原创 | Odaily星球日报

作者 | Loopy

还记得 XEN 吗?去年 10 月,XEN 一经推出就引爆了加密市场,参与该项目的地址数量高达百万级,一度让以太坊的 Gas 费用高居不下,Odaily星球日报曾在《谷歌前员工?曾主导归零土狗?解析 XEN 团队背景疑云》一文进行解读。

刚刚过去的这个周末,一款和 XEN 类似但又有所不同的项目近两天突然在加密社区蹿红。

10 月 28 日,TITAN X 代币发布,DEXTOOL 数据显示该代币上线后价格最高涨幅约 1800% 。仅仅持续了一天,TITANX 价格开始大幅跳水,从高点下跌约 94% ,部分社区用户对于回购资金及机制是否生效和正常运作提出了质疑。

从爆红到接近“归零”,TITANX 发生了什么?未来又能否复苏?Odaily星球日报为你带来关于详细解读。

TITAN X:XEN 的再进化

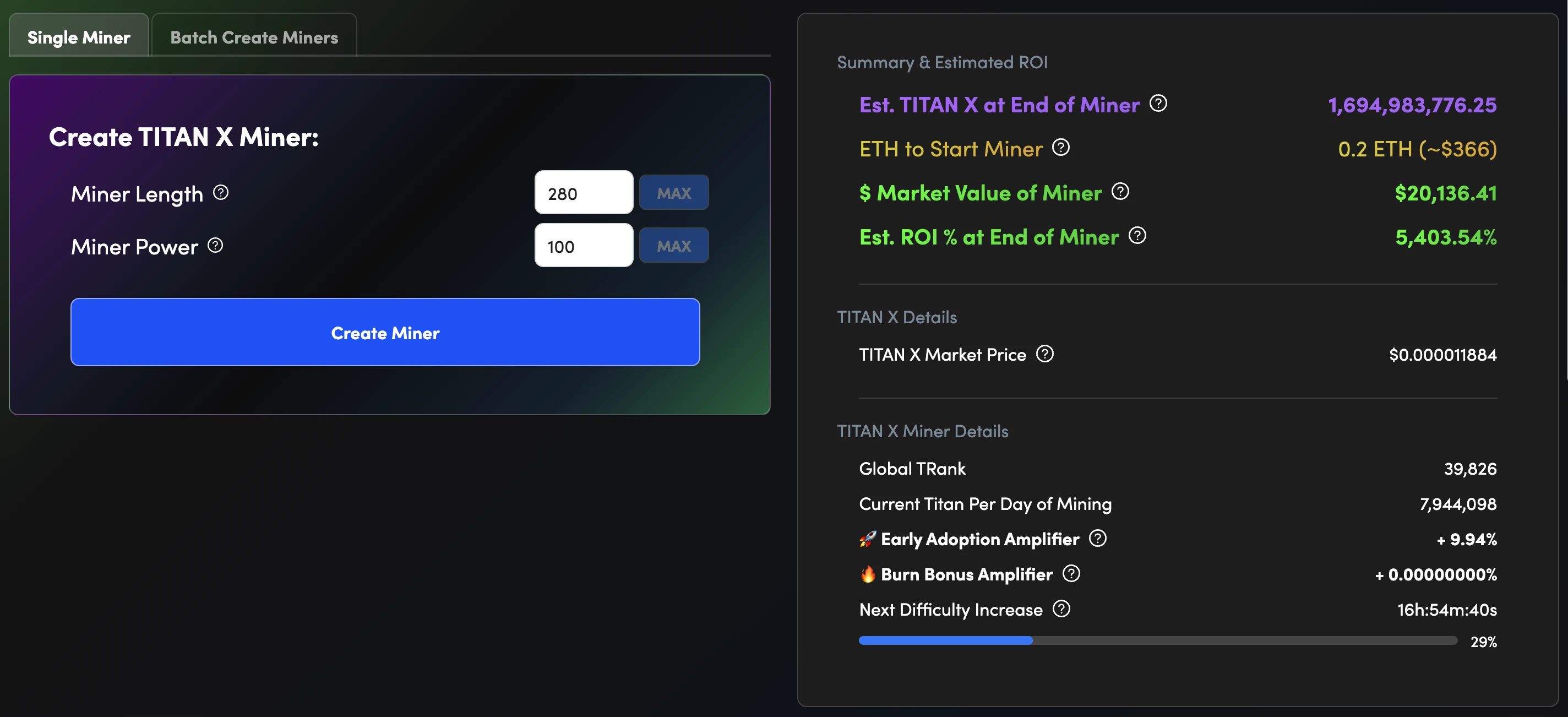

如何理解 TITAN X?概括来说,这一项目的机制非常简洁,几乎和 XEN 一模一样,即消耗 ETH 铸造 TITANX。

官方文档显示,TITAN X 拥有一种名为“虚拟矿机”的机制;借助虚拟矿机,用户可以通过质押 ETH 挖掘 TITANX。

而在代币销毁上,TITAN X 使用了一种名为“Proof of Burn 2.0 ”的销毁机制。生态系统内的开发人员可以使用 TITANX 来启动他们自己的代币,当他们这样做时——TITANX 将被销毁。这一机制类似Odaily星球日报此前曾介绍过的 XEN“套娃”式生态。

而和 XEN 不同的是,TITAN X 设计了将收益留向项目方、并由项目方回购的机制。根据官方文档,仅 28% 的 ETH 被用于奖励给质押 TITANX 代币 的用户,而 62% 的 ETH 都被发送给 TITAN X 合约用于回购和销毁。

安全性隐忧

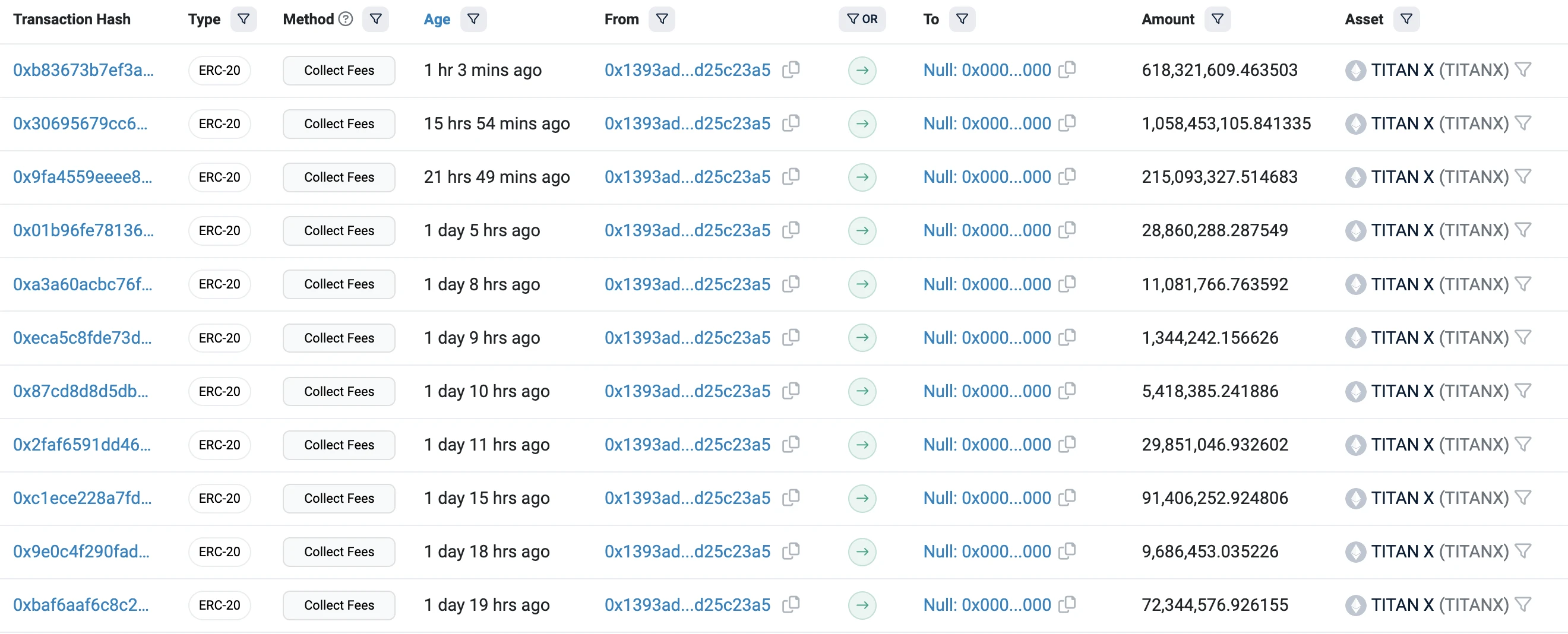

昨日,有社区用户质疑,TITAN X 的回购机制并没有有效运作,并存在合约风险。社区用户对这一项目的担忧在于,TITAN X 的回购合约存在 80 ETH 的回购上限,且并不能按时运作。

Odaily星球日报发现,该项目的回购操作也并非由合约“自动”执行,仍然需要项目方通过其控制的地址人工进行调用操作。以此来出发合约的回购操作。

此外,合约的安全性也缺乏保障。因此,项目方存在作恶的可能。在查询链上项目之后发现,在 TITANX 代币大跌期间,回购曾一度中断超过 7 个小时。

昨日稍晚间,TITANX 创始人 Jake Sharpe 于 X 平台发文表示,可能会直播回购和销毁 TITANX。对于回购限额,他也给出了回应,表示回购机制从一开始就设有限额,以防止滥用并培育健康的市场,几个月后或将取消回购上限。

链上数据显示,在中断 7 个小时后,目前 TITAN X 的回购地址已经恢复了回购销毁的操作,目前地址内有约 4700 枚 ETH。

归零之后,驶向何方?

尽管目前回购销毁已经恢复,但 TITAN X 已经失去了社区的信任。DEXTool 数据显示,TITANX 币价已跌至“归零”,目前其币价较最高点已经跌去约 94% 。

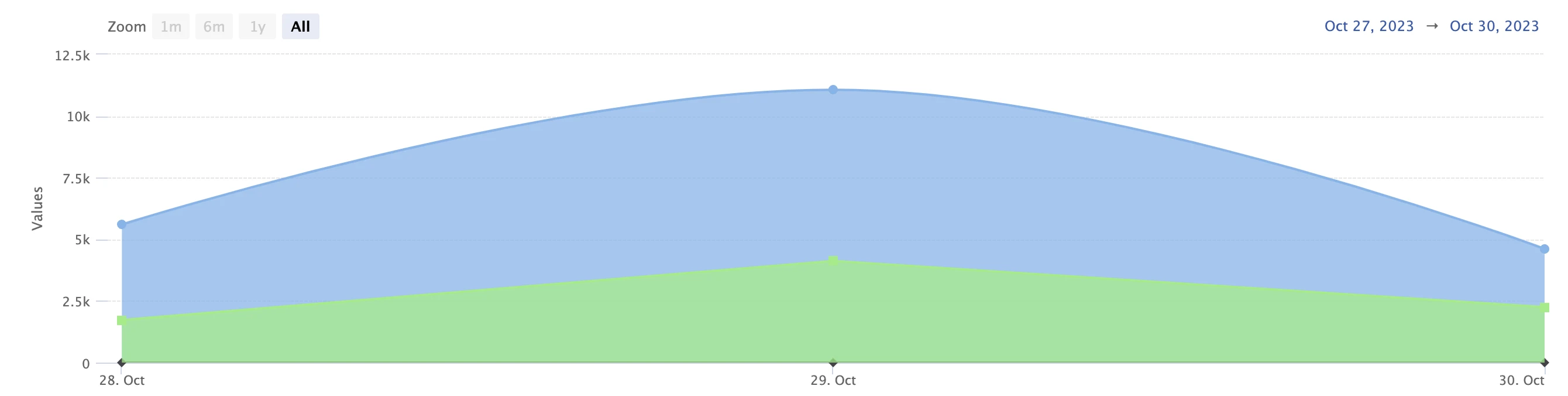

链上数据显示,随着 TITANX 的价格下跌,其链上交易数量也极具下跌。由于这一代币需要靠 mint 来生产,因此这也意味着用户数量的快速下跌。

(TITANX 铸造合约的 Tx 数量)

但代币独立地址数并未显著降低,目前 TITANX 拥有约 2700 个独立地址,最高峰值时也仅为 2804 个独立地址。

链上活跃度的降低,也让 TITAN X 的铸造收益率快速回升。但已经失去社区信任的 TITAN X 的,却有着诸多悬之未觉的隐忧:项目的合约设计,究竟是否安全?项目方是否存在“Rug”的能力?

另外,与 XEN 的盛况和地址数量相比,TITANX 的链上数据仍与 XEN 早期存在着极大的差距。XEN 曾一度“带火”了一个赛道,大量“仿盘”纷纷涌现;而在机制上有所优化的 TITANX,目前来看并不能复刻当初 XEN 的成功。

尽管 TITANX 在“虚拟矿机”的实验中迈出了自己的一步,但目前来看,TITANX 恐怕依然回天乏术。能否重拾社区信心、重新获取热度和流量, 这对 TITANX 来说是一个近乎不可能完成的挑战。