Compiled by: Zhou, ChainCatcher

Introduction

As the convergence of crypto and AI accelerates, Coinbase will no longer be just a crypto exchange; it is evolving into the settlement layer, distribution layer, and commercial layer of AI-native finance.

Most people still view Coinbase as a cyclical crypto brokerage, believing its performance is tightly linked to crypto trading volumes.

This is understandable, as Coinbase's valuation multiples are closely correlated with traditional brokers like IBKR, Robinhood, and Schwab. In contrast, Circle, as a pure-play bet on stablecoin growth, commands a high NTM P/E ratio of 103.9x.

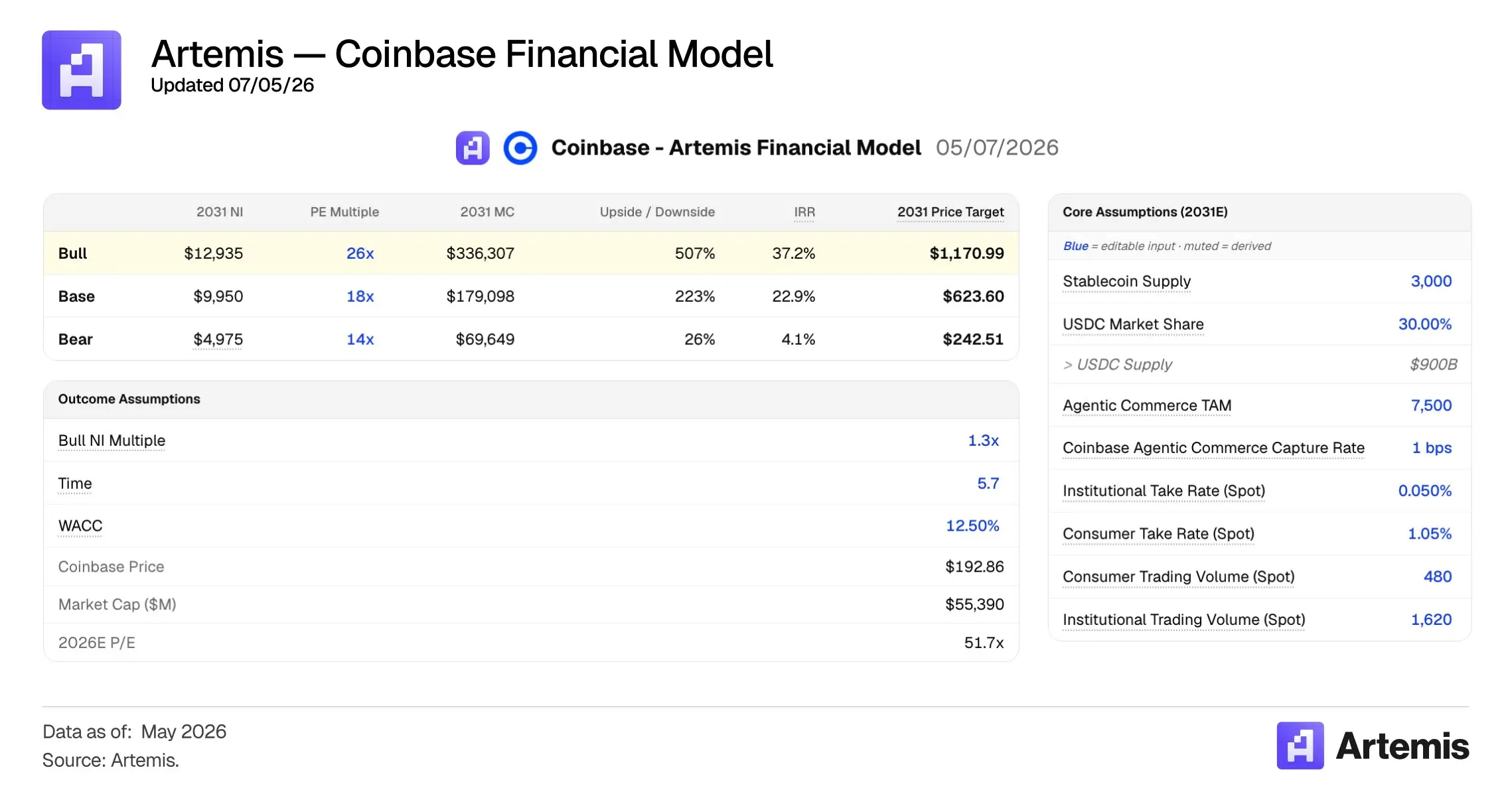

However, Coinbase has a full opportunity to grow into a $300 billion company by 2031 (approximately 6x from current levels, corresponding to a 35% annualized growth rate). The driving force is not just its exchange business, but its position as the top winner in the stablecoin and agent-based commerce fields.

Our core assumptions are as follows:

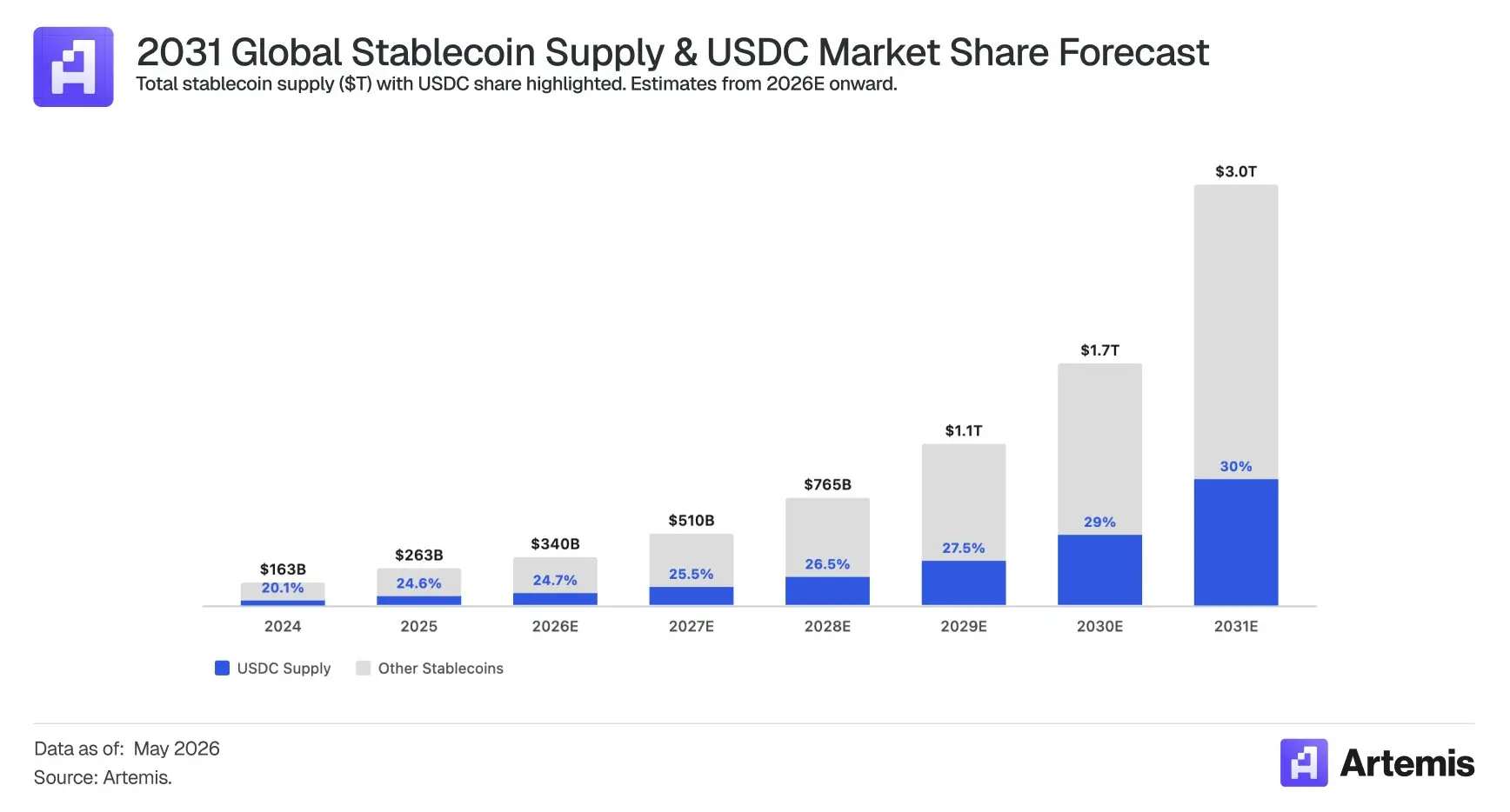

● Stablecoin supply reaches $3 trillion by 2031

● Agent-based commerce volume reaches $7.5 trillion by 2031

● Core exchange business aligns with market consensus: trading revenue of approximately $6 billion by 2028

What the market overlooks is that Coinbase is simultaneously benefiting from two epochal tailwinds:

1. The Rise of Stablecoins and Global Demand for a Digital Dollar

US Treasury Secretary Scott Bessent predicts stablecoin supply will reach $3 trillion by 2030 (a 10x increase from current levels). Bain & Company estimates the supply will expand 12x, reaching approximately $3.8 trillion by then.

2. The Rise of Agent-Based Commerce

McKinsey predicts global agent-based commerce will reach $3 to $5 trillion by 2030; we further predict that one-third of this volume will be completed on-chain and settled via agent-based payment protocols like x402 and MPP. We are already observing rapid growth of agent-based payments on-chain.

Coinbase is a clear beneficiary of both trends, continuously accumulating value through its position as the largest and most compliant distributor of USDC and the top network in agent-based payments.

Even if institutional investors are skeptical of DeFi or believe the crypto market is "dead," Coinbase's success will not rely on crypto asset or exchange trading volumes, but on its role as the most trusted, dominant stablecoin platform and AI agent payment infrastructure.

Why Coinbase is the Winner in the Stablecoin Race

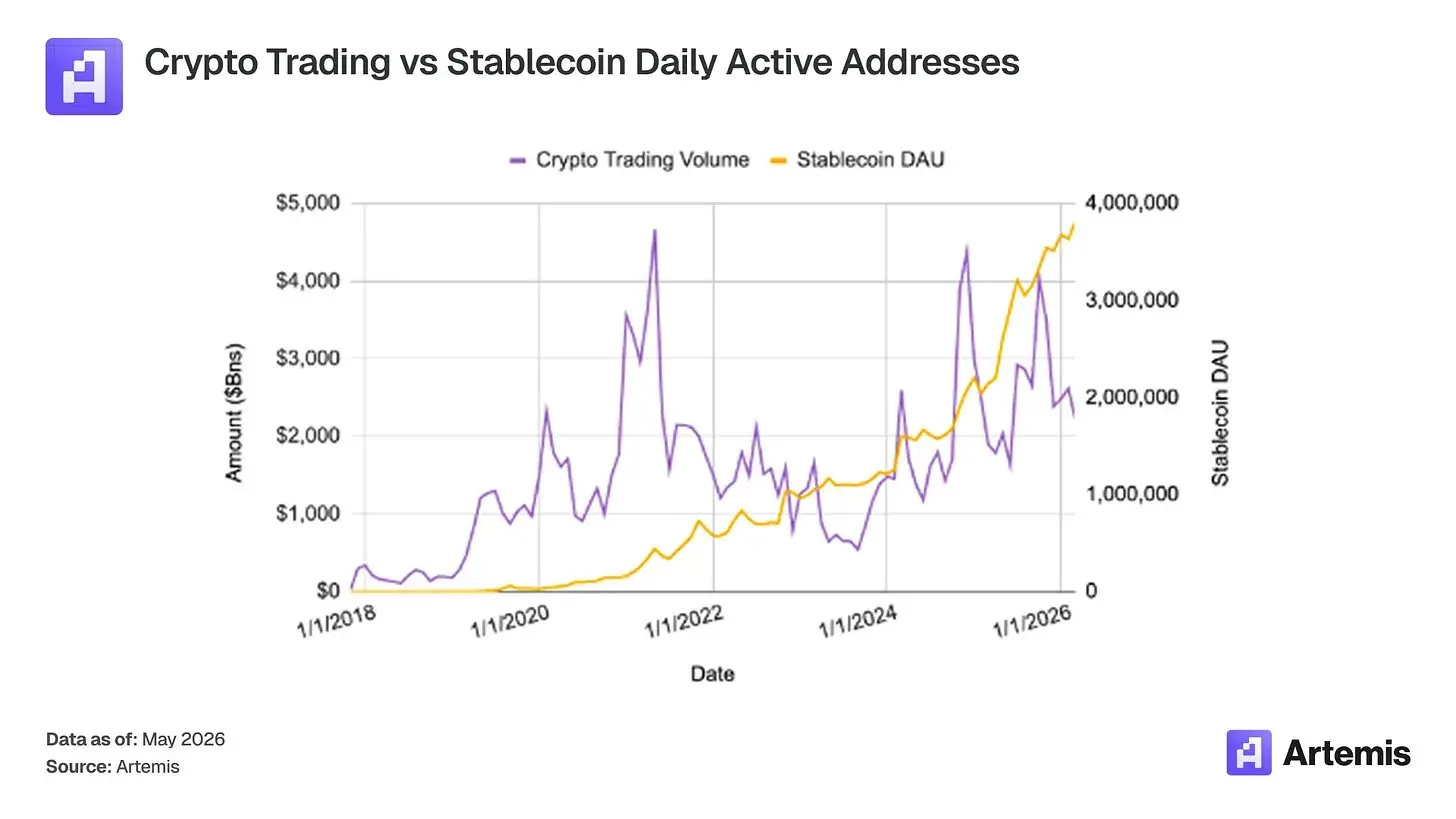

The market fails to realize that Coinbase is a clear winner from stablecoin growth. Even as crypto trading volumes decline, stablecoin usage has historically continued to rise.

The USDC distribution agreement is an asset of Coinbase, not Circle's. The revenue share Circle pays to Coinbase has risen from 32% in 2022 to about 50% in recent years.

The structural reason is straightforward: USDC held within Coinbase products can earn approximately 100% of the interest income, and it receives a substantial share of off-platform balances under the Payment Base waterfall distribution mechanism.

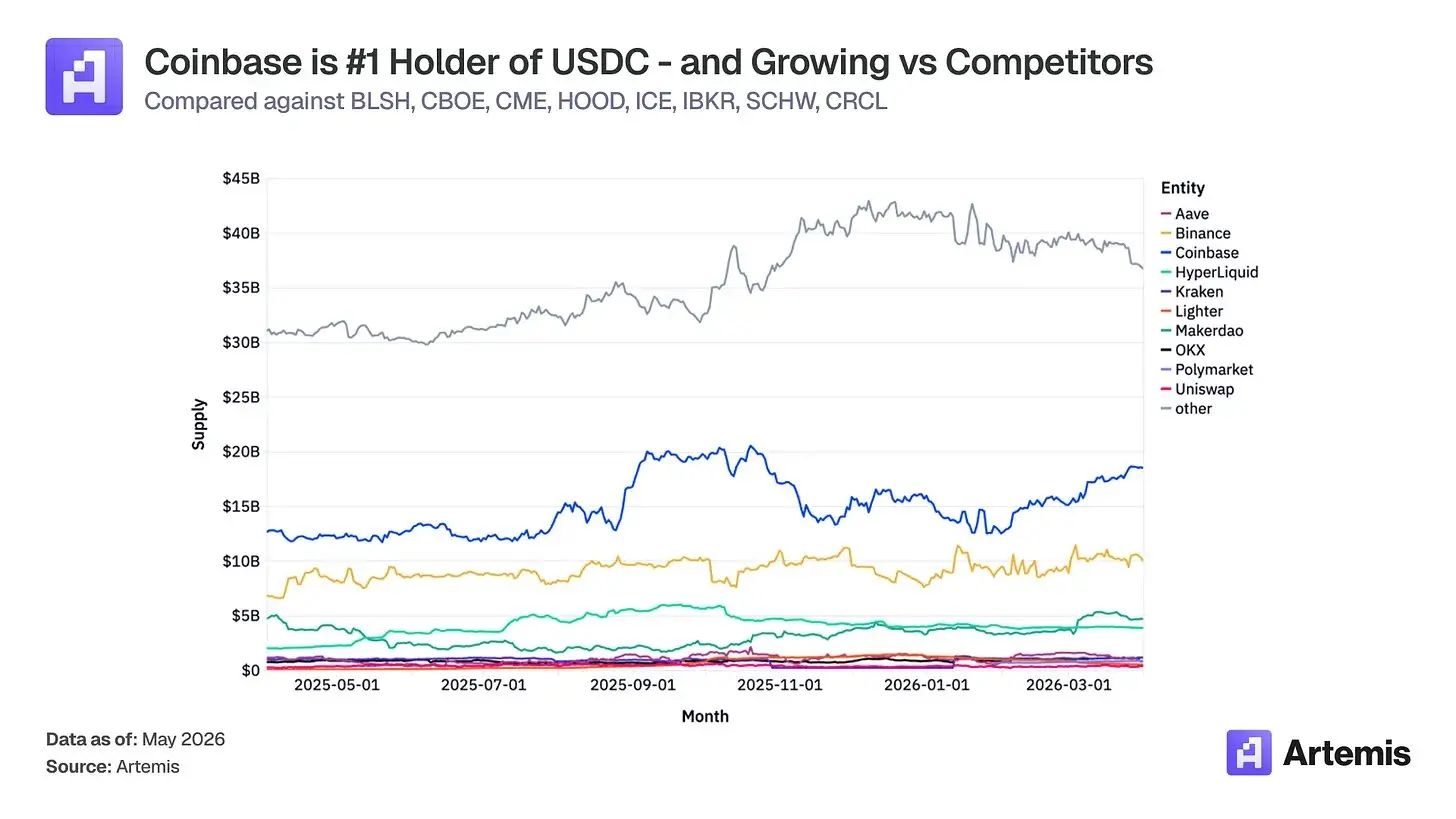

As Coinbase's distribution scale expands (with USDC average balances held in Coinbase products reaching a record $17.8 billion in Q4 2025), its share in the waterfall also increases.

From an investor's perspective, this agreement is more akin to Coinbase outsourcing compliance and reserve management to Circle, rather than Circle paying Coinbase for distribution access.

The cooperation agreement automatically renews every 3 years, subject to three threshold conditions (product, company, distributor). Public filings indicate that once these conditions are met, "the Circle agreement may not be terminated." The renewal mechanism is not a renegotiation cliff, but a continuous lock-in.

For Circle, exiting means cutting off USDC's largest single distribution channel. For Coinbase, the benefits in an upside scenario (scaled stablecoin payments due to regulatory clarity, significant USDC market cap expansion) will flow directly through the same contractual terms. The structure of this contract continuously strengthens Coinbase's market position, regardless of who leads Circle.

Future Growth of USDC

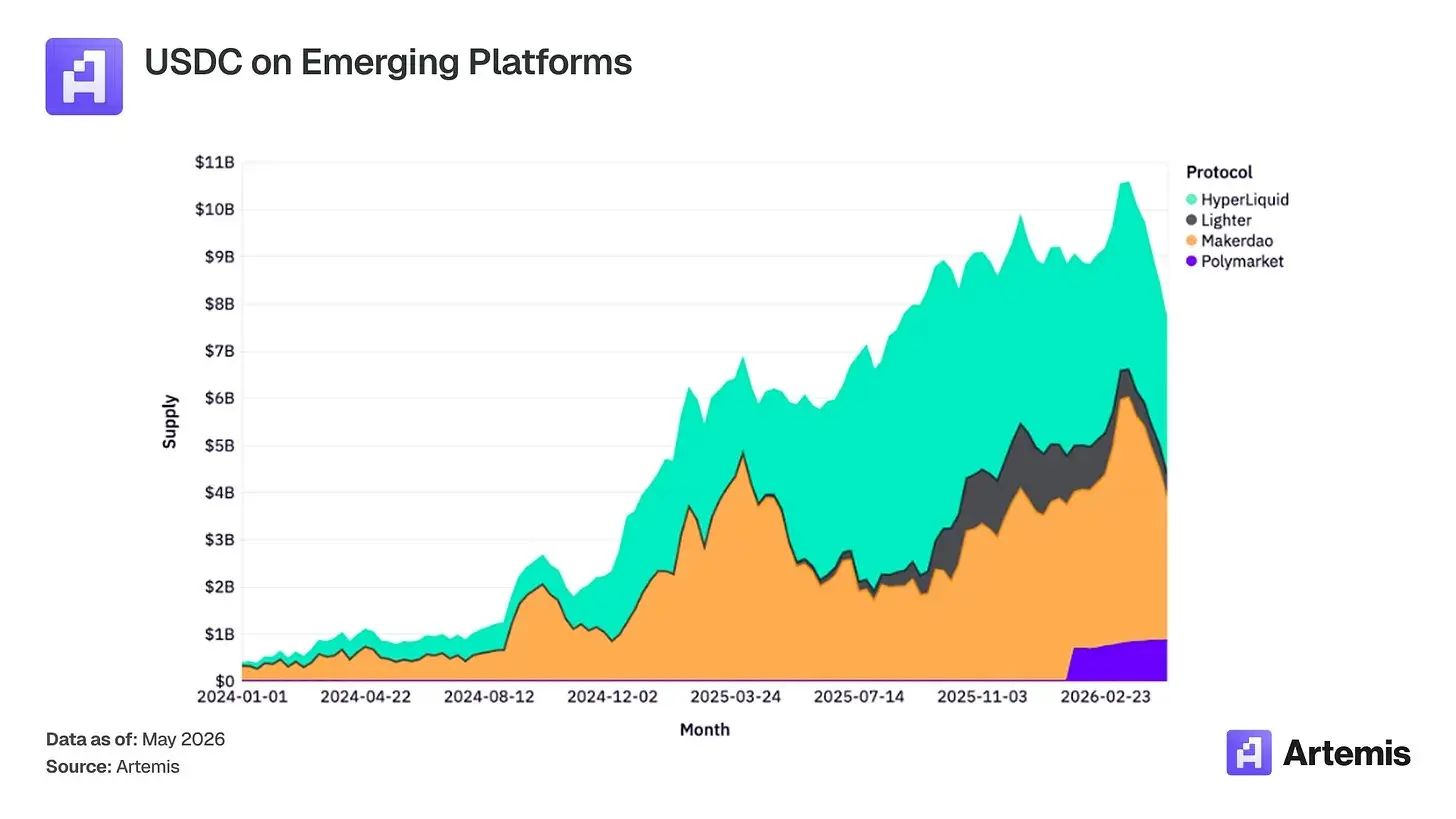

Beyond Coinbase, we also see rich use cases for USDC across numerous emerging protocols. Over the past two years, USDC supply has grown significantly within protocols like Polymarket, Hyperliquid, and MakerDAO. As new financial use cases continue to emerge on blockchain platforms, USDC usage in these protocols will deepen.

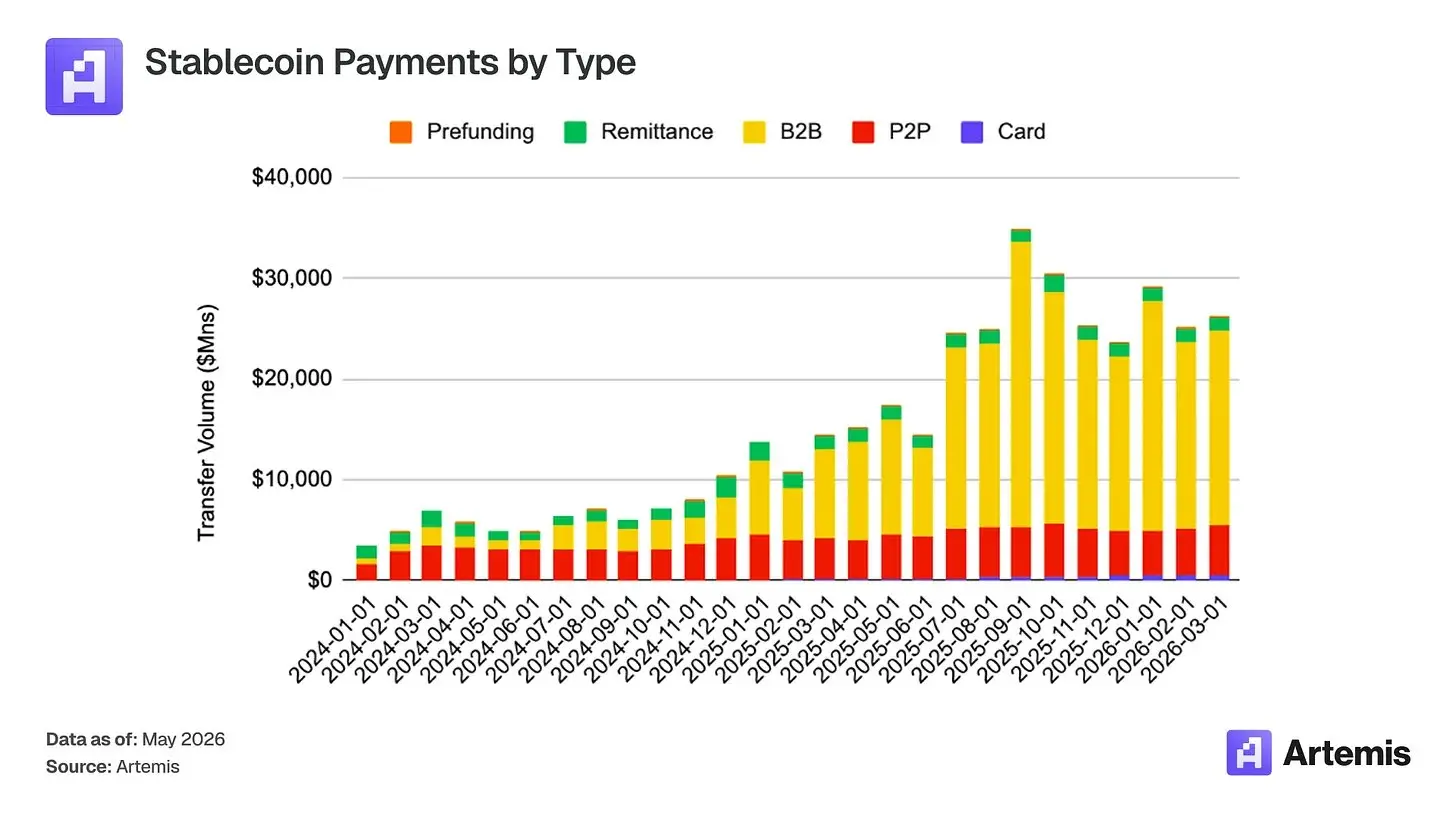

Coinbase is well-positioned to capture the next wave of stablecoin applications (payments). Over the past year, various transaction types based on card payment rails (B2B, B2C) have grown significantly, and USDC's share in such transactions has continued to increase.

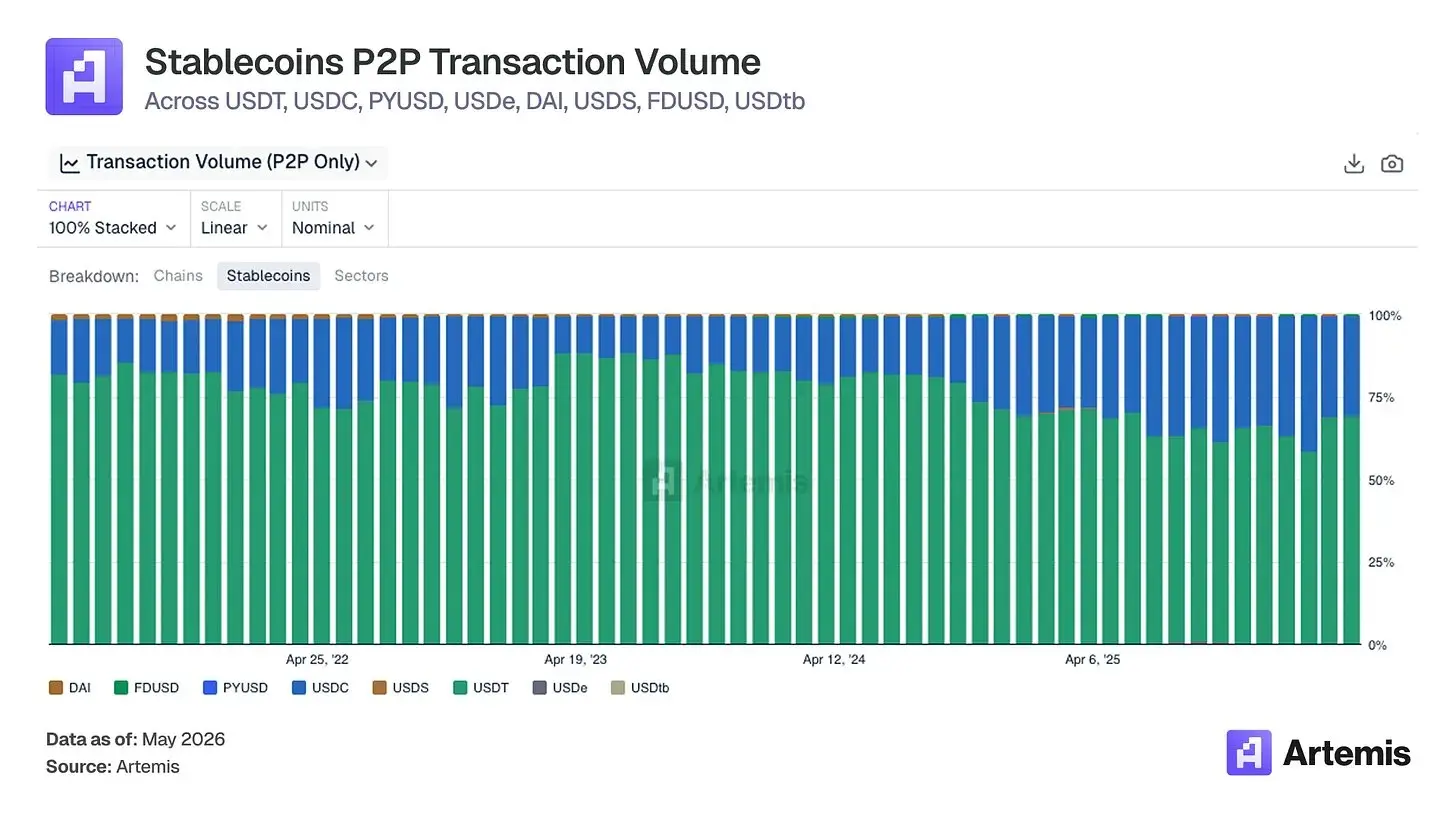

Looking at inter-address USDC transfer data (which can serve as a proxy for the transaction types above), USDC is steadily gaining market share from USDT.

Has the Market Misinterpreted the CLARITY Act?

The Digital Asset Market Clarity Act (H.R. 3633, known as the CLARITY Act) passed the US House of Representatives with bipartisan votes of 294 to 134 on July 17, 2025. The bill aims to establish a comprehensive regulatory framework for digital assets beyond payment stablecoins.

For Coinbase, the CLARITY Act is the most impactful piece of pending US legislation for its regulatory environment, building a largely complete federal regulatory architecture for the digital asset ecosystem in which Coinbase operates.

The CLARITY Act's impact on Coinbase's stablecoin business is also far more profound than commonly perceived by the market.

The revenue generated under current interest rate assumptions from Coinbase's distribution and reserve income-sharing arrangement with Circle is already on par with the economic benefits Circle itself receives as the issuer. Meanwhile, Coinbase's USDC Rewards program contributes another revenue stream, the ultimate size of which depends on the final wording of the Tillis-Alsobrooks compromise.

The market underestimates the scale and durability of these stablecoin-related revenues, viewing them as ancillary to the exchange business rather than independent infrastructure economics.

The CLARITY Act further strengthens this thesis by formally establishing the broader regulatory framework upon which stablecoins rely for clearing, settlement, and circulation, and explicitly defining the registered intermediaries through which institutional stablecoin flows pass. It reframes Coinbase's stablecoin business as the application layer of a regulated, rapidly institutionalizing system, rather than a consumer product line that fluctuates with retail token trading volumes.

Why Coinbase is the Winner in the Agent-Based Payments Race

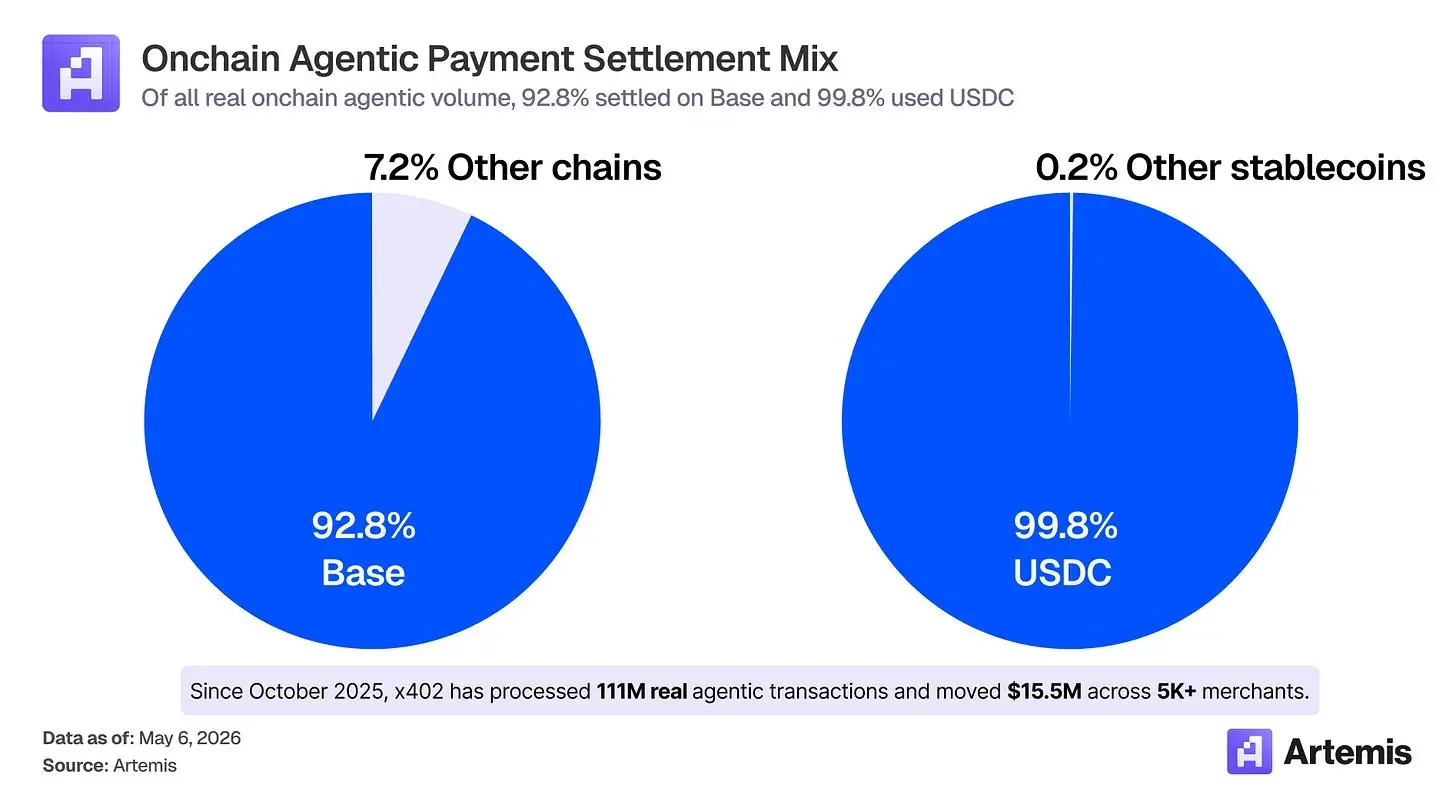

Most investors view Stripe (valued at $159 billion in February 2026) and Tempo as the clear winners in agent-based commerce, but on-chain data tells a different story: 92.8% of real agent-based payment volume occurs on Base, and 99.8% is settled in USDC.

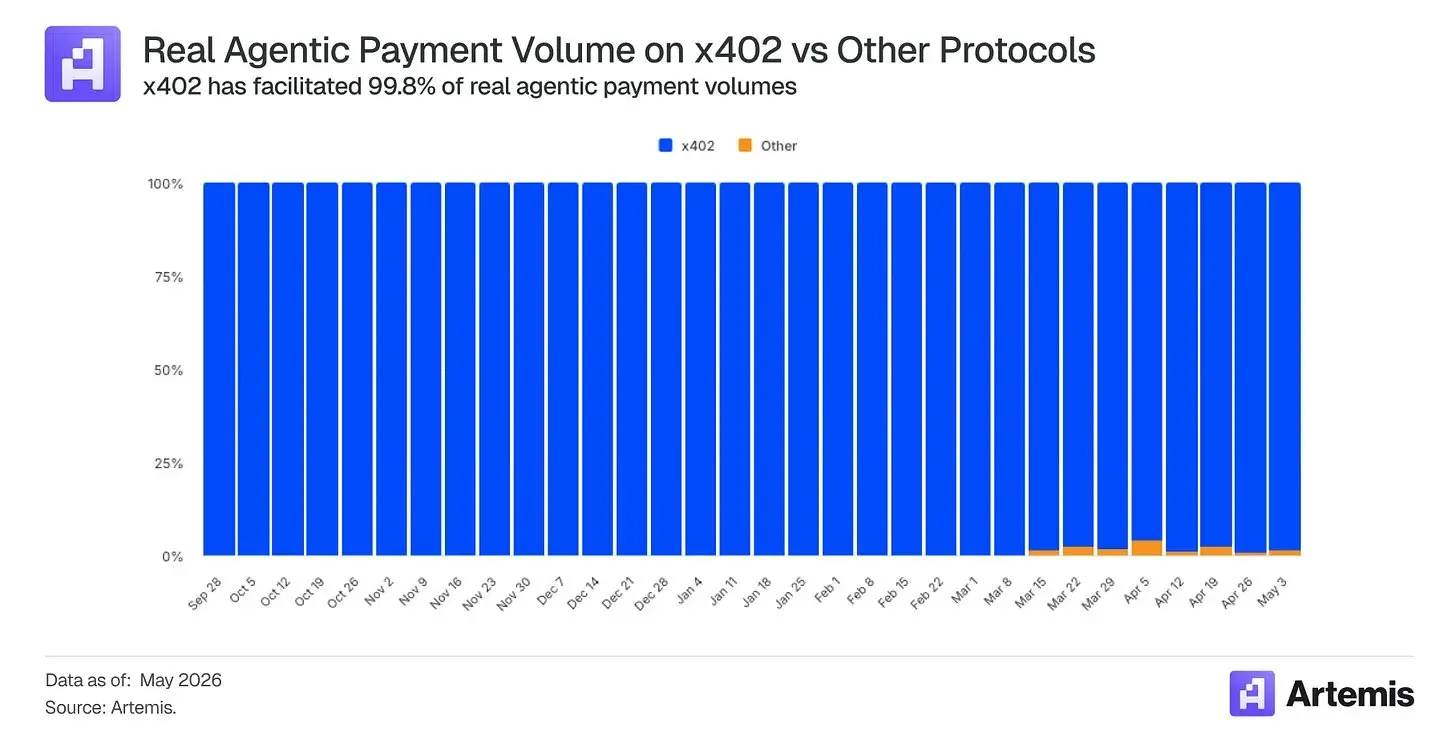

And of all agent-based payment volume, over 99.8% is completed via x402, an open payment protocol spearheaded by Coinbase.

AI agents are evolving from assistants that answer questions into autonomous systems that execute transactions on behalf of users, purchasing APIs, data endpoints, compute, inference services, and various resources at sub-cent pricing and machine speed.

Existing card payment rails are simply not designed for this. A typical card transaction has fixed costs of approximately $0.03 to $0.04 even before interchange fees, making a $0.003 API call economically unfeasible—a full two orders of magnitude difference.

In contrast, settling with stablecoins on a high-throughput L2 costs fractions of a cent, takes seconds, and requires no human intervention to set up billing relationships.

McKinsey predicts global agent-based commerce sales will reach $3 to $5 trillion by 2030. Gartner estimates that by 2028, AI agents will be involved in over $15 trillion of B2B procurement decisions.

These numbers have directional significance and should be taken as trend indicators; however, it is certain that if these scales materialize, stablecoin payment rails will be structurally prioritized, and USDC is already the default asset on this rail, from which Coinbase will directly benefit.

Current Track Record

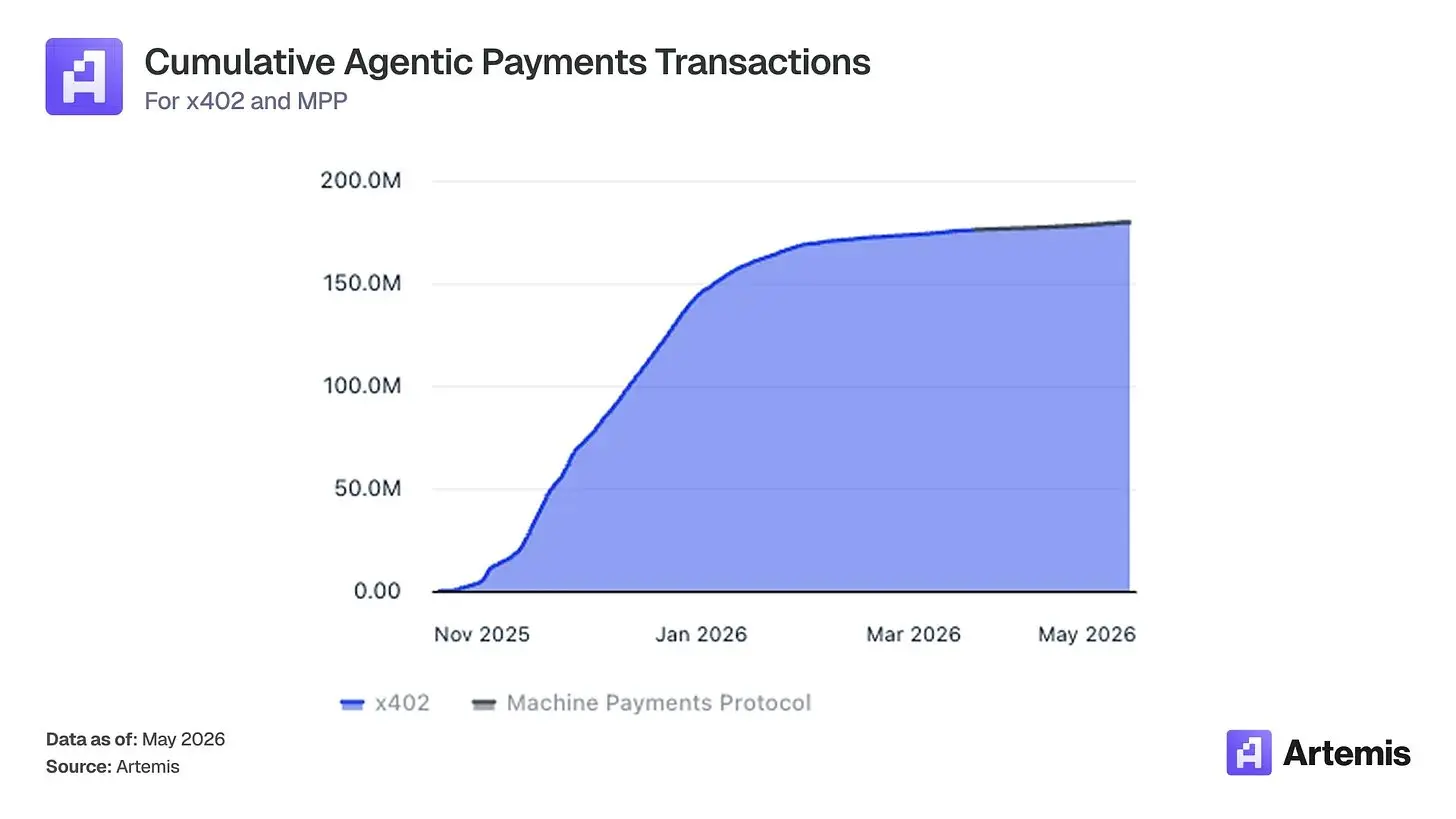

The x402 standard, an HTTP-native micropayment protocol co-developed by Coinbase (now managed by the Linux Foundation), has become the mainstream open protocol for agent-initiated payments.

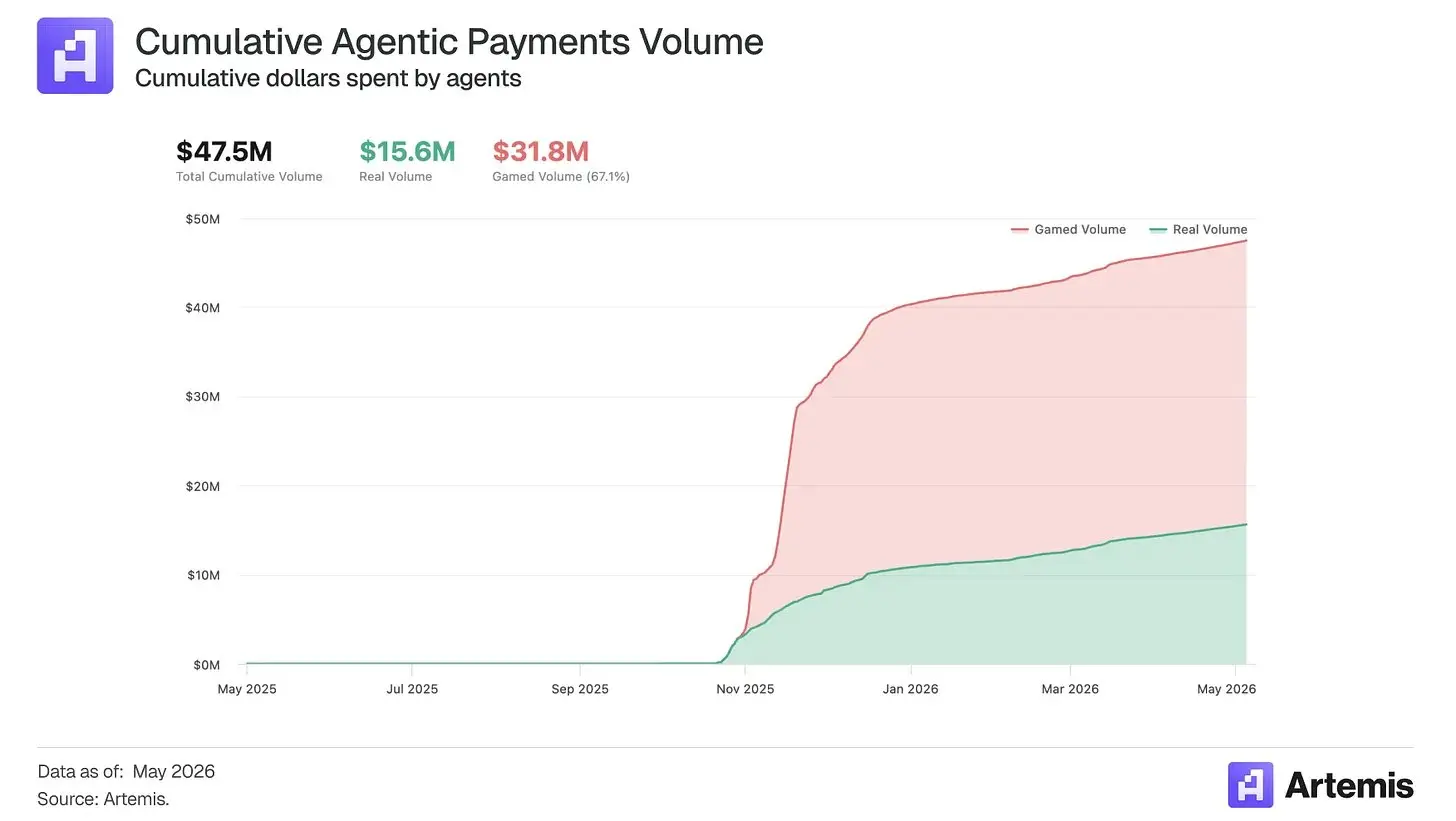

Since October 2025, x402 has processed over 180 million agent-based payments, circulating $47.5 million in agent spending across more than 5,000 agent-facing merchants.

When merchants open their services for agent invocation, Coinbase's L2 and USDC are already the default payment rails.

Furthermore, Agentic.Market provides Coinbase a path to control the resource discovery layer. If agents use it to discover, evaluate, and route x402 services, then value accumulates not only through Base settlement and USDC transaction volume, but also in Coinbase's role as the transaction coordination platform between agents and services.

How Coinbase Monetizes

Coinbase captures the economic value of agent-based payments through four revenue lines that are mutually reinforcing and built around the stablecoin core: USDC float interest, Base settlement revenue, CDP/AgentKit monetization, and Agentic.Market distribution revenue.

1. USDC Reserve Earnings

Coinbase's most significant upside revenue source is not trading fees, but float interest. Agent wallets need prefilled balances to authorize autonomous spending, pay API fees, cover usage-based services, and settle machine-to-machine commerce in real-time.

As agents become economic actors, USDC balances held in wallets controlled by Coinbase become deposits that generate continuous income. Every dollar of USDC held by an agent, regardless of turnover frequency, generates reserve earnings.

2. Base Sequencer Revenue

Every x402 or MPP-type transaction settled on Base becomes a sequencer transaction that can generate priority fees. This revenue line scales with the number of transactions, not payment amounts—a key point, as agent-based commerce is likely characterized by high frequency and low value, distinct from human commercial behavior.

However, as transaction costs tend to decline long-term, sequencer fees may have the smallest upside potential.

3. CDP, AgentKit & Facilitator Monetization

Coinbase can monetize at the developer level—the layer that enables agents to hold wallets, manage permissions, sponsor gas fees, complete x402 payments, and interact with paid services. This includes facilitator fees for x402 transactions, wallet infrastructure, gasless transactions, key management, policy control, and enterprise-grade developer tools.

If CDP becomes the default infrastructure stack for agent-based payments, Coinbase gains platform revenue even if individual payment amounts are low.

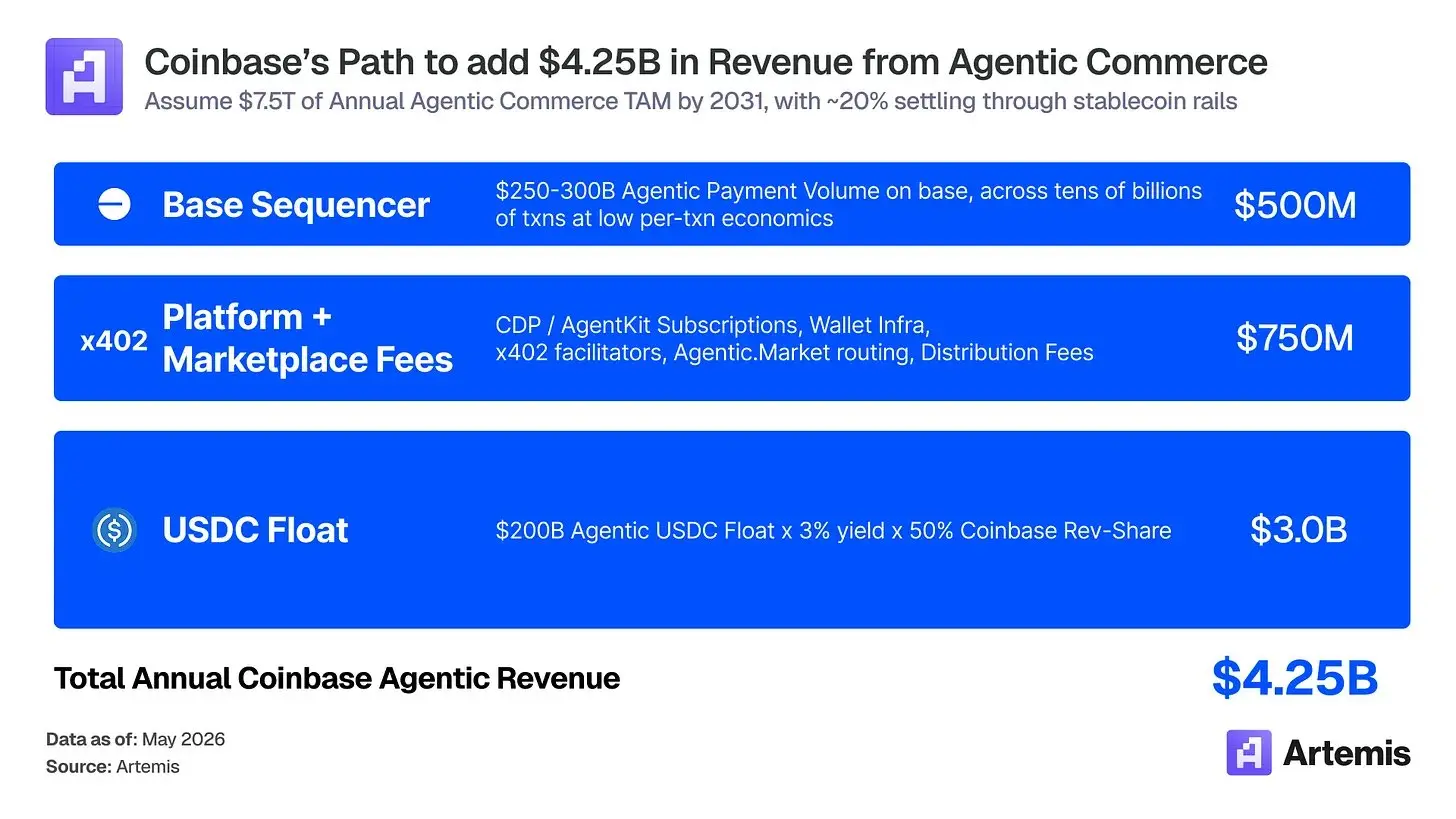

Scale Modeling

We assume annual agent-based commerce volume reaches $5 trillion by 2030. A majority of this will still flow through traditional rails like cards, ACH, and bank transfers, especially for large consumer and enterprise purchases.

However, machine-native, high-frequency, cross-border, API-based commerce will disproportionately adopt stablecoins and payment standards like x402 and MPP.

In an optimistic scenario, about 20% of agent-based commerce settles via stablecoin rails, corresponding to annual stablecoin agent-based payment volume of approximately $1 to $1.5 trillion. The optimistic scenario revenue breakdown is as follows:

● USDC Float Interest: $200 billion average agent USDC balance × 4% reserve yield × 50% Coinbase attribution share = $4 billion

● CDP/AgentKit/Facilitator/Agentic.Market: Developer subscriptions, wallet infrastructure, x402 facilitator fees, market routing, service provider analytics, and distribution fees = $750 million

● Base Sequencer: $250 to $300 billion agent-based payment volume processed on Base, tens of billions of transactions, low economic gain per transaction = $250 million

Total approximate $4.25 billion Coinbase-attributed agent revenue. The key takeaway: Once Coinbase becomes the operating account, developer platform, discovery layer, and settlement rail for autonomous commerce, real value accumulates continuously—and over the past few months, they have taken solid steps on this path.

Why Coinbase and USDC Will Prevail

Coinbase's advantage lies in controlling four mutually reinforcing layers of the agent-based payment stack: USDC float interest, Base settlement, CDP/AgentKit infrastructure, and the Agentic.Market discovery layer.

USDC is already the default settlement asset, meaning developers prioritize integrating it because it has the best tooling, deepest liquidity, and broadest developer support.

Base benefits from this, becoming the natural settlement chain for USDC-native agent-based payments, with low developer friction and growing facilitator coverage.

CDP and AgentKit sit a layer above, providing developers with wallets, key management, gas sponsorship, and payment infrastructure, giving agents genuine economic agency.

Finally, Agentic.Market has the potential to become the discovery and routing layer where agents find, compare, and invoke x402 services.

Competitors wanting to enter this market must simultaneously replicate liquidity, settlement capabilities, developer infrastructure, and distribution channels. And with every new agent, merchant, or service added, the existing Coinbase tech stack becomes increasingly difficult to dislodge.

Conclusion

The market views Coinbase as a crypto exchange, overlooking that it is building the underlying platform for AI-native finance.

Global leaders predict stablecoin supply reaching $3 trillion and agent-based commerce reaching $5 trillion by 2030. Stablecoin momentum has decoupled from crypto asset prices.

Coinbase has positioned itself as a core winner in this world and is already showing early leadership. x402, USDC, and Base have become the de facto tech stack for agent-based commerce, with each layer holding over a 90% share advantage against competitors.

Coinbase's unique position stems from developing Base, incubating x402, and holding a favorable position in the USDC economic split.

The market mispricing logic rests on three pillars.

The structure of the Circle agreement is a continuous lock-in, not a renewable contract, meaning the stablecoin revenue line has durability, not cliff risk.

The CLARITY Act formally codifies the regulated infrastructure layer Coinbase already operates, re-basing its valuation benchmark from a consumer product to a core market utility.

The flywheel effect of the four-layer agent tech stack (USDC, Base, CDP, Agentic.Market) is self-reinforcing; with every new agent and merchant added, the moat becomes harder to breach.

Coinbase's valuation benchmark should be closer to infrastructure companies than brokers.

We believe, riding these two epochal tailwinds, Coinbase will grow into a $300 billion company, with the majority of its revenue coming from subscription and service business lines like stablecoins and agent-based commerce.