Following the undercover battle in the underlying infrastructure of the wallet track in the previous article, many viewers have been urging for an update. So, Fourteen Jun will dive into the competition again in 2025.

Hyperliquid is undoubtedly the hotspot of the year. This time, let's look at the intricacies like insiders, connecting the events to see how wallets, exchanges, DEXs, and AI trading are all entangled in this melee!

1. Background

In 2025, the author has basically researched all the Perps (perpetual trading platforms) on the market, witnessing Hype's market 5x growth and peak halving (9->50+->25). Amidst the ups and downs, did it truly fall behind competitors? Or were there hidden worries about reduced platform revenue due to the openness of its hip3 and builder fee development?

The Perps track itself is also seeing emerging competitors. Recently, Aster, Lighter, and even Brother Sun (Justin Sun) entered the fray with sunPerps, whose promotional Twitter Space even set a new record for online attendance in a Web3 industry launch event.

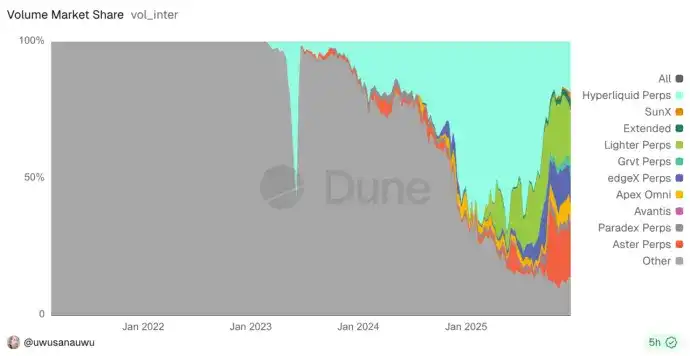

As shown in the figure below, one can see the state of this chaotic battle among rivals. Interestingly, this is also an ongoing process of a predetermined market being carved up.

Recalling the competition among all DEXs during the DeFi Summer, including Uniswap, Balancer, Curve, and numerous Uniswap fork projects like Pancakeswap, etc.

The present moment for Perps is exactly like that moment during DeFi Summer. Some want to be the platform, some want to aggregate others, some want to challenge the leader, and some just want to scrape the leftovers.

Over the past year, various wallets have been vying to launch perpetual trading capabilities at the DEX entry point. Metamask and Phantom took the lead, followed by Bitget's integration news last week. Other startup products like Axiom, basedApp, xyz (using hip3), and multiple AI trading platforms are also getting a share of the pie through integration.

At this point, the wallet track is also undergoing a new round of undercover warfare.

Everyone is competing to integrate Hyperliquid's perpetual trading capabilities. Is this behind the红利 (dividend) of technological openness, the temptation of rebate mechanisms, or simply a true reflection of market demand? Why have some major platforms remained inactive? Have the early integrators seized the market through this?

2. Ecological Origin, Builder Fee & Referral Mechanism

Hyperliquid's rebate mechanism mainly includes the Builder Fee combined with Referral (rebate).

The author has always considered this a very disruptive mechanism. It allows DeFi builders (developers, quantitative teams, aggregators) to charge additional fees as service revenue when placing orders on behalf of users. The total fee for users placing orders on these platforms and the official website itself remains unchanged.

Its essence is actually similar to Uniswap V4's hook mechanism. Both offer their order book (or liquidity pool) as infrastructure for various upstream platforms to integrate. This makes it easier for them to attract user groups from different platforms, and different流量 platforms (wallets) also have more comprehensive ecological products to serve the diverse needs of their users.

This mechanism initially brought dividend收益 (收益 - income) of over ten million USD to some projects, with significant early effects, but it subsequently declined.

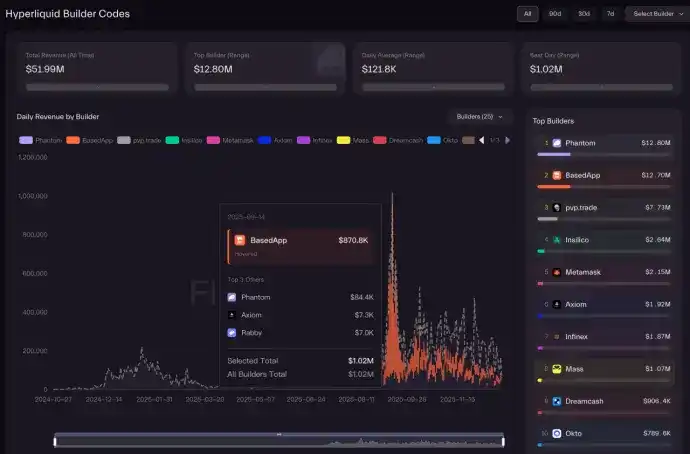

From the figure, we also see many points worth pondering.

• Why is there a 5x difference in integration收益 between Metamask and Phantom, given Metamask's user base is not smaller?

• Why is the收益 here for basedApp and Axiom vastly different? Where is Jupiter?

• Is the 12M dividend收益 a lot or a little? Is it short-term or long-term?

• Are platforms that only lightly integrate HypeEVM or the native coin at a disadvantage?

• Why are Bn (Binance), Okx, etc., not among them?

3. PerpDex's Open Strategy

To answer these questions, we must first understand how various platforms integrate.

3.1 Open API Integration Method

Actually, each Perps platform has opened its API, which is very comprehensive. Almost each has its own definition method, but the provided modules are大致 (roughly) as follows: Query type (account status, positions, orders, market data, K-lines, etc.), Trading type (place order, cancel, modify, adjust leverage, withdraw, etc.), Subscription type (WS real-time price推送 (push), order book, position changes).

Because this system itself needs these APIs provided to market makers for market making. The user side is just changing the trading direction, but user-side won't be able to contact like market makers can, so it must add some control.

Hence, the rate-limiting mechanism is necessary. Hype's is based on address + IP dual rate limiting, which can dynamically adjust the rate limit threshold with trading volume. High concurrency may face rate limit challenges.

The advantage of this official API solution is quick integration and implementation, no need to build your own nodes, low data latency, and good state consistency.

But the disadvantages are also obvious:可能面临 (may face) IP/region restrictions, susceptible to rate limiting impacts. Rate limiting is less problematic for a single user, but for a platform, it's hard to achieve because user volume can increase at any time, making dynamic scaling difficult.

There's also the update issue. Remember, apps have release restrictions for code modifications. If the official API upgrades change or gets rate-limited, the app side loses control. Besides becoming a traffic provider, they also have to额外承担 (bear additional) customer complaints and risks.

3.2 Read-Only Node Integration Method

Hyperliquid has a dual-chain structure, EVM and core chains, integrated into one program and closed-source封装 (encapsulated). It's hard for the outside to破解解读 (crack and read) the specific content. Officially, they only support project parties deploying this kind of read-only node (can obtain order, K-line, transaction data, but does not support sending transactions).

Moreover, not all historical data is open. The data volume here is huge: about 1T+ of data is added in just 2 days. After a year, if historical data isn't archived, the cost itself is hard to cover the收益.

If a project party deploys a read-only node to reduce the frequency of reading the official API and thus lessen rate limit issues, this is currently the officially recommended approach.

Adopting this solution also has significant technical challenges: occasional block drop phenomena, massive storage costs, missing historical data. And the node's data methods must be modified.

The author believes the biggest problem is the consistency issues brought by this half-open mechanism.

For example, if I use the K-line data from a read-only node to place an order, but the node itself is delayed (this本身 (itself) has a probability of occurring), and I can only use the official API to place the order, which has no delay. The data here might be inconsistent, so my market order could be filled at an undesired price.

Whose responsibility is it? Does the platform earn enough to cover compensation here? How much cost does the platform need to improve stability? Is it appropriate to just shift blame?

3.3 Market Choices

This shows a divergence, with different approaches from various players.

• Metamask, as a typical representative of a tool-oriented positioning, directly uses frontend integration with the open API, even open-sourcing the integration code. This simple and crude method brings fast launch efficiency. The author is also rare to see such a conservative head wallet platform make such a quick market move.

• Others doing the same include Rabby, Axiom, BasedApp.

• Trust Wallet has also integrated Perps, but it对接 (connects) to the BN系 (BN ecosystem's) Aster platform,显然 (obviously) giving the green light to their own products. But how internal rebates work is uncertain.

• Phantom, rising from the Solana Meme wave, appears more focused on the pursuit of experience here. They use the read-only node integration method, and even order placement operations are relayed through the backend, rather than the client directly calling the official API.

Actually, there are some amazing products on the market with different angles and choices.

For example, Trade.xyz is currently the platform with the highest trading volume on Hip3, not seeking the red ocean battle of the existing market but directly开拓 (pioneering) stock trading capabilities.

VOOI Light is also very capable (engineering-wise), an intent-based cross-chain perpetual DEX. Its core lies in simultaneously integrating multiple Perps DEXs. It can be said they use engineering effort to take multiple paths of the above platforms simultaneously. But the beauty is不足 (lacking) as it's also stuck on the complexity of multi-integration reserve funds, resulting in a less smooth experience.

Finally, the author recently experienced several AI trading platforms, almost all using open API integration + backend integration方案 (solutions) for multiple Perps. The experience is cutting-edge. Some are pure LLM large model text interaction, some are AI decision-making + follow trader methods (the underlying layer can also link with TEE custody solutions like Privy), achieving AI-assisted Perps trading without passing private keys to the project party.

Different solutions bring different experiences, which can explain some of the differences in the final rebate effect data.

4. Reflections

The previous social logins can only solve the recovery problem, but not automated trading.

4.1 Reserve Fund Complexity

This is actually the most easily overlooked. Hyperliquid's complexity far exceeds imagination; it's not simply "integrate and use."

Various platforms initially optimistically viewed its integration with an aggregated DEX mindset but also ignored that its essence is not a Lego model. After integrating Hyperliquid, if the market declines later, will the functionality remain? How many wallets are now delisting previous inscription protocols? And if the platform closes, will users go to the official platform to find their open positions?

Furthermore, if Hyperliquid falls out of favor, and perhaps Aster or Lighter become popular, will there be migration to new platforms? The APIs of various parties are not完全一致 (完全一致 - completely consistent). How to migrate? How to run parallel?

To smooth these out, it's unavoidable to increase the complexity of the experience.

Ultimately, if a user wants to use a large and comprehensive entry point, why not use the official one itself?

Frontend integration brings fast experience and coverage, but Metamask seems to have eaten a dumb loss, not making much money but白白提供 (providing for free) its user traffic.

Backend integration brings a premium experience, which is the core reason Phantom earns the most收益, but it also comes with huge costs. The final ROI (Return on Investment)收益 is perhaps only known to themselves.

4.2 Why Can't the Total收益 Break Through Higher?

Actually, reviewing our own preferences (focusing on advanced Perps players) for using platforms like Hyperliquid, we still prefer the complete official entry point and operate more on the PC端 (PC end). The main reasons are直观看到 (seeing directly) stop-profit/stop-loss settings, chart monitoring, margin modes, and other advanced functions. After all, this track itself has more high-end players.

The demand for using the移动端 (mobile end) is "monitoring and responding to market changes anytime, anywhere, for position risk and price management, not for complex analysis."

So Phantom's advantage lies in bringing new users an initial experience, then持续下行 (continuously declining), because its focus is still on the mobile end.

BasedApp, which has both App and web entry points, caters to both needs. However, due to competition from the official entry point on the web end, the上限 (upper limit) isn't high either.

But Hyperliquid's own App will be launched soon, so this market itself will become increasingly limited.

It can only be said that architectural differences determine the value of integration, but the size of the value depends on the depth of integration. Ultimately, the ceiling of this model is essentially internal competition; users contributed by entry platforms很难维持 (are hard to retain) in the original platform.

If wallets can provide advanced mobile functions (advanced charting, alerts and notification systems, auto trading), then there is indeed differentiated value. We can see后续 (subsequently) Phantom updates quickly, also launching various advanced functions, just to retain these users.

The way to break the situation lies in AI trading, auto trading (trading models not available on the official platform), and multi-Perps aggregation, following the same path DEXs took. But there are also problems like the difficulty of solving multi-platform reserve fund scheduling and the high efficiency of AI losing money. Even with industry-general private key custody methods (Privy, TurnKey)加持 (blessing), it still belongs to: users who know how will naturally know, those who don't can't learn.

4.3 User Growth & Ecological Niche Supplementation

Of course, the original intention of many platforms is that they can accept it not making money. After all, relying on手续费分成 (fee sharing) is like fishing for渣 (dregs) in the soup. But if it can attract users who use Perps or meet the perpetual trading needs of existing users, it is also a good ecological niche supplement.

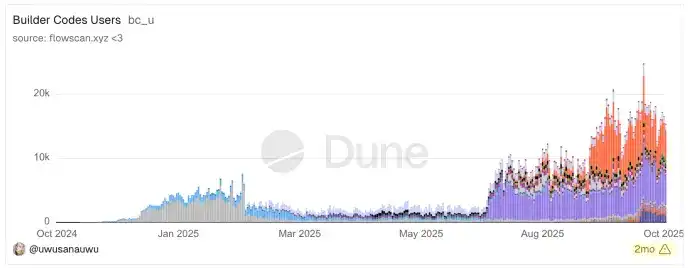

We can conclude this by grabbing some HL on-chain data for analysis because this group is actually very small.

From the figure below, the user体现 (reflection) of each integration is only a few thousand daily active users, totaling just over 10-20k.

Moreover, looking at Hyperliquid's own monthly active users, the essence of its收益 is based on a whale service model, belonging to a typical contract market Matthew effect and inverted pyramid fund structure.

Currently, HL's total wallet addresses reach about 1.1 million, with monthly active users at 217k and daily active users at 50k. But the key here—the top 5% contribute 90%+ of the OI and Volume, forming a typical pyramid structure.

The top users accounting for only 0.23% (fund range $1M+,共 (totaling) over 500 people) control 70% of the open interest ($5.4B). Among them, over 100 top users have an average holding of高达 (as high as) $33M, their OI (Open Interest)占比 (proportion) is 920 times their user proportion.

In contrast, the bottom users accounting for 72.77% (150k users) contribute only 0.2% of the contract volume, with an average holding of仅 (only) $75.

This structure shows that the contract market is essentially a博弈场 (battleground) for professional institutions and high-net-worth individuals. A large number of retail users虽然构成 (although constitute) the user base and activity, their capital size is almost negligible.

This structure actually reflects a counter-intuitive fact: indeed, Hyperliquid itself has very high收益,跃进 (leaping into) one of the most profitable exchanges in just one year.

But its收益 essentially comes from high-end玩家 (players) whales, whose motivation might be anti-censorship, or openness and transparency, or quantitative trading driven.

But the significance of integration by various platforms actually only brings常规 (regular) users. So this requires a long-term user education process to possibly shift those playing Perps in CEXs to the homogenized competition of Web3 Perps.

5. In Conclusion, Is Integrating Perps Really a Good Business?

Ordinary projects must adapt to the market, but when a platform's heat peaks, the market adapts to it. Hyperliquid is currently receiving such treatment, but it may not be able to守住 (maintain) this treatment. Although it can explain that the sharp increase in trading volume of other competitors in the market is due to new airdrop expectations, leading to non-genuine trading results.

Moreover, many of HL's measures are relatively correct. Compared to many past platforms that often wanted to do everything themselves and reap all the红利, the author点名批判 (names and criticizes) OpenSea, which could折腾出 (stir up) a forced royalty system, forcing the market to follow the leader. Each time had fixed high costs, intervened in the flow of goods, affected the market's real pricing, and eventually left countless NFTs as family heirlooms.

In HL, they opened the EVM and all various Dex Perps APIs, so the market quickly saw a bunch of derivatives.

RWA assets, especially U.S. stocks and gold, are becoming new traffic entry points and differentiated growth points in the current Perp DEX field. TradeXYZ's cumulative Perp volume of $19.1B, weekly average of $320M, daily average of $45.7M, is the best proof.

Hyperliquid's generosity is also visible in airdrops and buybacks. Often, staking HYPE for ADL profits also has considerable expected收益.

Going round and round, the龙头之争 (fight for the leading position) is for those few to worry about. Returning to this year's wallet integration undercover battle, integrating third-party Perps is mostly a low-ROI business, whether from user growth收益 or platform commission earnings and stability investment, it can't be considered a good business.

It can be imagined that after seeing the real收益 situation post-integration, most platforms, still reluctant to give up the红利 of the Perps track, will move towards self-research and大量拉新宣发 (extensive user acquisition promotion). The track battle is not over; it will continue to burn for another year. But only new users pulled from non-CEX are truly effective users.

Disclaimer

This article is information-intensive, as many architectural overviews are highly condensed, and the technology is not fully open source, based on analysis of published information.

Additionally, purely discussing from a technical solution perspective, with no positive/negative evaluation of any products intended.