Author: 137Labs

On February 23, a stablecoin named USD1 suddenly showed a significant discount in the secondary market.

On-chain quotes once fell to around 0.98 USDT, and social media quickly amplified the news.

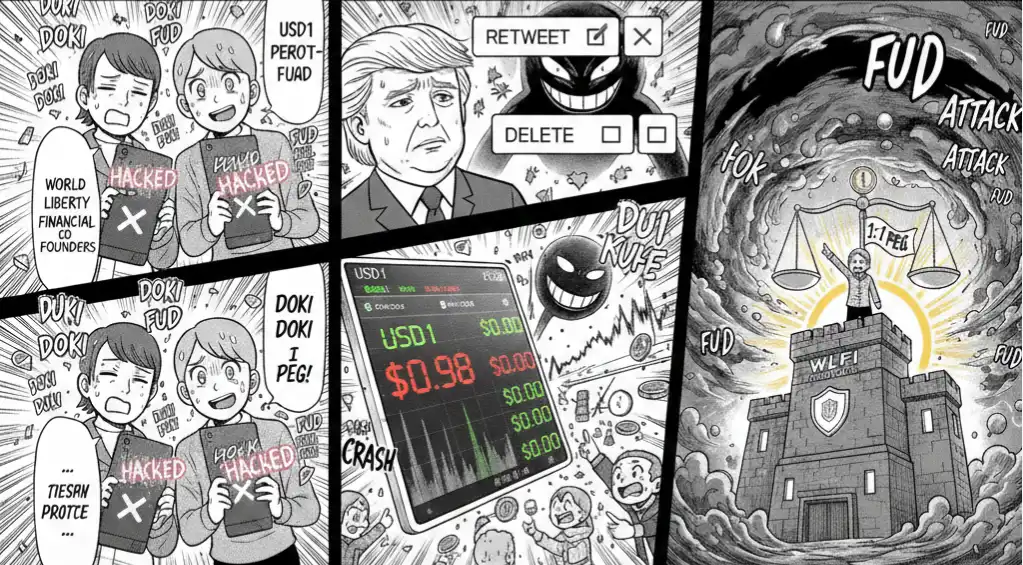

The project team, World Liberty Financial (WLFI), subsequently stated publicly that this was a "coordinated attack" and emphasized that the reserve and redemption mechanisms were unaffected.

The price then recovered.

But the problem had already emerged——

When a "stablecoin" begins to trade at a discount, is it merely a liquidity friction, or a precursor to a crack in the credit structure?

I. Timeline: From the Wicking to the "Attack" Narrative

Based on reports from CoinDesk, The Block, Decrypt, WuBlockchain, PANews, ChainCatcher, and others, the sequence of events is roughly as follows:

1️⃣ Abnormal Volatility in the Secondary Market

-

USD1 quickly fell to around 0.98 in some trading pairs

-

The discount lasted for a short time

-

The price subsequently recovered

Unlike the brief depegging of USD Coin in 2023 due to banking risks, no clear systemic banking shock occurred this time.

2️⃣ WLFI's Official Response

WLFI stated externally:

-

This was an organized short attack coupled with a public opinion coordination attack

-

Reserve assets showed no abnormalities

-

Redemption function is normal

-

The 1:1 peg structure remains unchanged

This explanation was subsequently reported by Chinese media including WuBlockchain and ChainCatcher.

3️⃣ Social Media Amplification Effect

The event spread rapidly on platform X.

Some related tweets were deleted, fueling further market speculation.

In the current emotionally charged market environment, "deletion behavior" is often interpreted as a signal, not a random operation.

Thus, the question shifted from "Is the price depegged?" to:

-

Is there a reserve risk?

-

Is there a concentrated bank run?

-

Is there insufficient information disclosure?

II. The Nature of Depegging: A Liquidity Problem or a Solvency Problem?

Judging a stablecoin depegging event hinges on distinguishing between two completely different risk structures.

The first is a liquidity shock.

In this case, reserves are still sufficient, the redemption mechanism remains unimpeded, but due to insufficient trading depth, market maker withdrawal, or concentrated selling pressure, the secondary market experiences a brief imbalance. Once the arbitrage mechanism kicks in, the price usually recovers quickly.

The second is a solvency crisis.

If the reserve assets themselves are problematic, or if the assets suffer from maturity mismatches and cannot be liquidated immediately, then the depegging is no longer a trading-level fluctuation but a repricing of the balance sheet. In this case, the discount often widens persistently, accompanied by redemption delays or a collapse in trust.

Based on the information disclosed so far, USD1 is closer to the former.

It is completely different from the algorithmic death spiral of TerraUSD (UST) in 2022. UST's collapse stemmed from mechanism failure, while USD1's wicking更像 (more like) a liquidity tilt within a short period.

But even so, this event still holds significance.

Because the true anchor of a stablecoin is not just the reserve assets, but market trust.

Once trust is questioned, the price reacts ahead of the fundamentals.

III. The Credit Structure of Stablecoins: Where Exactly is Their "Stability"?

Stablecoins are essentially the "base money" of the crypto market.

Their credit support generally comes from three models:

-

Algorithmic

-

Collateralized

-

Centrally Custodied Reserve-backed

USD1 belongs to a more centralized reserve structure.

The risk of this model lies not in the algorithm, but in:

-

Reserve Transparency

-

Asset Liquidity

-

Maturity Structure

-

Market Making Depth

Once the market suspects that reserves are discounted or face liquidation risks, the price often falls first.

This is highly similar to a "shadow bank run" in traditional finance—as soon as depositors start to doubt, the act of withdrawal itself amplifies the risk.

IV. Why Was the Market Reaction Particularly Sensitive This Time?

The fear index was already at an extreme low that day.

In an environment where liquidity was already tight:

-

Leverage levels decreased

-

Risk appetite weakened

-

The market became highly sensitive to uncertainty

Stablecoins are not just trading tools; they are the cornerstone of lending and liquidity.

Once a discount appears, the chain reaction may include:

-

Decrease in collateral ratios

-

Triggering of liquidations

-

Further compression of leverage

-

Capital outflow from the market

Therefore, even though the price recovered quickly, the psychological shock did not disappear simultaneously.

V. Is the "Attack" Narrative Valid?

WLFI attributed this volatility to a "coordinated attack".

Short attacks and public opinion resonance are not uncommon in the crypto market.

When trading depth is insufficient and market sentiment is fragile, prices are easily subject to amplified volatility.

But whether an attack can be sustained depends on one core factor:

Does the market believe the reserves are real, redeemable, and sustainable?

If the reserve structure is transparent and redemptions remain smooth, attacks often find it difficult to be effective in the long term;

If reserve disclosure is insufficient, panic is more easily self-reinforcing.

VI. The Differences Between USD1, USDC, USDT, and the True Meaning of This Depegging

Historically, USDC fell to $0.88 in 2023 due to banking risks; its problem stemmed from exposure to custodian bank risks and limitations on the pace of reserve liquidation.

Meanwhile, Tether has experienced minor depegging multiple times, usually during extreme panic phases or under concentrated withdrawal pressure, but the key to its eventual recovery lies in the continuous availability of the redemption mechanism and the verification of reserve redemption capability.

USD1 currently seems to be in the midst of a "trust stress test".

This event is closer to a liquidity shock than a solvency crisis.

The rapid price recovery indicates that a systemic bank run has not yet formed.

But what is truly worth paying attention to is not that single price of 0.98, but whether the market has begun to reassess the risk premium of "stability".

Stablecoins are the monetary base of the crypto market.

When the market questions their safety, the impact transmits outward along the credit chain:

-

Leverage decreases

-

Lending contracts

-

Collateral assets are repriced

-

Capital flows back to mainstream assets or exits the market

Even if the event itself is just short-term volatility, it will increase the cost of future financing and liquidity.

Depegging is never just a price problem; it is a credit pricing problem.

The price can recover quickly,

but trust takes time to repair.

USD1's depegging may not necessarily evolve into a systemic risk,

but it reminds the market——

During periods of liquidity contraction,

credit always changes before the price.

And once credit begins to be revalued,

the entire risk structure也随之 (also随之 -也随之) changes accordingly.