Author: Xiao Bing, Deep Tide TechFlow

On May 22nd, after China Securities Regulatory Commission (CSRC) announced plans to impose severe penalties on three overseas brokerages—Futu, Tiger Brokers, and Longbridge—their stock prices plummeted sharply.

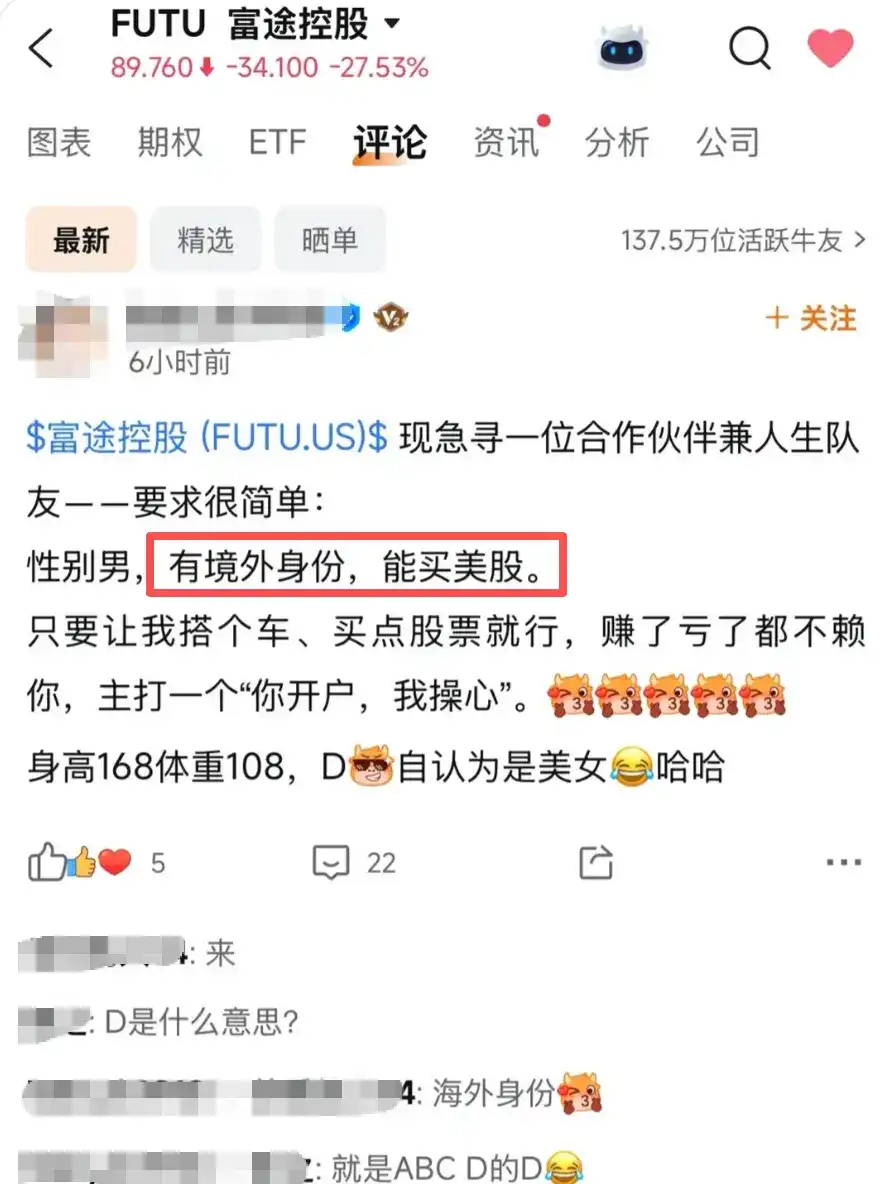

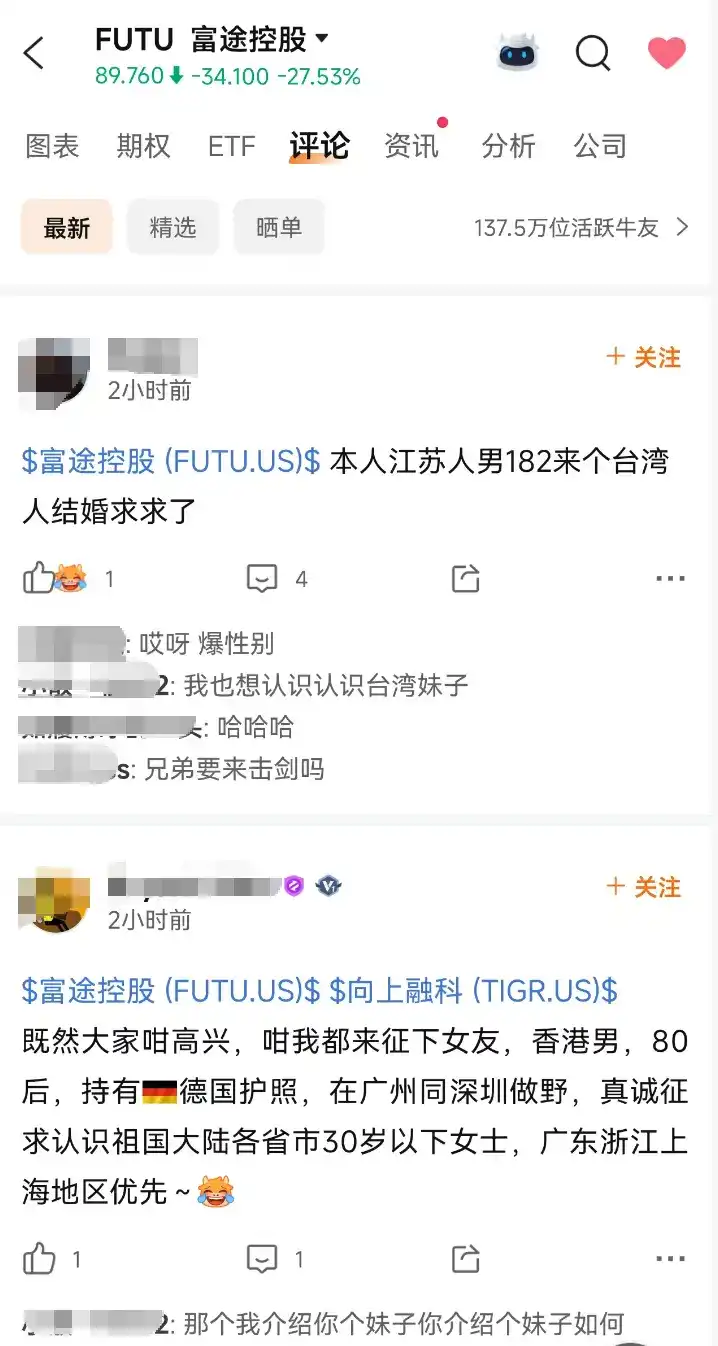

However, in the community of Futu's own app, the tone took a sudden turn. Beyond discussing stocks, it became a matchmaking platform for investors overnight.

A self-proclaimed D-cup beauty from mainland China is seeking an overseas man; a mainland-born '90s generation individual with a 2046% return is willing to consider "any gender" for an identity swap; a Hong Kong man holding a German passport is inverting the selection criteria, preferring "Guangdong, Zhejiang, or Shanghai natives"......

This isn't just anecdotal. You're witnessing a latent, securitized marriage market taking shape in real time within the Futu community. Demand side, supply side, price preferences, geographical screening conditions... all spontaneously forming. This is the most honest natural language leak of the mindset among China's middle-class investor group in 2026.

The Regulatory Hammer Falls

On May 22nd, China's Securities Regulatory Commission, along with seven other departments, jointly issued the "Implementation Plan for Comprehensive Rectification of Illegal Cross-border Securities, Futures, and Fund Business Activities." On the same day, they announced plans to impose severe penalties on three overseas brokerages: Futu Holdings is slated to be fined approximately 1.85 billion RMB; Tiger Brokers faces a fine of 411.2 million RMB; Longbridge is also on the list. Both Futu and Tiger's US-listed shares plunged over 30% in pre-market trading.

The brokerages' responses were measured in their wording. Futu stated that as of the end of Q1 2026, funded accounts from mainland China accounted for about 13% of the company's total funded accounts; Tiger Brokers said client assets from mainland China constituted roughly 10% of the group's global total assets. Both emphasized that "business operations in all regions outside mainland China remain normal."

But for mainland users who already hold US stocks in their Futu or Tiger accounts, the truly stinging piece of information boils down to one phrase:

Sell only, no buying.

This means that for the foreseeable future, if you want to open a new US stock account to buy NVIDIA, Tesla, or an S&P 500 ETF, you must first possess identification proving you are a non-mainland Chinese resident.

Looking back over the past three years, the account opening threshold for mainland users by overseas brokerages has been raised step by step:

- Late 2022, the CSRC named them for the first time;

- May 2023, their apps were removed from mainland app stores;

- Starting 2024, only mainland residents who "actually work or live overseas" were accepted, requiring proof like overseas utility bills, credit card statements, tax documents;

- September 2025, the threshold was raised to requiring "proof of overseas permanent residence";

- Late 2025, only "non-mainland Chinese ID documents" were accepted;

- May 2026, fines were directly imposed on the brokerage entities.

The threshold for opening an account escalated from a utility bill all the way to an overseas passport or permanent residence card. The other side of this curve is precisely the process by which identity is being repeatedly repriced in the investment market.

Overseas Identity, the New Hard Currency for the Middle Class

For China's domestic middle class in 2026, overseas identity has become a latent asset class. It cannot be bought and sold like real estate, nor does it have a public quote like stocks, yet it possesses all the basic attributes of "hard currency."

First is scarcity. Hong Kong's various talent admission schemes approved around 140,000 applicants in 2024, with the vast majority coming from the mainland. It sounds like a lot, but against a population base of 1.4 billion, the penetration rate is less than one in ten thousand.

Unlike real estate, overseas identity doesn't depreciate due to population outflows, policy adjustments, or rising interest rates. At any given point in time, it corresponds to the same set of clear-cut rights and offers an extremely high rate of return. What it unlocks isn't just a single stock, but an entire dimension of asset allocation: US stocks, overseas real estate, offshore insurance, foreign currency deposits, compliant channels for crypto assets.

Most tempting is its non-transferability. Identity as an asset cannot be arbitraged in a secondary market like stocks. It can only be held by the individual, or transferred through three ancient methods: marriage, childbirth, and inheritance.

School district housing once spawned a complete gray industry chain: agents, transfer companies, fake household registrations, sham marriages, sham divorces. The overseas identity industry chain is now replicating all this: Hong Kong Quality Migrant Admission Scheme agencies, Portugal's Golden Visa, Singapore's Employment Pass, Malta citizenship, rapid Caribbean citizenship programs. Each product comes with a clear price list and processing timeline.

The form of the asset has shifted from a "property deed" to a "residence card," from a "school place" to an "account opening qualification."

The past two decades saw the middle class using school district housing to lock in social status; the next decade will see them using overseas identity to lock in assets.

Is Studying Abroad Equivalent to Buying Insurance?

Stepping back for a broader view, the logic behind the Chinese middle class purchasing overseas resources has been redefined three times over the past twenty years.

2000 to 2010 was about betting on overseas development potential. Sending children abroad for studies or families moving overseas was underpinned by an offensive judgment: opportunities were greater abroad. This was an investment, with the goal of returns.

2010 to 2020 was about diversification. After rapid domestic wealth accumulation, overseas real estate, insurance, and education were incorporated into the family asset framework for geographical dispersion. This was a defensive move, aiming for risk control.

2020 to the present is about "buying insurance." An overseas identity is no longer just part of the portfolio; it has become the entry ticket itself. Even if it generates no returns, without it, you lack the qualification to even enter certain investment markets. It is a premium paid to hedge against uncertainty, its price rising as uncertainty increases.

The regulatory hammer on May 22nd is yet another jump point on this "insurance price curve."

When a generation realizes they have missed the window to obtain an overseas identity themselves, they will transfer their hopes to the next generation. What will truly see price increases next might not be talent scheme agents, but rather spots in international schools, overseas university preparatory courses, and services for accompanying young children studying abroad. This "identity insurance" will be passed down through family generations.

I don't know which path that '90s individual with the 2046% return ultimately chose.

The evidence left behind after a year spent proving they are among the top 1% of the top 1% in the US stock and crypto markets should have been a highlight on a resume.

But after May 22nd, it became an attachment to a matchmaking profile.

A curve that could make a fund manager's eyes turn red is finally being used this way.

This is 2026.