Editor's Note: The following discussions are personal opinions and do not constitute investment advice. Information compiled from X.

Eileen Gu Joining Benchmark? Fake!

Popular Replies:

Next step: HTX Co-CEO, TRON Global Ambassador lol

She's been getting roasted these past few days—criticized in Chinese circles, called out in English circles, one moment representing Americans, the next representing Chinese!

Fun fact: Eileen Gu is a U.S. citizen, and the U.S. government taxes globally. So, 40% of every dollar she earns in China goes to the U.S. government!

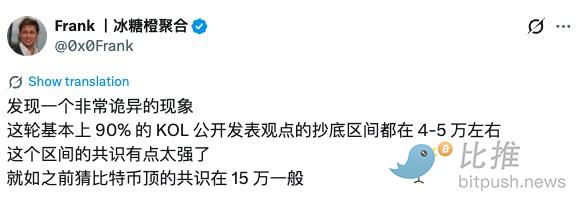

90% of KOLs' Bottom-Buying Range is $40K-$50K?

Popular Replies:

You're right on point. Actually, if it really drops to $40K-$50K, it would be reasonable. History is there, everyone gets it. The fear is if it drops to $20K-$30K or even lower—that would shatter all faith.

Hahaha, a couple of months ago they were shouting $60K. If it really drops to $40K-$50K, they'll start yelling $30K-$40K.

"Eight Years, Still $1900"—ETH Maximalists Collective Meltdown

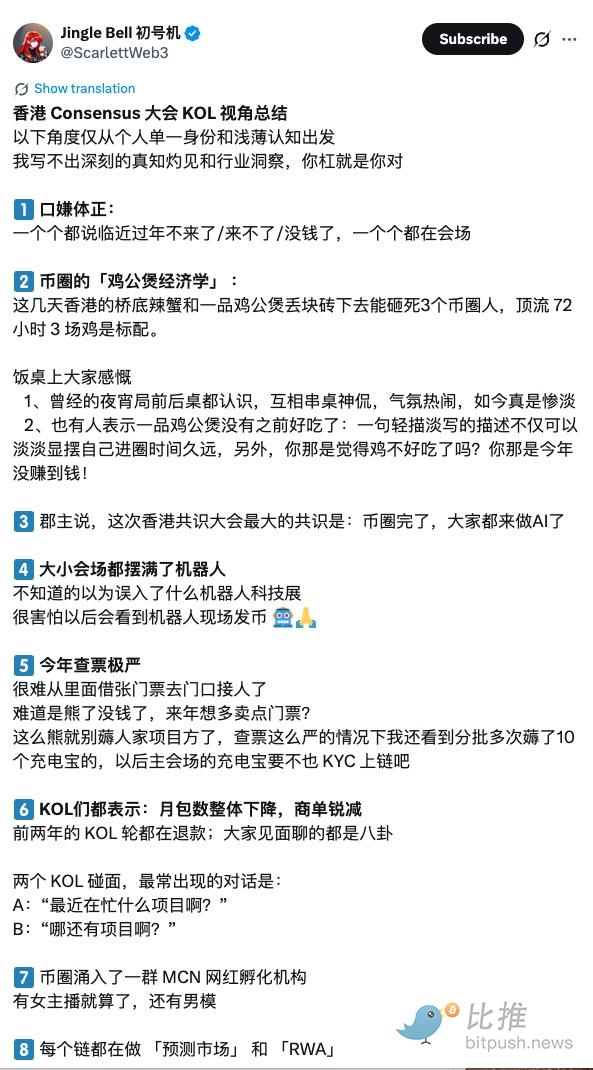

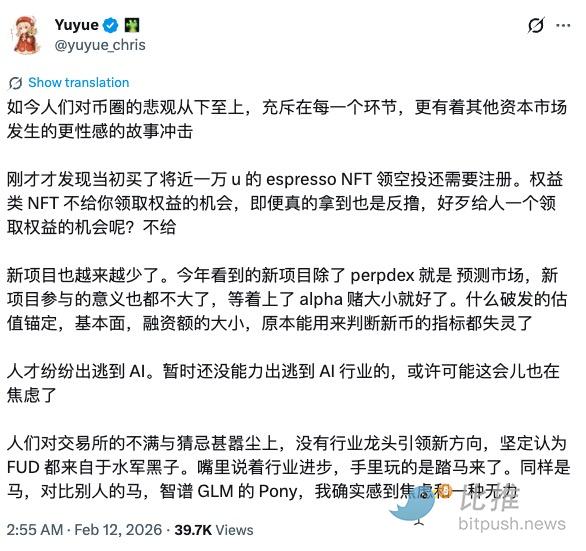

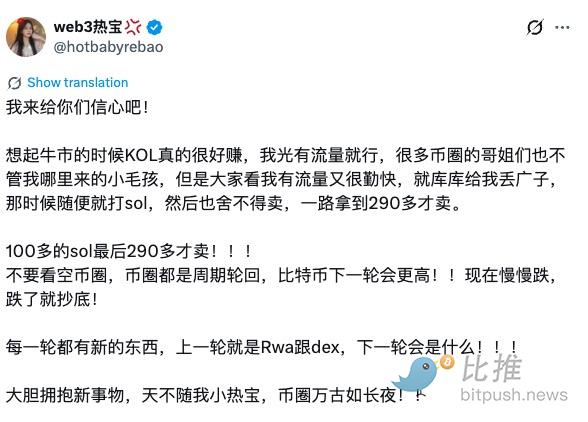

Hong Kong Conference Essay Extravaganza

Pessimism Pervades the Industry—Some Flee, Others Hold Firm

Popular Replies:

Extremes reverse—wait for the mean reversion. Right now, it's about resting. The sooner you rest up, the more advantage you'll have;

Just wait it out;

The AI circle's siphon effect should become particularly strong this year.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush