$135 per share, 555.6 million shares, $1.77 trillion.

SpaceX has pinned its IPO price here. According to the S-1/A filed with the SEC on June 3 and the FWP roadshow materials filed on June 4, the company plans to issue 555.6 million shares of Class A common stock at an offering price of $135 per share. The stock is expected to list on Nasdaq and Nasdaq Texas under the ticker symbol SPCX. After deducting underwriting discounts and offering expenses, the company expects net proceeds of approximately $74.4 billion, or about $85.7 billion if the underwriters fully exercise their additional purchase option.

The real question posed to the market by the roadshow is not "How much should a rocket company be worth?" What SpaceX repeatedly emphasizes in its materials is something else: space transportation, satellite connectivity, and AI computing power are being consolidated into a single balance sheet.

According to the same FWP roadshow materials, SpaceX claims to be the only company simultaneously building the three-layer hardware and software infrastructure for space, connectivity, and AI. The Space business is responsible for lowering the cost of reaching orbit, Starlink is responsible for extending connectivity on land, at sea, in the air, and beyond mobile networks, and the AI business integrates xAI, Grok, X, and the Colossus computing cluster into the same narrative.

The figures it provides are substantial enough. According to the roadshow materials, SpaceX has carried over 80% of global mass to orbit since 2023, with approximately 650 cumulative launches, operates over 9,600 Starlink satellites, has about 10.3 million Starlink users, and covers 164 countries and regions. Grok and X have approximately 550 million monthly active users, X sees about 350 million daily posts, and the nominal power consumption of its AI computing infrastructure exceeds 1GW.

This is precisely where the greatest divergence lies on Wall Street today.

SpaceX says it's selling infrastructure. Skeptics say it's packaging infrastructure, AI, and Musk's personal premium together for sale.

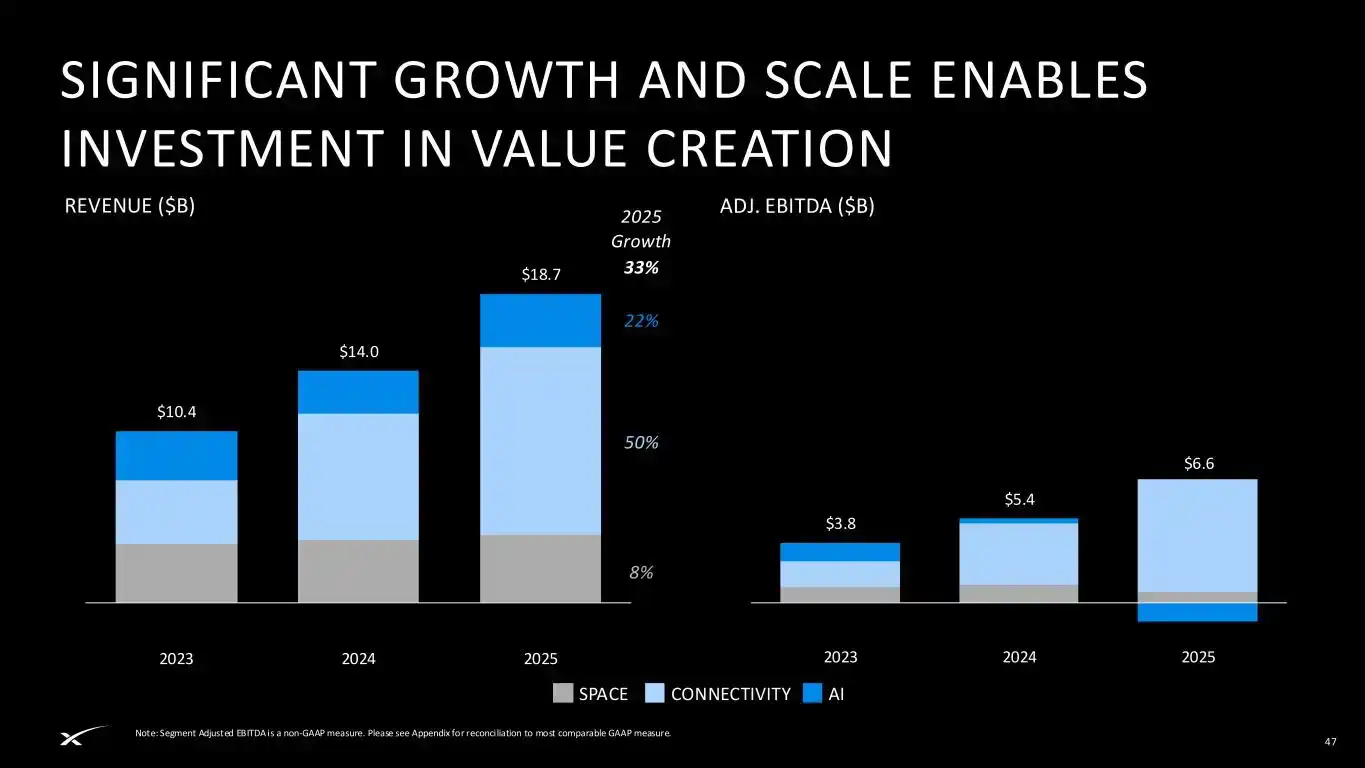

First, look at the hardest piece in the roadshow. Connectivity is currently the part that most resembles a 'public company business.' According to the roadshow materials, the Connectivity segment generated $11.4 billion in revenue and $7.2 billion in adjusted EBITDA in 2025, up from $7.6 billion in revenue and $3.8 billion in adjusted EBITDA in 2024. The Space segment reported $4.1 billion in revenue and $0.7 billion in adjusted EBITDA in 2025. The AI segment reported $3.2 billion in revenue and an adjusted EBITDA loss of $1.2 billion in 2025.

Combined, these three bills present a highly uneven SpaceX. Starlink is profitable, rockets provide deployment capability, and AI is burning cash while contributing valuation optionality.

According to the roadshow materials, SpaceX's total revenue for 2025 was $18.7 billion with adjusted EBITDA of $6.6 billion, but it recorded a GAAP net loss of $4.9 billion. Capital expenditures rose from $4.4 billion in 2023 to $11.2 billion in 2024, and further to $20.7 billion in 2025. For the first quarter of 2026, the company still recorded a GAAP net loss of $4.3 billion.

Translated into stock market language, this is not a mature earnings stock. It's a stock selling the future control of infrastructure to the public market ahead of time.

Wall Street's initial set of reactions is to acknowledge that the story has changed.

In an article by fund manager Mike Alves, he stated that investors should not just look at the headline valuation of $1.75 to $2 trillion; the real question is whether SpaceX is building the infrastructure layer for the next generation of the economy. Shaun Davies, Associate Professor of Finance at the University of Colorado Boulder, also described SpaceX as a hybrid of aerospace, communication infrastructure, defense technology, and AI. Scott Pace, Director of the Space Policy Institute at George Washington University, offered a judgment closer to the roadshow's pitch, suggesting that growth drivers come from communications, data, and AI combining through space in new ways.

This is the core logic of one bullish camp. Don't try to fit SpaceX into the mold of Boeing, AT&T, or traditional aerospace companies. It's selling access to a difficult-to-replicate infrastructure platform.

Reuters noted that at least one large institutional investor in SpaceX privately is not comparing it to Boeing or AT&T, but rather to companies like Palantir, GE Vernova, Vertiv—firms that have been revalued by AI infrastructure. PitchBook analyst Franco Granda's statement in the same report was blunt: investors today are paying a platform premium, betting on tomorrow's monopoly economy of infrastructure.

But this valuation framework has its own awkwardness. At a $1.75 trillion valuation, SpaceX would trade at roughly 110 times its estimated 2025 revenue, making even Palantir appear cheaper on some metrics. Calculations based on S&P Capital IQ data show that if using the $1.75 to $2 trillion market cap range and revenue for the trailing twelve months ended March 31, 2026, SpaceX's price-to-sales ratio would be about 90x to 103x, exceeding all of the 'Magnificent Seven' companies and significantly higher than Tesla's roughly 16x P/S ratio at the time.

Bulls can accept this price because they don't see SpaceX as a rocket company. Bears cannot accept this price precisely because SpaceX is no longer just a rocket company.

Valuation divergence becomes clear from here.

The first line is $780 billion. Morningstar analyst Nicolas Owens, initiating coverage on SpaceX, assigned a fair value estimate of $780 billion, less than half the IPO's target valuation. Owens' concerns center on the AI business, noting that Grok is currently not a leading AI lab, technologies like orbital data centers are unproven, and investors might find a more risk-adjusted entry point post-IPO.

The second line is $1.22 trillion to $1.29 trillion. A valuation model by New York University Stern School of Business professor Aswath Damodaran, based on the limited financial data available at the time, gave a baseline valuation of $1.22 trillion, with a median of $1.29 trillion after 10,000 simulations. He acknowledges SpaceX is an engineering marvel and has tremendous competitive advantages, but his bottom line is clear: at a pricing of $1.75 trillion or even $2 trillion, buyers have very little upside potential.

The third line is $1.25 trillion. Baillie Gifford-managed Scottish Mortgage Investment Trust valued its SpaceX holding at $1.25 trillion as of March 31, 2026, emphasizing the valuation is based on verifiable transactions, not media speculation. This number is interesting. Scottish Mortgage is a long-term holder; it's not bearish on SpaceX, but it also hasn't directly marked it up to $1.75 trillion.

Beyond that lies the $1.77 trillion that SpaceX itself is presenting to the public market.

These four numbers placed together represent the real SpaceX on Wall Street today.

It's not a simple case of some shouting 'buy' while others shout 'sell.' It's more like a price band: $780 billion is the conservative anchor set by fundamentals-focused analysts, $1.22 to $1.29 trillion is Damodaran's compromise between narrative and discounted cash flow, $1.25 trillion is the marking by existing institutional holders, and $1.77 trillion is the price SpaceX is preparing for the public market to accept.

Trading sentiment on social platforms is more direct. On X, accounts like Ticker Wire, Surmount, and VirtualBacon, focused on trading, discuss not discounted cash flow, but the $75 billion fundraising, $1.75 trillion valuation, potential index buying pressure, and the trading rhythm where SpaceX's IPO could be followed by potential listings from OpenAI and Anthropic. They treat SpaceX as a liquidity event, not a company that needs to be slowly dissected in Excel.

This is also the warning given by Scott Sacknoff. SPADE Defense Index manager Scott Sacknoff believes the SpaceX IPO has pushed mainstream investor enthusiasm to near irrational exuberance levels, with publicly traded space company stocks already up 60% to 100% year-to-date. At a $1.75 trillion valuation, those likely to make real money may be traders, not buy-and-hold long-term investors.

Traders look at supply and demand; long-term investors look at the path to valuation realization.

There are three checkpoints on this path.

The first checkpoint is Starlink. It must continue to convert user growth, ARPU, mobile connectivity, and enterprise/government customers into cash flow. SpaceX's roadshow places Connectivity within a $1.6 trillion total addressable market (TAM), with Starlink Broadband representing $870 billion and Starlink Mobile representing $740 billion. This market is not small, but the public market will first scrutinize revenue quality, not TAM.

The second checkpoint is AI. SpaceX's roadshow writes the long-term AI opportunity at $26.5 trillion and proposes a roadmap to begin deploying AI computing satellites starting in 2028. Reuters Breakingviews on April 24 called this market proclamation "planetary-grade absurdity," with a simple reason: a $28.5 trillion total addressable market already exceeds one-fifth of global GDP. This isn't to say AI lacks value, but that SpaceX has anchored its valuation optionality on the hardest-to-validate piece.

The third checkpoint is the governance discount. According to SpaceX's S-1/A, based on the post-offering ownership structure, Elon Musk will control approximately 82.4% of the voting power of common stock. Class B common stock carries 10 votes per share, Class A carries 1 vote per share. In an open letter dated May 13, the New York City Comptroller, New York State Comptroller, and CalPERS CEO, representing combined assets under management exceeding $1 trillion, called on SpaceX to adopt one-share-one-vote or impose a sunset clause of no more than 7 years on supervoting rights.

Kiplinger's Mike Alves offered a bullish interpretation of this issue. He argues that in an ordinary company, such control might be a deal-breaker, but SpaceX's market might consider 'getting exposure' more important than governance. The implication here is that investors are not buying governance rights, but an option on Musk continuing to steer the ship.

This roadshow has rewritten SpaceX from a rocket company into an infrastructure conglomerate. What Wall Street must now do is decide how much of this conglomerate consists of real cash flows, how much is future technology roadmaps, and how much is the Musk premium.

If you only look at the roadshow, SpaceX has told an exceptionally complete story. Rockets drive down costs, Starlink connects users, AI brings in computing demand, and orbital computing further raises the ceiling.

If you look at Wall Street's reactions, another story is also complete.

Morningstar is waiting for a lower price, Damodaran is waiting for a major pullback, Scottish Mortgage hasn't marked its holding up to the IPO target price, PitchBook and some institutions are willing to rationalize the platform premium, trading accounts are watching for potential index buying and short-term liquidity, and the pension system is watching control.

SpaceX's rockets are not in dispute. The dispute lies in how much investors are willing to pay for the entire sky that lies beyond those rockets.