Author: Jonah Burian

Compiled by: Jiahuan, ChainCatcher

Many speculate that the next billion users of blockchain will be Agents. But few ask the further question: In that world, who will make money?

Every previous theory of value capture in the crypto space assumes the user is human. The "Fat Protocols" theory posits that protocols are best at monetizing human users.

The "Fat Apps" theory I explored with my colleagues in "How to Capture Value" and "The Great Repricing" argues that the application layer can do better. But Agents change the nature of the user, and existing theories will break down accordingly.

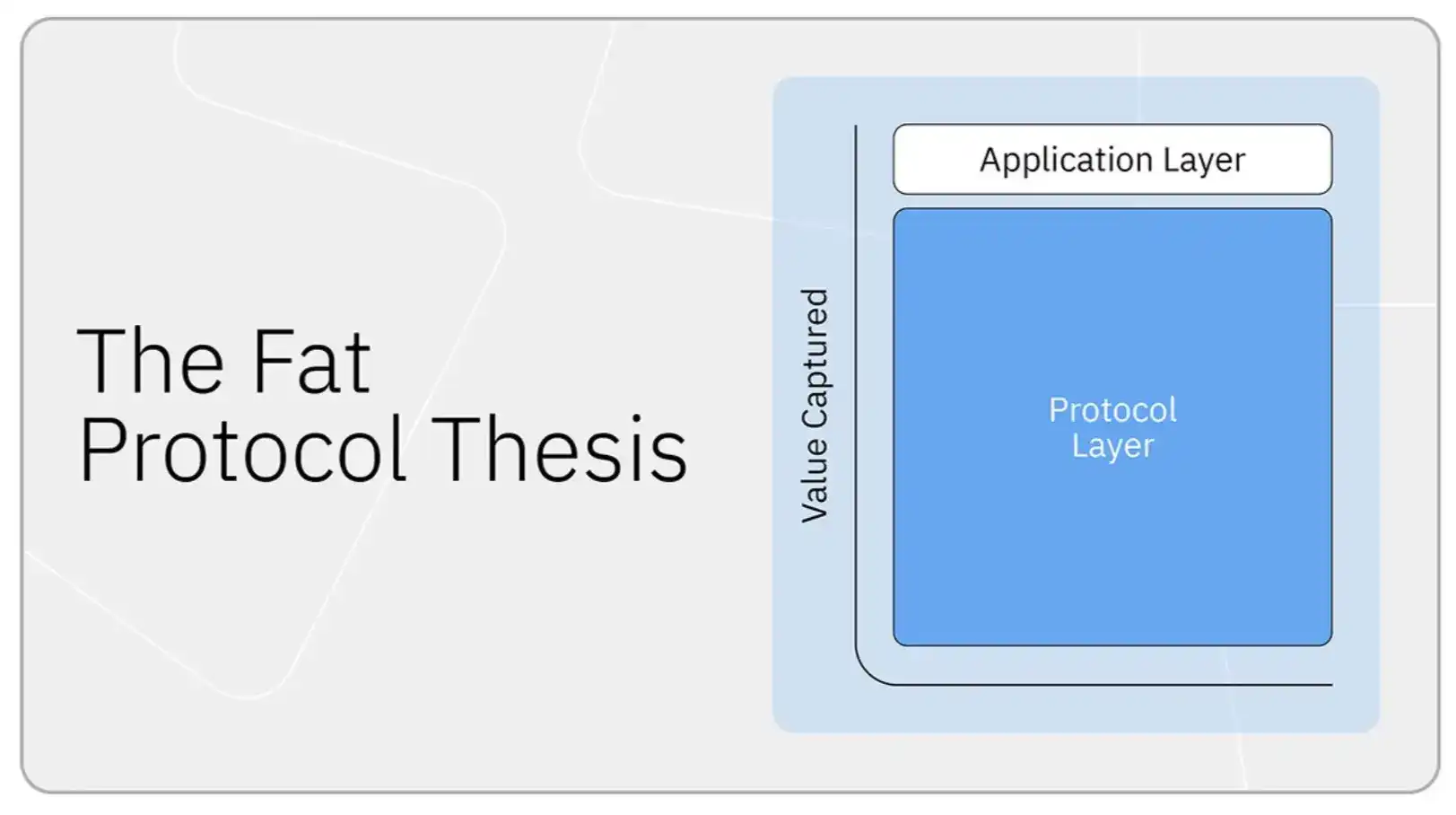

The Fat Protocols Theory

In 2016, @jmonegro proposed "Fat Protocols." For nearly a decade, it has been the dominant value capture theory in crypto.

The core idea: In the traditional internet, value accumulates at the application layer (@Google, @facebook), while the underlying protocols (TCP/IP, HTTP) capture almost no value. The crypto world will completely reverse this. Blockchains have open, shared data, so applications will become commoditized.

And because using the network requires consuming the protocol's token, the token will capture the speculative value generated by usage growth as it appreciates. Each application's success drives demand for the token. The underlying protocol will grow faster than any application built on top of it.

For years, this seemed correct. Bitcoin and Ethereum's values far surpassed any companies built on them.

This model works perfectly when the protocol itself is scarce, costly to build, and difficult to replace. Bitcoin and Ethereum in 2017 were indeed very scarce; there weren't dozens of general-purpose L1s competing for the same workloads.

Block space was sufficiently constrained that holding the underlying asset felt like holding a piece of every application that needed it.

Today, reliable alternatives exist at every layer of the infrastructure stack: multiple high-throughput L1s, dozens of L2s, and modular settlement and data availability (DA) layers competing fiercely on price. Block space has gone from constrained to abundant.

As cross-chain bridges and aggregators make the underlying chain nearly invisible to users, user switching costs collapse. Infrastructure becomes interchangeable, and interchangeable commodities compete on price. The result is that protocol pricing power dies along with scarcity.

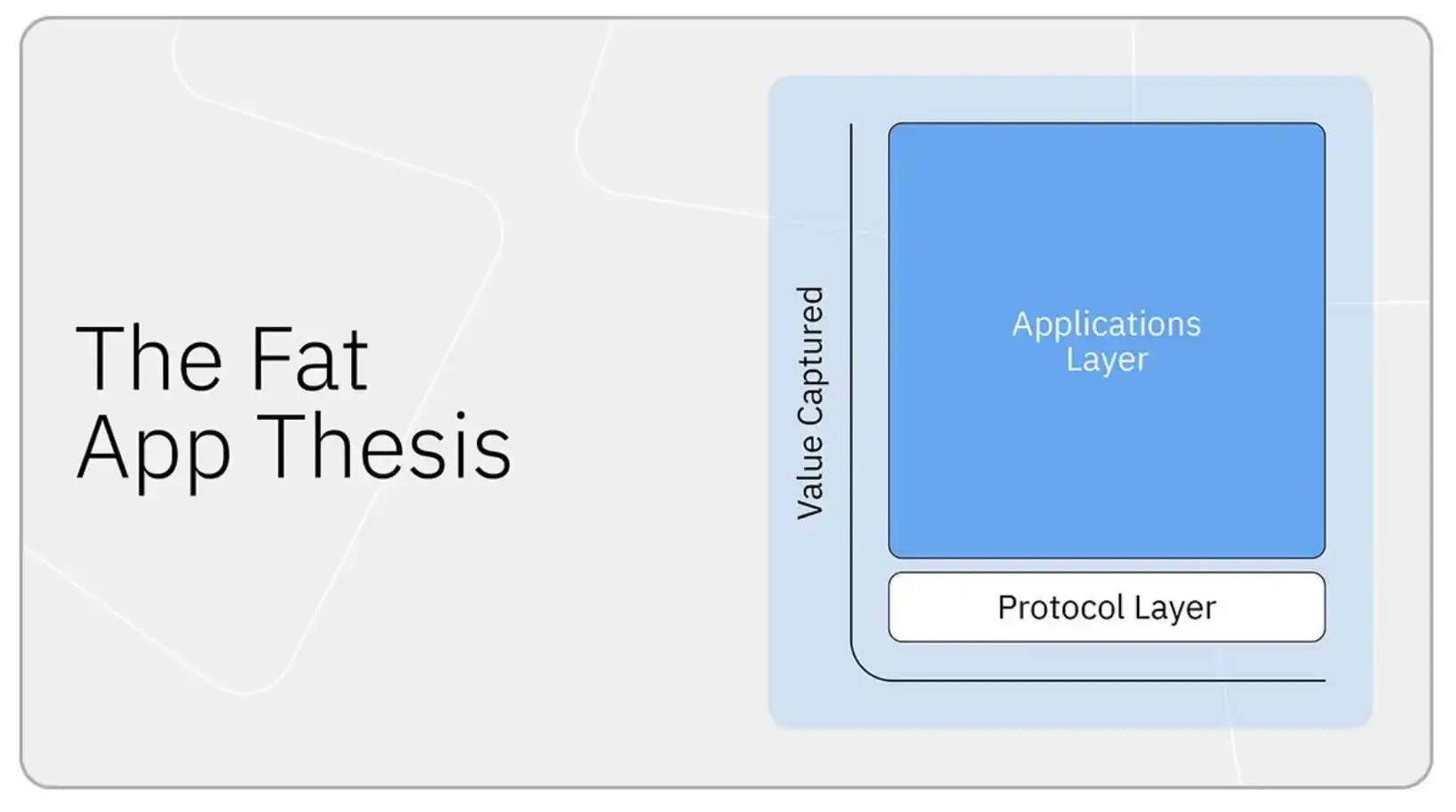

The Fat Apps Theory

By 2026, the entities capturing most of the economic benefits are applications, not protocols: e.g., @phantom, @coinbase, @Polymarket, @Pumpfun.

In my view, the reason is that the most valuable asset in crypto is the user relationship.

If you control the user interface and transaction flow, you control distribution, and can profit from almost any on-chain product users touch: swaps, lending, staking, minting, and fiat on/off ramps. This is probably why funds are so obsessed with neobanks.

Applications also push infrastructure into pure price wars, forcing infrastructure margins down to marginal cost. I documented this dynamic in "How to Capture Value." The same dynamic is playing out in the stablecoin space, which I've discussed elsewhere.

Asset prices are reflecting this theory. Spencer and I called this shift "The Great Repricing": in this cycle, value is starting to accrue to the layer that owns the user.

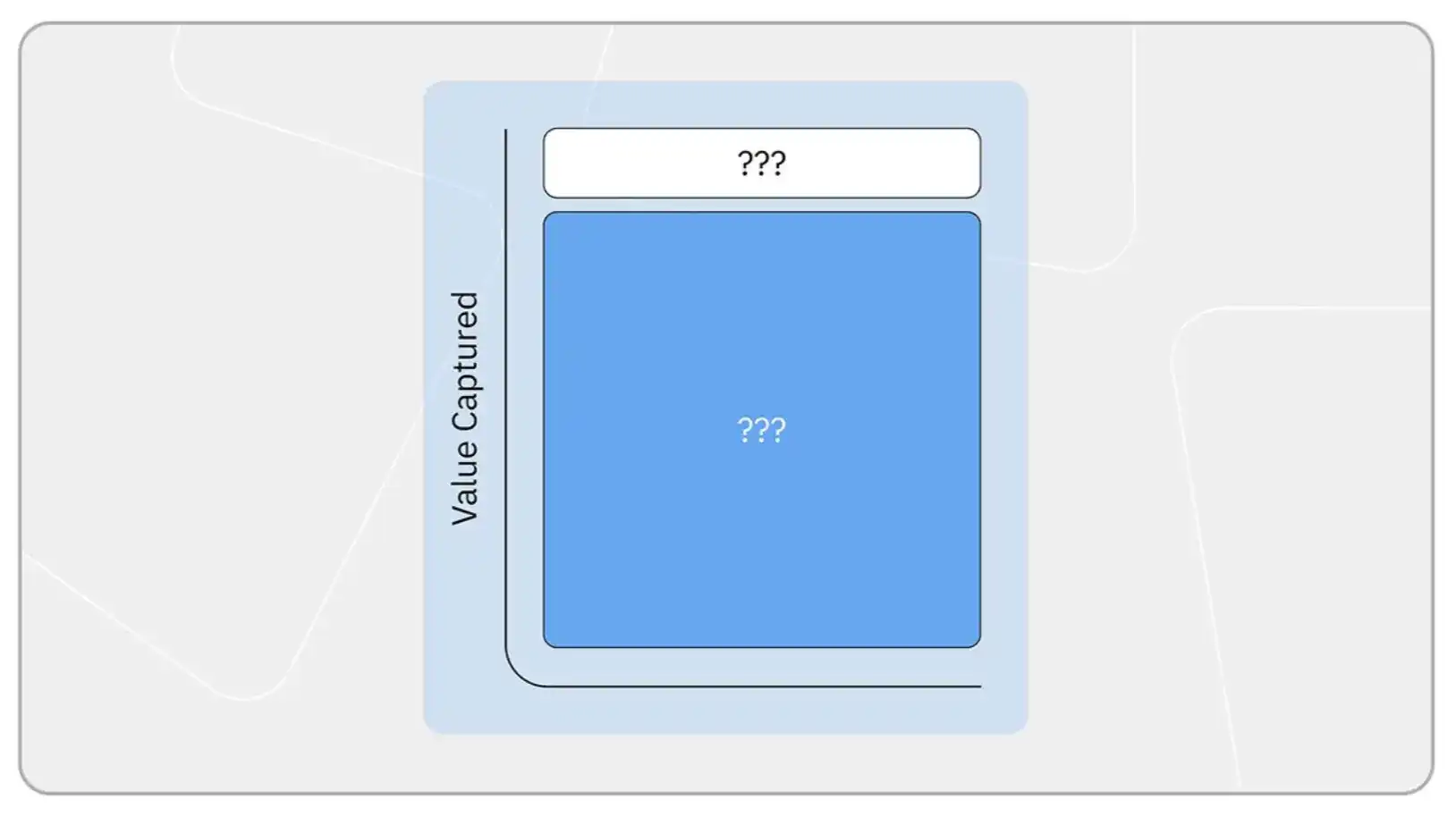

Why Agents Break This Logic

The Fat Apps theory assumes users are humans who value UX, brand, and convenience. But Agents don't care about any of that. They call APIs directly, have no brand loyalty, and switch between platforms at zero cost.

When the user becomes software, owning the user relationship is no longer an unbreakable moat. The entire front-end moat upon which the Fat Apps theory relies is failing.

So, who captures value in the age of Agents?

Applications Go "Headless"

In one version of the future, winners at the application layer remain winners by shedding their front-end interface, i.e., going "headless."

Wallets and aggregators have already done the hardest work: integrations with dozens of protocols, routing logic, authentication, and fiat on/off-ramp infrastructure.

The logical next step is to open this tech stack as an API for Agents, letting Agents route through them—just as humans route through @phantom or @JupiterExchange today.

In this world, the Fat Apps theory survives. It just loses its front end. The companies that won in the human era transform into pure back-end infrastructure for Agents. We already see traditional SaaS companies like Salesforce moving in this direction.

The Resurgence of Protocols

In another version, Agents completely skip the middle layer.

If integration becomes easy enough (well-documented APIs, standardized RPCs, predictable execution semantics), Agents have no real reason to pay an aggregator to do something they can do themselves. Aggregators' advantages in the human era were UX and handling routing complexity.

But Agents don't need UX, and routing is an engineering problem that Agents are increasingly good at solving.

If the world evolves this way, the Fat Protocols theory gets a second life.

Pricing Power Collapses Across the Stack

Perhaps Agents will apply commoditization pressure everywhere. They are perfectly rational, frictionlessly routing to the cheapest venue every single time with zero loyalty.

Applications lose the ability to charge a UX premium from humans. Aggregators and infrastructure lose pricing power because there is no longer human inertia protecting them from price wars.

In this scenario, no one in the tech stack captures much profit. Margins across the supply chain are forced down to marginal cost. The residual value accrues to the owners of the Agents, or to the end-users the Agents serve.

Crypto becomes a utility, and it's hard to make big money in utilities.

Agents Create Unprecedented Activity

The simple take on this is: Agents are doing everything humans do, just faster and at greater scale. Even if margins are compressed, the overall pie grows.

I think there's a more interesting version.

Agents enable activities that were previously infeasible: e.g., continuously rebalancing a portfolio for less than a penny in execution costs, machine-to-machine commerce between Agents, and entirely new markets that exist only because pricing and transaction speeds far outpace what humans can follow.

Current on-chain activity data doesn't reflect this because we assume a human must be involved.

If this is the change Agents bring, then the question shifts from "how is the existing pie divided" to "how much new economic activity pours on-chain, and which layers are ready to serve it."

A Yet-Unnamed Business Model

Every cycle, we try to guess where value will flow, and tend to think existing business models will extend into the future. This assumption usually causes us to miss the new models that haven't yet emerged.

When the internet was new, no one foresaw the attention economy. The idea that "slicing up user attention and auctioning it to advertisers would become the dominant business model, and a single company could capture a significant share of global ad spend" was alien. It only seems inevitable in hindsight.

AI looks like one of the biggest technological disruptions in decades. In an Agent-dominated world, some value capture might flow to business models no one is talking about today. And the entities capturing that value might not be the ones the market is currently focused on.

What to Watch

The most likely outcome is not one system completely replacing the other. For a long time, humans and Agents will coexist as crypto users, with entirely different maps of value capture.

As long as humans interact on-chain, the Fat Apps theory still applies: consumers willing to pay for UX, brand, and convenience will continue to pay a premium to the applications that own that relationship. And the layers involved in Agent transactions will be governed by a separate set of theories, whichever of the above scenarios becomes reality.

For builders, I think the question worth iterating on the Agent side is: What actually makes an Agent come back to you instead of routing directly to the next cheapest alternative? UX probably isn't the answer. Liquidity, latency, settlement guarantees might be.