Bank of Japan officials are increasingly focusing on the potential impact of the weak yen on inflation, a trend that could substantially disrupt the future path of interest rate hikes. According to sources familiar with the matter who spoke to Bloomberg, although the Bank of Japan may keep interest rates unchanged at the upcoming policy meeting, exchange rate factors may prompt it to reassess the timing of rate hikes, and could even force it to act earlier than planned.

As reported by Bloomberg, Bank of Japan officials believe that the influence of the weak yen on prices is strengthening, particularly as companies are increasingly inclined to pass rising input costs on to consumers, which could further intensify inflationary pressures. Although the Bank of Japan just raised its benchmark interest rate last month and has not set a predetermined path for borrowing costs, if the yen continues to weaken, policymakers may consider moving forward with rate hikes that were originally expected to occur later.

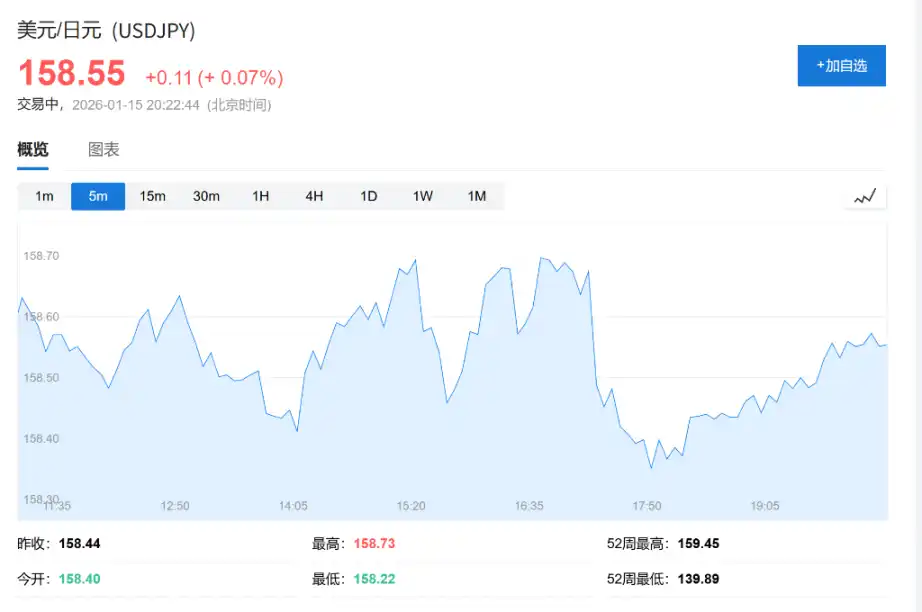

Currently, the general expectation among private economists is that the Bank of Japan will raise rates at a pace of about once every six months, meaning the next move could occur this summer. However, sources told Bloomberg that officials prefer to execute policy adjustments in a timely manner rather than being excessively cautious, suggesting that the previously market-expected pace of hikes is now facing uncertainty. Affected by this news, the yen briefly fell to around 158.68 against the U.S. dollar before rebounding to 158.33. As of the time of writing, the yen has fallen to 158.55 against the dollar.

January Meeting Expectations: Rates to Remain Unchanged

The Bank of Japan will announce its latest policy decision on January 23. Sources told media that officials currently view maintaining the interest rate at 0.75% as appropriate, a level that has reached a three-decade high. Although the overall inclination is to hold steady, the committee will continue to monitor economic data and financial market developments up to the last moment to make a final decision.

The focus of this meeting will be on how the central bank assesses the impact of the yen on potential inflation. Sources told Bloomberg that, given that inflation trends are already close to the bank's 2% target, officials will closely watch how exchange rate fluctuations alter the price expectations of households and businesses.

Exchange Rate Transmission Mechanism Under Scrutiny

Yen depreciation typically increases inflationary pressures by raising import costs, while also boosting exporters' profits. However, some officials point out that as the yen remains weak, its negative impact on the economy may be increasing. Officials believe the Bank of Japan still has room to continue raising rates, with the key being to time the policy adjustments correctly.

The Japanese business community is also speaking out more frequently on the exchange rate issue. Yoshinobu Tsutsui, head of Keidanren (Japan Business Federation), the country's largest business lobby group, made rare comments this week calling for government currency measures to prevent excessive yen depreciation, describing recent yen movements as "a bit too much."

Market Background and Political Factors

Although the Bank of Japan raised its benchmark interest rate on December 19, the yen remained weak against the U.S. dollar. The yen slid further to a new 18-month low this week, affected by news that Prime Minister Takaichi Sanae will call a snap election next month.

Data compiled by Bloomberg shows that the 10-year average exchange rate for the yen against the U.S. dollar is 123.20, while over the past two-plus years, the yen has generally fluctuated between 140 and 161.95. Although it rebounded slightly after hitting an 18-month low earlier this week as monetary authorities stepped up warnings, the overall depreciation trend continues to put persistent pressure on the central bank's decision-making.