the irreconcilable racial矛盾 (contradictions) between Chinese and Malays—in the 1964 racial riots, 23 people died and hundreds were injured.

After independence, Singapore faced a残酷的现实 (harsh reality): the people on this island did not feel like "Singaporeans" at all. The Chinese identified with Chinese culture, the Malays with the Malay Federation, the Indians with India. No one had a sense of belonging to the concept of "Singapore," let alone was willing to sacrifice for it.

The fundamental problem Lee Kuan Yew needed to solve was: How to make a group of people who distrust each other voluntarily stay under the same roof and be willing to付出 (give) to maintain that roof?

HDB: Not Just Housing, but a National Binding Mechanism

The answer was HDB public housing—perhaps one of the most ingenious social engineering projects in human history.

On the surface, HDB solved the housing problem. In the 1960s, a large population in Singapore lived in squatter settlements and slums. The government built public housing on a large scale, selling it to citizens at prices far below market rates and allowing the use of the Central Provident Fund (CPF) to pay mortgages. Today, over 80% of Singaporeans live in HDB flats.

But the true genius of HDB lies in its underlying political logic. Lee Kuan Yew once said a very frank sentence (paraphrased): "A person who owns assets in a place is more willing to defend it."

The HDB system achieved at least three strategic goals simultaneously:

First, creating "stakeholders." When you are just a tenant, the rise and fall of the city have little to do with you—you can just move away. But when you own a house, your net worth is tied to the fate of the country. Housing prices rise, your net assets rise; the country falls into chaos, your assets shrink. Every HDB owner becomes a "shareholder" in Singapore's national fortune.

Second,强制种族融合 (forced racial integration). This is the most underestimated design of the HDB system. HDB implements a strict Ethnic Integration Policy (EIP): each HDB community has quotas for the proportion of Chinese, Malays, and Indians, ensuring that no single-ethnic enclaves form. Your neighbors are necessarily different from you. Children play together downstairs, attend the same schools. After a generation, racial barriers were slowly dissolved by the forced mixing of physical space.

Third, linking personal wealth to the quality of national governance. The appreciation of HDB flats depends on Singapore's continued prosperity and good governance. Good governance leads to area development and improved amenities, which升值 (appreciates) your flat. This creates a powerful positive feedback loop: citizens have an incentive to support good governance because good governance directly enhances their asset values.

A single HDB flat accomplishes three tasks simultaneously: "binding interests—eliminating divisions—incentivizing governance." This is not just housing policy; it is the cornerstone of the nation. To secure the outside, one must first secure the inside—Lee Kuan Yew understood this deeply.

Solana's "Race Problem": A Divided Community

Switching perspectives back to Solana. After the FTX collapse, the Solana community faced a degree of fragmentation no less than that of Singapore in 1965.

There are at least three "ethnic groups" on the chain with截然不同 (distinctly different) interests:

Speculative traders and Meme players. They are the largest contributors to on-chain activity on Solana, bringing transaction volume, fees, and话题热度 (topic heat). But they have no loyalty to Solana; they go to whichever chain has the hype, essentially a floating population.

Native developers and builders. They have invested significant time and technical capital in building DeFi protocols, infrastructure tools, and DePIN projects on Solana. Their relationship with Meme speculators is微妙而紧张 (subtle and tense)—they need them (users and流量 (traffic)) but also dislike them (lowering the ecosystem's seriousness).

Validators and stakers. They are the cornerstone of network security, investing real money in hardware and staking capital. They care about network stability, staking yields, and the long-term value of SOL, neither participating in nor caring about short-term speculation.

The competitive tension between these three groups is divisive. Meme players complain about the unfairness of the priority queue for retail users during network congestion; developers complain that Memes吸走了 (suck away) all the attention and funds; validators complain about the opacity of the MEV distribution mechanism. Without a mechanism to align the interests of these three parties, the centrifugal force within the Solana community will only grow.

Where is Solana's "HDB"?

Lee Kuan Yew's wisdom—making citizens hold assets, binding personal interests to collective fate—what启示 (enlightenment) does it offer for Solana? Some mechanisms similar to "HDB" already exist in the Solana ecosystem, but they are far from systematic:

The Staking mechanism is the design closest to "HDB." When you stake SOL, you lock your assets into the network, and your收益 (returns) directly depend on the network's health. Stakers naturally become "shareholders" in network security. But currently, Solana's staking is mainly concentrated in the hands of large holders and institutions; the participation rate and sense of participation of ordinary users are insufficient—this is like if HDB flats were only sold to the rich, the poor would still be tenants, and the effect of "interest binding" would be greatly reduced.

Governance tokens and airdrops are a form of "house distribution." Ecosystem projects airdropping governance tokens (like JTO, JUP airdrops) to early users and developers are essentially "distributing assets"—turning participants from bystanders into stakeholders. Jupiter's JUP token airdrop covered nearly a million active wallets, instantly creating a large number of "homeowners" with a sense of belonging to the Jupiter protocol. If designed properly, this mechanism is no less effective than HDB.

Superteam DAO's globalized community is an attempt at "ethnic integration." Superteam establishes localized communities in different countries and regions, allowing developers from India, content creators from Turkey, and DeFi users from Nigeria to collaborate within the same organizational framework. This is somewhat like HDB's ethnic quota system—reducing cliques and factionalization through structured mixing.

But what Solana still lacks is a truly systematic "asset binding—interest alignment" mechanism. Imagine a more complete version: if the Solana ecosystem could establish a system where developers receive continuous protocol-layer revenue sharing for deploying successful applications on the chain; where active users accumulate some non-transferable "on-chain credit" or "citizenship" through long-term use; where validators' rewards are linked to the reliability of their service and their contribution to decentralization—then the personal wealth of every participant would be tightly bound to Solana's overall prosperity.

When speculators, developers, and validators all become "homeowners," not just "tenants," they will truly be willing to fight for the long-term interests of this chain. This is the most profound lesson Lee Kuan Yew taught us with an HDB flat: people won't fight for abstract ideals, but they will fight desperately for their own assets.

Chapter 6: The Crossroads of Transformation—"What Comes After?"

Singapore's Three Leaps

Singapore's economic transformation can be roughly divided into three stages:

First Stage (1960s-1970s): Labor-intensive manufacturing. Utilized low-cost labor to attract multinational companies to set up factories, earning foreign exchange and solving employment. This was the "survival" stage.

Second Stage (1980s-1990s): Financial and trade hub. Utilized geographic location and institutional advantages to become a regional capital distribution center and shipping logistics hub. Gray funds played a non-negligible role in this stage. This was the "gaining a foothold" stage.

Third Stage (2000s-present): Knowledge economy and high-end manufacturing. Heavily invested in education, attracted talent (Global Talent Program), developed high-value-added industries like biomedicine, semiconductor design, and fintech. Simultaneously tightened anti-money laundering regulations, gradually "cleaning" the financial system. This is the "defining itself" stage.

Each leap did not happen naturally; it was an active transition to a new model before the profits of the old model were exhausted. This requires极强的战略定力和政治意志 (extremely strong strategic determination and political will)—because transformation means主动放弃 (actively giving up) part of the current benefits.

Solana's Current Position: The End of the Second Stage

Using Singapore's framework for定位 (positioning), Solana is currently in the middle to late second stage. The capital and user红利 (dividends) brought by the Meme wave still exist, but the marginal effects have begun to diminish. Market fatigue with the next 100x Meme is rising, and if Solana cannot complete its transformation before this wave of heat subsides, it risks becoming a "casino chain"—just as if Singapore had remained stuck in the gray finance stage, it might be just another Cayman Islands today.

What Could Solana's Third Stage Be?

I don't know either, but it's definitely not some AI Agent.

Conclusion: The Fate of Public Blockchains is Ultimately the Fate of Governance

Looking back at Singapore's story, its success was not due to luck but because at every critical juncture, it made counterintuitive yet logical and commonsense decisions: opening up when it should (even accepting gray funds), controlling when it should (maintaining order with strict laws and harsh punishments), and transforming when it should (even if it meant sacrificing current benefits).

Solana stands at a similar crossroads. The Meme热潮 (craze) has given it life-sustaining ammunition and an active user base, but if it cannot accomplish three things before this红利 (dividend) subsides—establish a dynamic token economic governance mechanism, achieve true decentralization to win institutional trust, and cultivate a core industrial ecosystem beyond Memes—then it could be like countless small countries in history that "almost succeeded," hesitating at the window of transformation and ultimately being淘汰 (eliminated) by the times.

The competition among public blockchains is about narrative in the short term, technology in the medium term, and governance in the long term.

A token is not just a price symbol; it is the currency of a digital nation. And monetary policy has never been a dead written curve but an art of balance, timing, and restraint.

Postscript:

This article uses Singapore's development history as an analogical framework to analyze the Solana public blockchain ecosystem, aiming to provide a new perspective for thinking about public blockchain governance. The historical narrative of Singapore has been simplified to serve the analogical logic and does not constitute a comprehensive evaluation of Singapore's policies.

Also, you ask if the same comparison framework can be used for other public blockchains, sure, why not?