原文标题:How should project founders approach the Korean market?

原文作者:Ash

原文编译:Ismay,BlockBeats

编者按:刚刚落幕的韩国 KBW 会议产生了很多有趣的故事,三箭资本联合创始人 Zhu Su 曾在社交媒体发文表示,「听说区块链会议韩国区块链周(KBW)的门票供不应求,这是看涨信号。」加密 KOL 在本文中从多方面介绍了加密项目如何打入韩国市场,值得收藏。

以下为原文内容:

韩国的加密货币交易所处理了惊人的 20 亿美元交易量,这为项目提供了独特的机会。今年我在 @kbwofficial 会议上有机会与当地利益相关者交流,并总结了一些关键见解,帮助您制定进入策略。

内容分解:

• 韩国生态系统概况

• 规划营销活动

• 了解韩国散户

• 其他

保存这份指南!

韩国生态系统概况

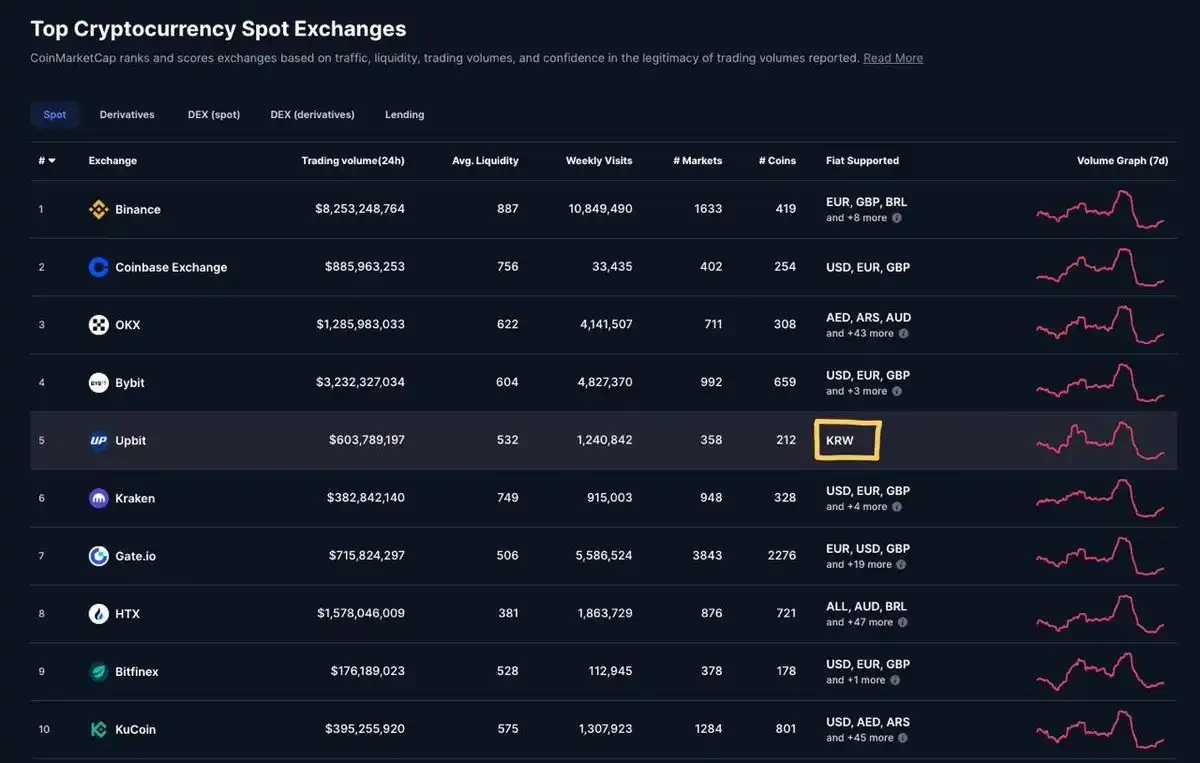

这一部分涵盖了当地的生态系统,包括中心化交易所(CEX)、媒体、研究和咨询、投资、项目以及 KOL。据多个消息来源,约有 10% -15% 的韩国人(600 万-900 万人)使用中心化交易所进行交易!

a) 中心化交易所

韩国有三大中心化交易所(Upbit、BitThumb 和 Coinone),其中 Upbit 和 BitThumb 占据了 95% 的市场份额。

一个有趣的事实是,这些交易所都与银行连接以支持资金的进出:

• UpBit 连接 KBank

• BitThumb 连接 农协银行

• Coinone 连接 KakaoBank

在每个交易所内,韩元(KRW)的交易量最大,因此大多数项目应该努力让自己的代币与韩元进行交易对的上线。

我发现本地中心化交易所交易量之所以如此庞大,原因有:

• 本地赌博文化*以及韩国散户强大的购买力

• 韩国人不喜欢自我托管,因此更愿意在中心化交易所进行交易

• 韩国人将加密货币视为一种投机资产类别(类似于股票),注重的是炒作的叙事而非基本面(例如与大品牌的关联,如 Ondo 与 Blackrock,Doge 与 Elon Musk)

*在与一些人交谈后,我会说这是韩国的阴暗面,当前的经济条件(飙升的房地产市场、低工资、疲软的股市以及垄断性的经济结构)迫使人们通过高风险赌博摆脱贫困,希望一夜暴富。

b) 媒体

语言障碍使韩国用户往往依赖本地出版机构获取最新新闻和动态。除了 @official_naver 的博客,知名的媒体平台还包括:

@eBlockmedia

@CoinnessGL

@bloomingbit_io

@FACTBLOCK

@tokenpostkr

对于非韩国项目,直接与这些媒体公司合作可能具有挑战性,这时下一个利益相关方会派上用场。

c) 研究与咨询

韩国拥有一个蓬勃发展的研究和咨询生态系统,许多公司充当项目与用户之间的桥梁,也在国际项目与韩国受众之间发挥中介作用。

要制定成功的韩国市场进入策略,与一家有信誉的公司合作至关重要。我将这些公司分为两大类:

i. 顾问类

• @Xangle_official

• @DeSpreadTeam

• @0x undefined_

• @INF_CryptoLab

• @Edward__Park

• @EncodingLabs

• @Whitewater_Labs

• @ 071 _labs

ii. 研究类

• @FourPillarsFP

• @Tiger_Research_

明确目标能够帮助创始人更容易选择合适的公司。例如:

• 想要与韩国机构建立联系:

@Xangle_official

• 连接韩国开发者并增加研究曝光率:

@FourPillarsFP

• 针对 Degen 或散户用户:

@DeSpreadTeam

• 紧跟本地法规动态:

@Tiger_Research_

d) 投资

韩国的资本市场规模不大,只有少数几个主要玩家,可以分为两大类:

i. 风投基金

• @hashed_official

• @nonceclassic

• @LECCAVentures

• @blocore_vc

• @ROKCapital

• @SamsungNext

ii. 做市商(MMs)

• @presto_labs

• @alphanonce

• @hyperithm

*请注意,由于监管原因,做市商不能在韩国的中心化交易所开设公司账户。

e) 项目

• DeFi:

@MitosisOrg、@keplrwallet、@Exponents_Fi

• 生态系统:

@KaiaChain、@initiaFDN、@StoryProtocol

• 游戏:

@delabsOfficial、@WemixNetwork、@MaplestoryU

• 验证者:

@dsrvlabs、@a 41 _allforone

*我肯定遗漏了很多项目,请不要怪我。

f) KOL

• @Edward__Park

• @kimyg 002

• @0x ProfessorJo

• @delucinator

营销活动规划

许多项目渴望进入韩国市场,吸引他们的是巨大的交易量和韩国散户投资者的强大购买力。

然而,这种狭隘的思维方式是不尊重韩国参与者的,韩国人并不容易被操纵来提供退出流动性。特别是在 Terra Luna/Anchor 事件之后,韩国的 Degen 投资者更加谨慎且知识渊博。

韩国人非常重视透明的营销和真实的意图。拥有有魅力但谦逊的创始人、能激发信任的项目,往往能够在韩国文化中吸引大量追随者,类似于邪教或宗教在韩国的影响。

在进入韩国市场之前,制定一份全面的营销计划,确保:

• 有明确的关键绩效指标(KPI)

• 包含可执行的用户操作项

• 提供清晰的未来路线图(包括 TGE 前后的计划)

一个简单的营销活动可以这样规划:定义明确的营销目标并为用户设定具体行动→与媒体机构和咨询公司合作进行 SEO 优化,并推出韩文翻译的研究报告→策划 KOL 推广活动以扩大影响力。

在饱和的市场中,大多数传统营销策略已经不足以脱颖而出。韩国投资者对不断出现的任务活动和代币/节点销售日益疲惫。要想脱颖而出,必须具备创意,提供真正的价值,例如有吸引力的激励措施或财务收益机会。

了解韩国散户

众所周知,韩国人是潮流引领者和追随最新热点的狂热者,这从他们活跃的时尚圈、对奢侈品牌的痴迷以及对 K-Pop 的忠诚便可见一斑。这意味着项目必须不断更新其营销材料,并呈现创新且吸引人的叙事,以维持散户投资者的兴趣。

韩国用户可以分为以下三类:

• 撸空投用户:需要可执行的步骤

• 机会主义的挑选者/交易员:追随叙事和热点

• 基础设施用户(技术至上):非常少见,因为韩国人更信任第三方解决方案

使用一刀切的方法注定失败,定制化的营销活动对目标受众至关重要。通过透明和公开的沟通来建立信任,同时使用韩语,是在韩国市场取得成功的关键。

其他

a) 韩国的大型消费应用

• Naver

• Coupang(电商)

• Kakao(KakaoTalk, Kakao Taxi)

• Samsung Pay(显而易见的原因,Apple Pay 在韩国不适用)

b) 韩国的开发者主要来自 SKY 或 KAIST

SKY 是韩国三所最负盛名大学的非正式缩写:

• 首尔大学

• 高丽大学

• 延世大学

而 KAIST(韩国科学技术院)是一所国立研究型大学。

c) 我学到的其他有趣的事

• Aptos 和 Sui 在韩国非常受欢迎。

• 许多生态系统已经开始招聘韩国负责人,包括 Monad、Chromia 等。

• 没有遇到任何来自 Upbit 或 BitThumb 的人,这些交易所的上市非常困难且随机。

• 街上有很多电子烟店。

• 下次去韩国旅行时:使用 Naver Map 和 KakaoMap 导航;Uber 和 Kakao Taxi 出行;Catch Table 寻找餐厅;Coupang Eats 点餐外卖,Papago 进行翻译。

好了,啰嗦够了。

总结:绘制本地生态系统和市场概况→与本地咨询公司合作→制定本地化的营销活动→了解韩国散户→不要仅仅因为韩国交易量大就去利用它。

本文由非韩国人撰写,如有遗漏或错误,欢迎在评论区指正!