A new study from crypto insights firm Coincub is shedding light on the most accommodating markets in the world for the digital asset industry.

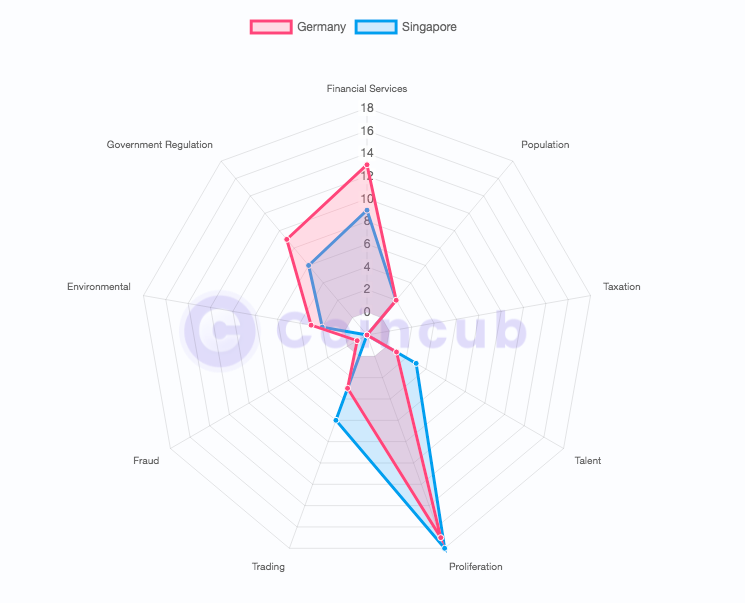

Coincub’s latest report says that Germany has now replaced Singapore as the most crypto-friendly country on earth.

The analytics firm highlights a number of key developments over the past year that have helped Europe’s largest economy to overtake Singapore.

“Germany is already one of the world’s most crypto-friendly countries. The country also has the highest number of Bitcoin nodes besides the US, but with a smaller population and GDP demonstrating an even greater commitment to crypto. There have been several positive developments over the last few months.

The Federal Financial Supervisory Authority issued a crypto custody business license for Coinbase’s German arm earlier this year. German stock market operator Deutsche Boerse has also listed more than 20 crypto exchange-traded products on its digital exchange, Xetra. The Sparkasse savings bank looking into offering wallets to trade crypto is a huge step for institutional acceptance.”

Source: Coincub With Singapore now ranked second, the United States now sits in third, followed by Australia, Switzerland and Hong Kong.

Coincub says that the United Arab Emirates (UAE) has become a new country on the list, appearing at number 22 after previously taking a hard stance against crypto with bans on trading and other activity. India has moved up to number 19, but as Coincub says, suffers from indecisive government policy.