Original Author: Long Yue

Original Source: Wall Street News

As the Bank of Japan's monetary policy meeting on December 19 approaches, market concerns about a potential hawkish interest rate hike are intensifying. Could this move mark the end of the era of cheap yen and trigger a global liquidity crisis? A recent strategy report released by Western Securities on December 16 provides an in-depth analysis.

High Inflation Makes Hawkish Rate Hike by Japan Inevitable

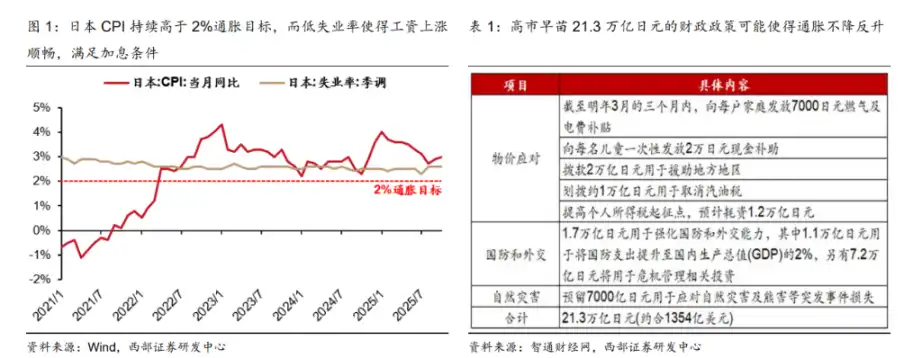

The report points out that multiple factors are behind the BOJ's potential rate hike. Firstly, Japan's CPI has consistently remained above the official 2% inflation target. Secondly, the unemployment rate has long stayed below 3%, creating favorable conditions for nominal wage growth. Market expectations for significant wage increases in next year's "Shunto" (spring labor negotiations) are high, which will further increase inflationary pressures. Finally, the 21.3 trillion yen fiscal policy introduced by Takayuki Kobayashi could also exacerbate inflation.

These factors collectively force the Bank of Japan to adopt a more hawkish stance. The market worries that once the rate hike is implemented, it could lead to the concentrated unwinding of the massive "carry trade" positions accumulated during Japan's YCC (Yield Curve Control) era, thereby causing a liquidity shock to global financial markets.

Theoretical Analysis: Why the Most Dangerous Phase of Liquidity Shock Might Be Over

Despite market anxieties, the report analyzes that, theoretically, the current impact of a Japanese rate hike on global liquidity is limited.

The report lists four reasons:

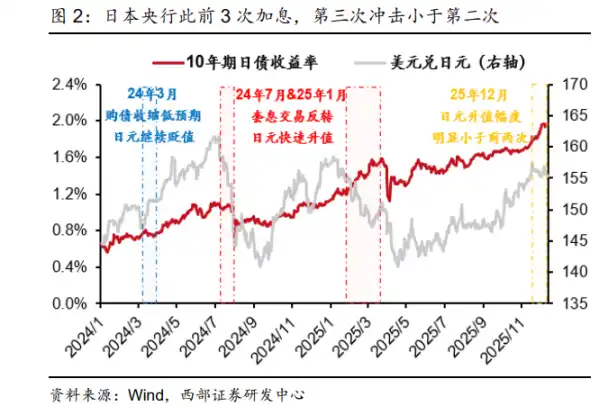

Risk Partially Released: The Bank of Japan has already implemented 3 rate hikes since March last year. Among these, the hike in July last year, coupled with the exit from YCC, did cause a significant liquidity shock, but the impact from the January hike this year has noticeably weakened, indicating increasing market adaptation.

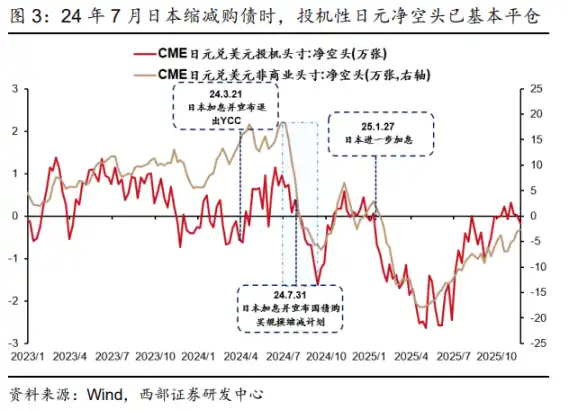

Speculative Positions Already Exited: Data from the futures market shows that most speculative yen short positions were unwound in July last year. This means the most active "carry trades" most likely to cause chain reactions have receded, and the most dangerous phase of the liquidity shock has passed.

Different Macro Environment: The current U.S. is not experiencing a "recession trade" similar to July last year, dollar depreciation pressure is not significant, and the yen itself remains weak due to geopolitical and debt issues. This weakens expectations for yen appreciation, thereby reducing the urgency to unwind "carry trades".

The Fed's "Safety Cushion": The report specifically mentions that the Federal Reserve has begun to pay attention to potential liquidity risks and has initiated balance sheet expansion (quasi-QE) policies, which can effectively stabilize market liquidity expectations and provide a buffer for the global financial system.

Actual Risk: A "Catalyst" in a Fragile Market

The report emphasizes that theoretical safety does not mean one can rest easy. The current fragility of global markets is the real root cause of the potential shock triggered by a Japanese rate hike. The report describes it as a "catalyst".

The report analyzes that the reason the July rate hike last year had such a large impact was the resonance of two major factors: "massive unwinding of active carry trades" and the "U.S. recession trade". Currently, the former condition has weakened. However, new risks are emerging: Global stock markets, represented by U.S. stocks, have experienced a 6-year "big water bull" market (prolonged bull market fueled by liquidity), accumulating substantial profits and inherent fragility. Simultaneously, concerns about an "AI bubble" are resurfacing in the U.S. market, leading to strong risk-off sentiment among investors.

In this context, the certainty of a Japanese rate hike could likely become a trigger, sparking panic selling and inducing a global liquidity shock. However, the report also offers a relatively optimistic judgment: such a liquidity shock would most likely force the Federal Reserve to introduce stronger easing policies (QE), so global stock markets, after a brief sharp decline, are very likely to recover quickly.

Watch and Wait, Monitor the Signal of "Stocks, Bonds, Forex Triple Kill"

Faced with this complex situation, the report advises investors to "watch and wait".

The report believes that since the Bank of Japan's decision is basically an "open secret," but capital flows are unpredictable, the best strategy is to observe.

Scenario One: If capital does not exhibit panic flight, the actual impact of the Japanese rate hike will be very limited, and investors need not take action.

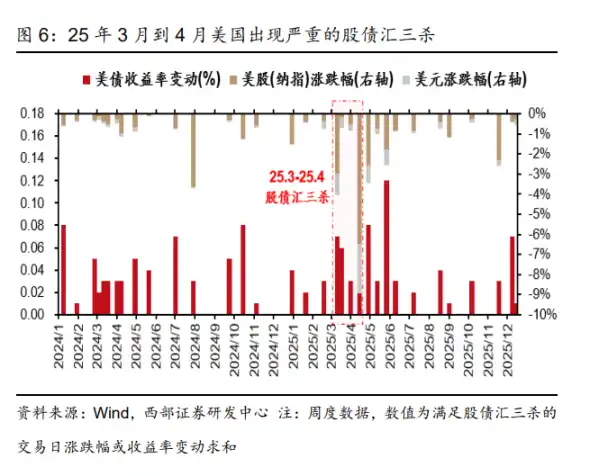

Scenario Two: If capital panic does trigger a global liquidity shock, investors need to closely monitor a key signal—whether the U.S. market experiences 2-3 consecutive instances of a "stocks, bonds, forex triple kill" (simultaneous decline in stock, bond, and foreign exchange markets). The report points out that if a situation similar to early April this year repeats, it indicates a significantly increased probability of a liquidity shock.

Finally, the report believes that even if a Japanese rate hike causes short-term turbulence, it will not change the broader long-term trend of global monetary easing. In this context, it continues to be bullish on the strategic allocation value of gold. Meanwhile, as China's export surplus expands and the Federal Reserve restarts interest rate cuts, the RMB exchange rate is expected to return to a medium-to-long-term appreciation trend, accelerating cross-border capital inflows, which is positive for Chinese assets. The report is optimistic about AH shares experiencing a "Davis Double Click" of earnings and valuation. For U.S. stocks and bonds, the report holds a震荡 (volatile/oscillating) view.