LaunchPad 一直是加密领域财富效应的象征。虽然今年加密市场行情处于下行通道,多个项目上线即破发,但多家头部交易所上线的 LaunchPad 项目仍有不错的表现。

本文将综合比较各大交易所 LaunchPad 项目的回报率、平台上新速度、玩法模式等维度,揭秘哪家头部交易所的 LaunchPad 更具造富效应。

1. 项目收益率对比

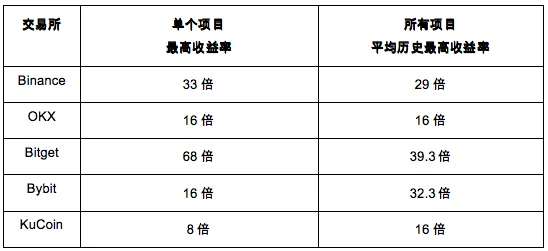

根据 Coingecko 和 CryptoRank 的数据, 2023 年以来头部交易所的 LaunchPad 项目上线后都有不错,平均最高收益率均在 10 倍以上。

其中,表现最为亮眼的是 Bitget。其 LaunchPad 所有项目的平均历史最高收益率为 39 倍,排名第一;而 Bybit 和 Binance 紧随其后,平均历史最高收益率分别为 32.3 倍和 29 倍。以单个项目的最高收益率而言,Bitget 于 7 月份上线的 TYPE 最高涨幅达到 68 倍,是所有交易所 2023 年上线 LaunchPad 项目收益率最高的。

(2023 年头部交易所 LaunchPad 项目表现)

另外,平台币的价格表现也间接决定着 LaunchPad 项目的收益率。由于参与各大交易所的 LaunchPad 均需持有平台币,如果平台币价格波动较大甚至出现了暴跌,将导致 LaunchPad 项目的收益无法弥补平台币下跌的亏损。

今年以来,平台币整体表现差强人意。虽然多数平台币的价格较年初有所上涨,但却不及比特币 2023 年的上涨幅度(BTC 较年初上涨 107% )。所以,如果以 BTC 本位计算,绝大多数平台币的表现都不及格。而 Bitget 的 BGB 是唯一一个涨幅超过 BTC 的平台币,目前其价格较年初已上涨了 168% ,成为了 2023 年表现最好的平台币之一。

(2023 年头部交易所平台币表现)

2. 项目上新速度对比

此外,上线新项目的数量也从侧面反应出了一个 LaunchPad 的造富能力。

进入 2023 年以来,单从上币数量来看,Bitget 更为积极。截止目前 Bitget 的 LaunchPad 已上线了 5 个项目。10 月 26 日,Bitget 宣布将上线新一期的 LaunchPad——T 2 T 2 ,这是一个类 Friend.tech 项目。而 Binance 已在今年上线了 3 个 LaunchPad,排名第二。

(2023 年头部交易所 LaunchPad 上线项目数)

除了上线更多的 LaunchPad 项目,Bitget 也首发上线了多个行业热门币种(如 BLUR 等);除此之外,Bitget 还设置热门叙事币种专区,如 AI、MeMe、BRC 20 等。

3. 玩法模式对比

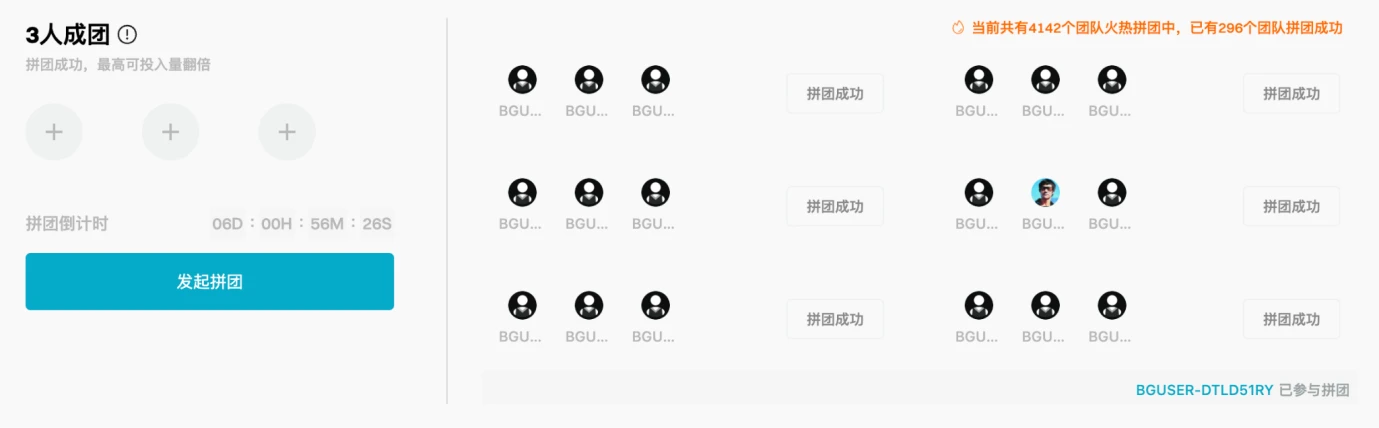

经过了多年的发展,目前 LaunchPad 的玩法已基本固定——通常是持有平台币获得参与抽签的资格,中签后兑换新项目代币。各大主流交易平台均采用这种模式,但它对用户的吸引力却在减少。

近期,Bitget 在新一期 LaunchPad 中采用全新的拼团模式,降低了参与门槛(50 BGB 起投)。从参与人数来看,该项目开启不到一周,已有 4000 多个团队拼团中,参与人数近万人。

小结

从以上分析来看,Binance 在 LaunchPad 上仍具号召力,保持着较高的上新速度和投资回报率,而 Bitget 等平台也正在迎头赶上,不仅有更高的投资回报率和上新速度,还有更多元化的玩法。