Bloomberg Intelligence’s senior commodity strategist, Mike McGlone, is predicting that Bitcoin (BTC) is headed to a six-figure price.

McGlone says that the oil prices will persist on a downward trend throughout the second half of 2022 towards a price of $50 a barrel and this will trigger deflationary trends worldwide.

The deflationary impact will consequently send the price of gold rising to $2,000 an ounce and also boost the price of Bitcoin to $100,000, according to the Bloomberg Intelligence strategist.

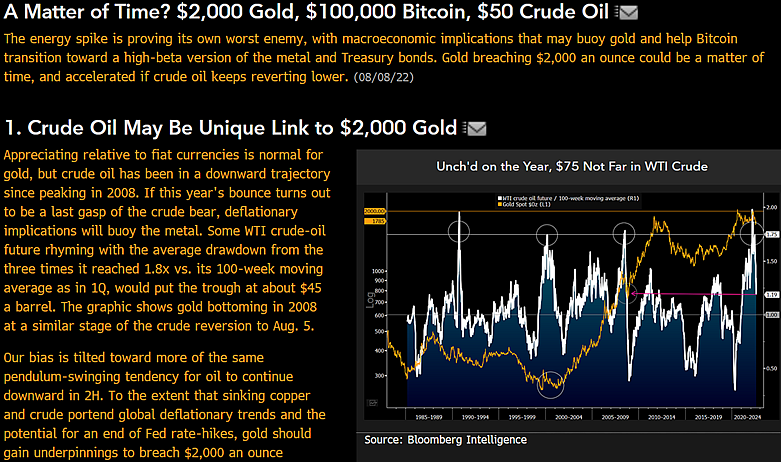

“A Matter of Time? $2,000 Gold, $100,000 Bitcoin, $50 Crude Oil –

The energy spike is proving its own worst enemy, with macroeconomic implications that may buoy gold and help Bitcoin transition toward a high-beta version of the metal and Treasury bonds.”

Source: mikemcglone11/Twitter

Bitcoin is trading at $23,400 at time of writing.

This is not the first time that McGlone is predicting that Bitcoin will reach a six-figure price. In March, when the flagship crypto asset was trading at over $40,000, the Bloomberg Intelligence strategist predicted that Bitcoin would first undergo a correction before surging to $100,000.

“But Bitcoin is the gold in the space. And it’s still speculative. I just really think it needs to be shaken out a little bit and then go back up as a whole market.”

Bitcoin fell to a year to date low of around $17,622 in June.