原创 | Odaily星球日报(@OdailyChina)

作者|Golem(@web3_golem)

今日早上 8 点,备受瞩目的 Fractal 主网终于上线。Fractal 采用了一种名叫“Cadence Mining”独特的挖矿机制,即每开采 3 个区块,其中两个区块将被免许可挖矿,另一个区块将被合并挖矿。这样的机制催生出许多 Fractal 生态挖矿项目,同时也激发了用户租赁算力参与挖头矿的激情。

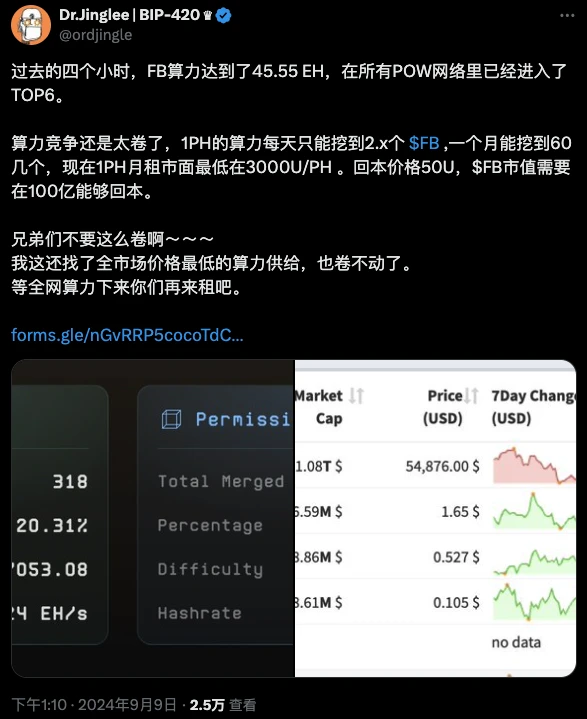

因此,由于利益相关,主网挖矿产出和 FB 价格成为社区关注焦点。虽然 FB 场外价格已经上涨到 19 u 左右,但许多社区成员依表示可能租赁算力参与头矿可能血本无归。

事实果真如此吗,普通用户参与 Fractal 头矿究竟是“吃肉”还是“割肉”的前奏,Odaily星球日报将在本文中简要分析 Fractal 挖矿产出与收益,希望能为读者提供参考。

挖矿成本收益估算

根据 Fractal 区块浏览器的数据显示,目前 Fractal 合并挖矿算力约为 90 EH/s,免许可挖矿算力为 10000 PH/s(1 EH/s= 1000 PH/s)。

已知目前市面上每月 1 PH/s 算力的租赁价格在 3000-5000 USDT 之间。即使按最低的租赁成本计算,以 FB 19 USDT 的价格计算,每日产量达到 5.26 枚 FB 就实现了盈亏平衡。

社区中较为广泛的挖矿产出计算方式如下:

按 30 秒的平均出块时间和三分之二产量被免许可开采来计算,每日大约产出 7.2 万枚 FB,其中免许可挖矿获得 FB 约为 4.8 万枚。因此 1 PH/s 的算力每天大约能获得 4.8 枚 FB,按照 FB 场外价格 19 USDT 计算,矿工每日收入约为 91.2 USDT。

如果以这种计算方式来估计,租赁算力开采 FB 头矿不仅不会赚钱,而且随着全网免许可挖矿算力的增加,每 1 PH/s 被分配到的 FB 奖励持续减少,亏损还将会扩大。

相对动态的计算方式:

以上的计算方式基本是基于算力持续增加和每日产量不变的情况,但事实是,虽然 Fractal 官方预设的平均出块时间为 30 秒,每日产出大约为 7.2 万枚 FB,不过目前网络平均出块速度已经明显快于预期。

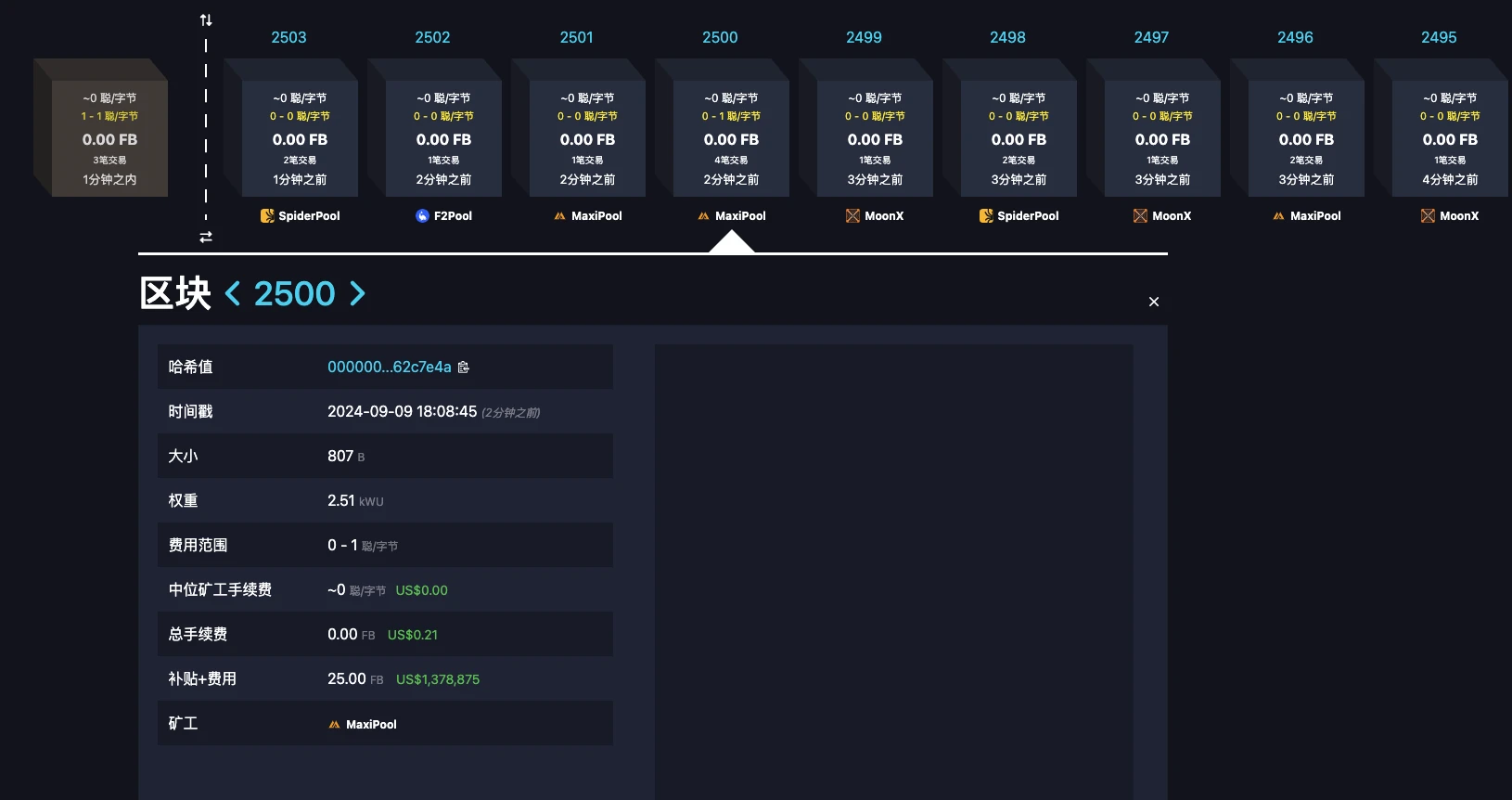

如下图,Fractal 主网启动 10 小时就开采出了 2500 个区块,产出了超 6.25 万枚 FB,这也就是说实际上随着算力的增加,区块的开采速度也在加快。每日真正的产量将会超过此前估计的 7.2 万枚。

因此,Fractal 主网在头矿期间真正的出块平均时间约为 10 ~ 15 秒,也就是说 FB 今日产出可能会在 14 到 21 万枚之间。即使按最保守 14 万枚 FB 产出估计,其中三分之二被免许可开采,即 9.3 万枚 FB, 1 PH/s 的算力今日大约能获得 10.3 枚 FB。按照 FB 场外价格 19 USDT 计算,矿工每日收入约为 195.7 USDT。

如果以这种计算方式来估计,只要 FB 价格坚挺在 10 USDT 以上,租赁算力开采 FB 头矿的玩家依然是可以盈利的。

不过,这样的计算方式也只是相对动态而已,全网算力情况、每日产出和 FB 价格等变化都会影响到挖矿产出与收益,最终 Fractal 挖矿是否值得长期参与还需要等网络运行稳定后再重新进行评估。

Fractal 仍然充满挑战

围绕今日 Fractal 主网上线,除了在挖矿收益上受到广泛讨论外,关于其网络仍然存在着一些质疑。

mempool 创始人就在 X 平台发文表示,Fractal Bitcoin 似乎是 Bitcoin Core v2 4.0.1 的“克隆”副本,其预挖(premine)代币占 Fractal Bitcoin 完全稀释供应的 50% ,矿工们将需要整整两年(一个 Fractal Bitcoin 减半区间)才能赚取创始人们首日获得奖励的一半。同时Fractal Bitcoin 有许多只存在白皮书中的无意义技术用语,因此在他看来,其只是(比特币的)又一个垃圾分叉(shitfork)。

在网络运行上也出现了节点问题和长时间不出块的问题,不过团队的问题响应速度也较快,及时修复了节点行为并很快提供了新的节点版本。

同时,根据场外 19 USDT 的价格,目前 FB 的市值已经接近 40 亿美元。虽然 FB 已经可以通过 Fractal 主网进行转移,但目前并没有任何 DEC/CEX 上线 FB 代币,用户的交易行为依然依靠场外 OTC,交易效率较低及不透明性也给 FB 未来的价格走势“蒙上一层不确定”。