This column combs the trading status of the spot market and futures market within the day, and analyzes the trading performance of BTC and the overall market. Help investors tap effective trading signals.

Market view

BTC, Eth and other mainstream currencies rebounded in the short term. On the brin online track, the price performance was relatively strong, and further change signals appeared at any time. The current trend is favorable for bulls, and the contract position has reached a recent high, indicating that the willingness to do long has increased.

goods in stock

1. Exchange BTC stock

The stock of BTCs in the exchange fell to 2.303 million BTCs on March 23. From the change of BTC stock in the exchange, the outflow increased from February to March, indicating that the selling pressure of BTC continues to reduce. Since July 26, 2021, the trend of BTC outflow from the exchange has continued, which means that investors' willingness to operate has decreased and the price of BTC has been supported by growth.

2. Market value and trading volume of the whole network

In the past two hours, the overall market trading volume was US $102.1 billion, and the overall market value increased by 2.5% to US $2 trillion. Pay attention to the trading volume and market value performance of the overall market in the past three months. The market value fluctuation space of the whole network runs between us $16423 billion and US $25005 billion.

contract

Contract transactions in mainstream currencies such as BTC can find spot prices and improve the direction of price operation. At the same time, it can also provide hedging methods for spot investors. Analyzing the long and short position direction, position change and leverage performance of the contract can help us confirm the trading signal.

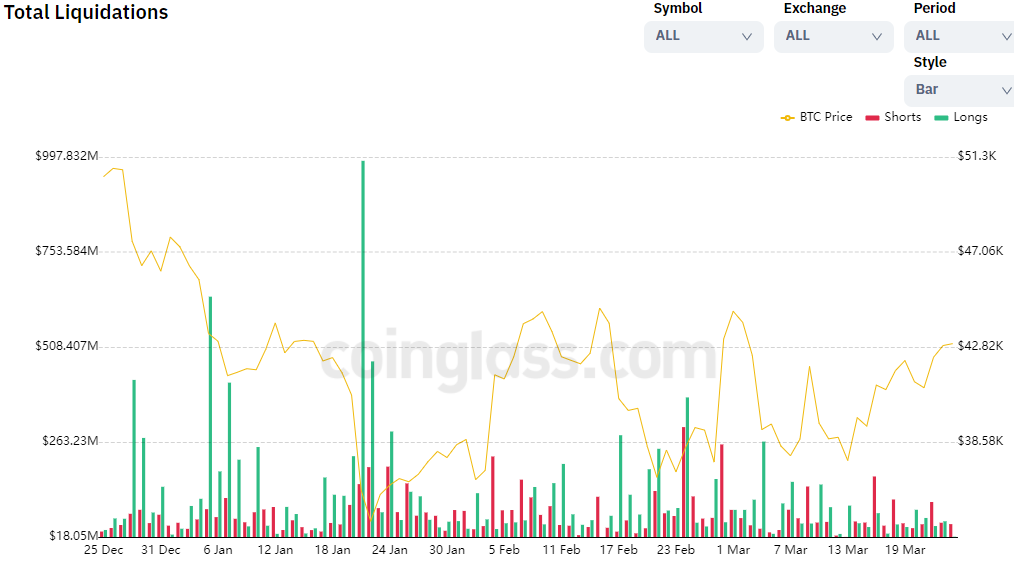

1. Statistics of warehouse explosion in the whole network

The number of open positions indicates the effect of the release of market resistance during the price operation. The larger the number of open positions, the greater the reverse capital strength. After a short period of time, the excessively high position explosion amount can also prompt the price reversal signal. Because the fund increases the number of positions in the opposite direction in a short time, promoting the reverse operation of the market in a short time.

Network wide contract explosion

On March 24, the empty single explosion warehouse of the whole network contract reached US $35.31 million, and the multi single explosion warehouse of the whole network reached US $11.68 million. From the absolute value of position explosion, it is a low level in the short term. At the same time, the number of empty single positions has been generally large since mid March. At present, the reverse view of position explosion is relatively favorable for price rise.

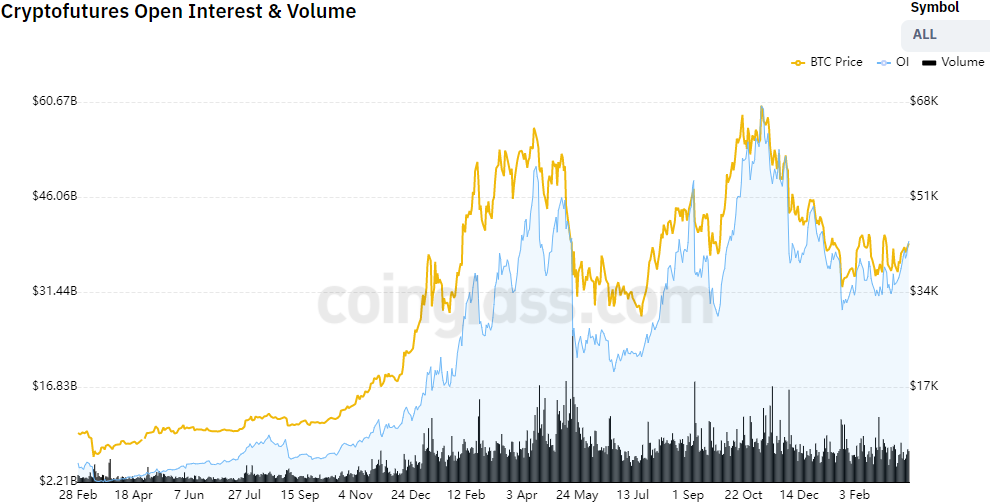

2. Statistics of positions and turnover of the whole network

The trading volume and position of the whole network contract were stable. On March 24, the position shrank by US $39.2 billion, a slight increase of 1.8%; The turnover was US $110.3 billion, a slight decrease of 5.9%. It is worth noting that the contract position is the highest level since January 5, indicating that the overall market heat is continuing to grow.

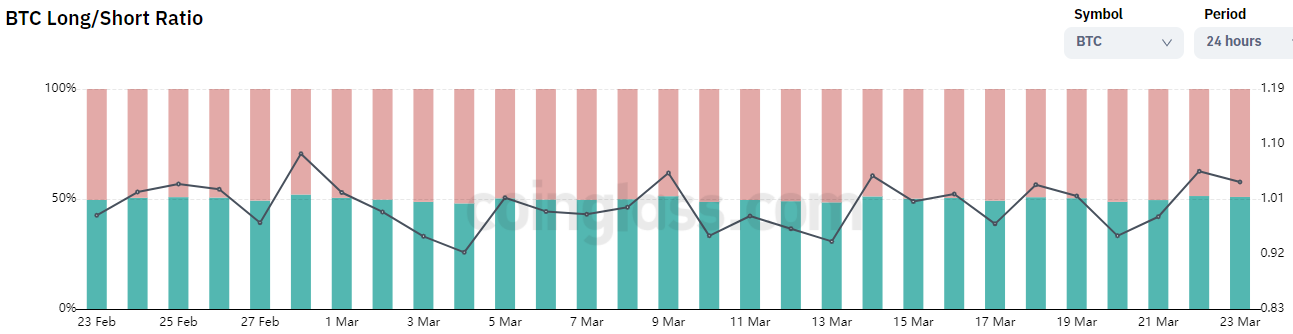

3. Statistics of long and short positions of the exchange

The proportion of long and short positions in the exchange intuitively reflects the strength of long and short positions, and the dynamic proportion of long and short positions better verifies the trading signal. When multiple positions account for a large proportion, it indicates that the buyer has strong strength, and the BTC price is easy to rise but difficult to fall. On the contrary, the short strength is strong, suggesting a short signal.

On March 24, the proportion of multiple and empty orders in BTC was 1.04%, and the proportion of multiple orders was 50.93%, while the proportion of empty orders was 49.07%. Many parties dominated for the third consecutive trading day, and BTC had strong short-term upward momentum.

4. Contract capital rate

The higher the contract capital rate, the more information the bulls have about the price rise. The latest capital rate value of BTC shows that the fluctuation space of capital rate since 2022 is small, and the financing cost on more trading days is lower than 0, which means that the cost of financing for investors to buy BTC is very low. On March 23, the capital cost of BTC was -0.00024. The capital cost of BTC is lower than 0, the market is still in the bottom confirmation stage, and the opportunity of low absorption is relatively low.