Article Author: Kyle Soska

Article Translation: Block unicorn

The cryptocurrency market has been in a risk-off state for several consecutive months, and I have been carefully studying various market data, looking for signs of a potential market turnaround. In this article, I will delve into the market structure of perpetual futures and, combined with data from the Ethena transparency dashboard, analyze market risk appetite.

In short: Ethena's deployed capital is at a multi-year low, only 71% of the 2025 low. This is not a criticism of Ethena, but rather a reflection of the current market conditions. Directional short positions are almost on par with directional long positions, an extremely rare and historically unsustainable balance in the cryptocurrency space.

The cryptocurrency market has long been characterized by the extreme volatility of its assets and the heavy use of leverage by traders. My previous research, "Understanding Cryptocurrency Derivatives: The BitMEX Case Study," explored the novel 100x perpetual contracts offered on BitMEX.

Since the BitMEX era, cryptocurrency futures have become the highest-volume product in the cryptocurrency market, with trading volumes 5 to 20 times that of the spot market. As a center for leveraged trading for retail investors, perpetual contracts can reflect the risk appetite of the cryptocurrency market and are therefore worthy of our attention.

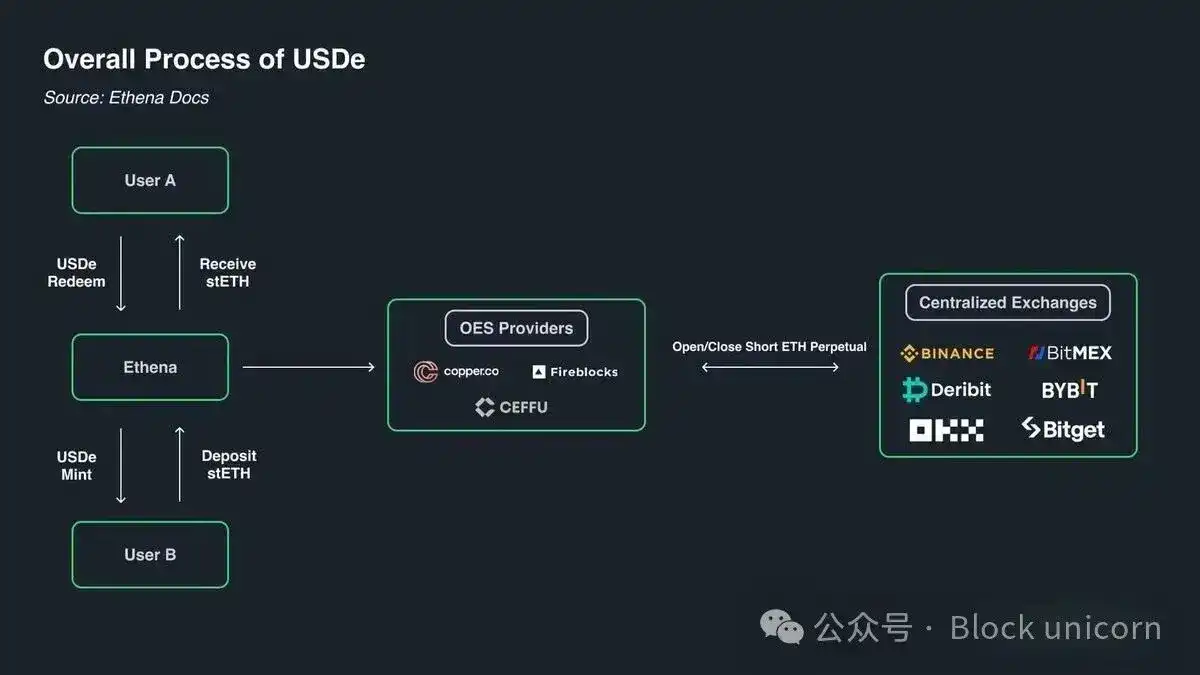

Ethena provides us with an extremely unique perspective, allowing us to gain deep insights into the cryptocurrency derivatives market. As shown in the figure below, Ethena implements a cryptocurrency arbitrage trade. The strategy is simple: when cryptocurrency traders go long, Ethena acts as their counterparty and goes short. Ethena ensures it buys exactly the same amount of assets as the traders are shorting. In a sense, Ethena provides a leverage service. Traders want to profit from rising cryptocurrency prices but lack capital; while Ethena has capital but limited risk tolerance. Therefore, traders use perpetual contracts to borrow funds from Ethena at the basis plus the funding cost of the perpetual contract.

(Chart: Ethena Mechanism Illustration)

By construction, each long contract corresponds to a short contract in a 1:1 ratio. Each open interest in perpetual contracts represents a cash flow agreement between two parties. The exchange's role is to facilitate the matching of these contracts, ensuring that each contract always has a sufficiently funded long and short holder. The table below shows the four possible outcomes facilitated by the exchange.

Perpetual Contract Matching Matrix

Every trade has a buyer and a seller. When both the buyer and seller of a contract are long or both are short, the exchange merely transfers ownership of the contract from one party to the other. This transfer does not create or destroy any contracts. When the buyer is long and the seller is short, a new contract must be created, with the buyer taking the long position and the seller taking the short position, increasing the open interest by 1 contract. On the other hand, if the seller is long and the buyer is short, the exchange can directly unwind the contracts of the buyer and seller and delete the newly released contract, decreasing the open interest by 1 contract.

So, who are the actual holders of these contracts in a typical market? I believe contract holders can be broadly categorized into four types:

-

[Long] Directional Longs

-

[Short] Directional Shorts / Hedgers

-

a. Direct Asset Shorts / Hedges

-

b. Structured Product Hedges

-

-

[Short] Basis Traders (e.g., Ethena, etc.)

-

[Hybrid] Perpetual Arbitrageurs

Directional Longs seek exposure. They are risk-takers, and their demand for risk depends on their level of risk appetite.

Directional Shorts include both investors who wish to take on the downside risk of an asset and investors who wish to hedge their assets in a tax-efficient manner. Venture capital firms and company employees compensated with tokens often wish to hedge tokens that vest at current prices. For altcoins, many markets are too small for effective direct hedging, or may not even exist. In such cases, companies like Cumberland, Wintermute, FalconX, Flowdesk, and Amber can construct dynamically managed synthetic positions, using short sales of Bitcoin and Ethereum and other highly correlated assets to hedge exposure to less liquid markets (e.g., Monad). Projects like Neutrl also employ this strategy, offering such hedging as a yield strategy.

Basis Traders are opportunistic shorts. They are not interested in directional risk but actively fill the excess demand from directional longs when market supply and demand are imbalanced. Under most market mechanisms, long demand exceeds short demand, and the basis traders' role is to bridge the gap. Their position sizes are usually highly elastic.

Perpetual Arbitrageurs hold both long and short positions in perpetual contracts simultaneously. Their role is to connect different perpetual contracts and correct any minor price discrepancies, at a cost not exceeding transaction fees. Their long positions perfectly match their short positions at any given moment.

By construction, all perpetual contracts are in a 1:1 ratio, with long positions perfectly matched by short positions, so we know:

Directional Longs + Arbitrage Longs = Directional Shorts + Basis Shorts + Arbitrage Shorts

Furthermore, the structure of perpetual arbitrage tells us:

Arbitrage Longs = Arbitrage Shorts

Canceling this term from the first equation yields:

Directional Longs = Directional Shorts + Basis Shorts

Ethena provides us with a proxy for all basis shorts, which helps us gain insight into the difference between directional longs and shorts.

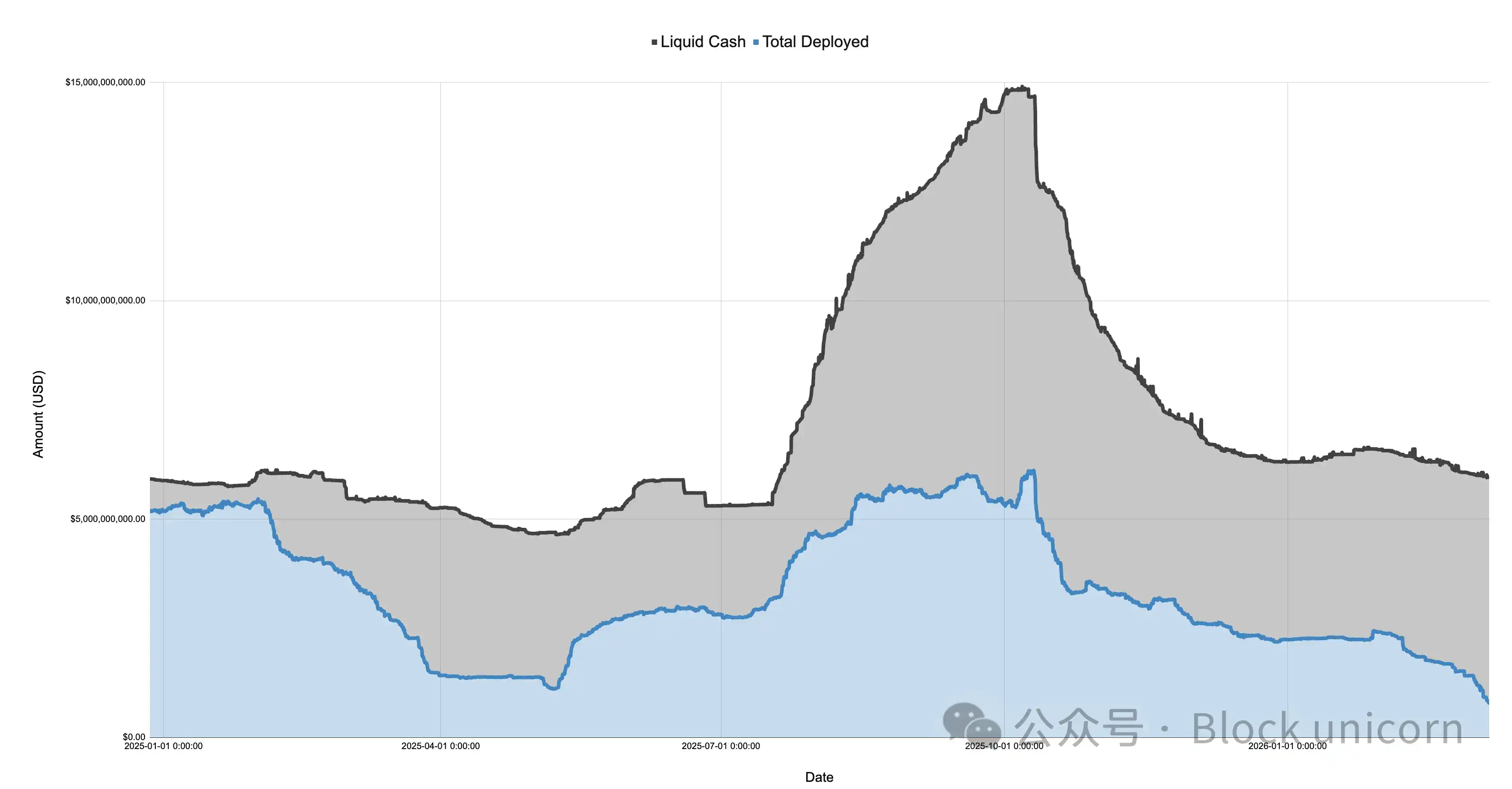

The chart below is Ethena's self-reported balance sheet, divided into cash and deployed capital, for the period from December 27, 2024, to March 7, 2026:

(Chart: Ethena Balance Sheet 2024-2026)

The market turned sharply risk-off in January 2025 after the launch of the $TRUMP token, followed by a continued decline during the initial tariff discussions and the "Liberation Day" in April. During this period, Ethena's deployed capital plummeted from over $5 billion to around $1.108 billion, a drop of more than 75%.

It is important to note that Ethena's deployed capital can serve as a reference for the degree of excess long demand in the market. Although Ethena is not the only institution conducting such trades, its size is substantial (sometimes around 25% of Binance and Bybit), and as long as it has ample cash, it will expand its positions to meet any unmet long demand. This suggests that while total long demand may not have fallen by 75% by April 2025, the excess demand not met by directional short covering did indeed fall by 75%.

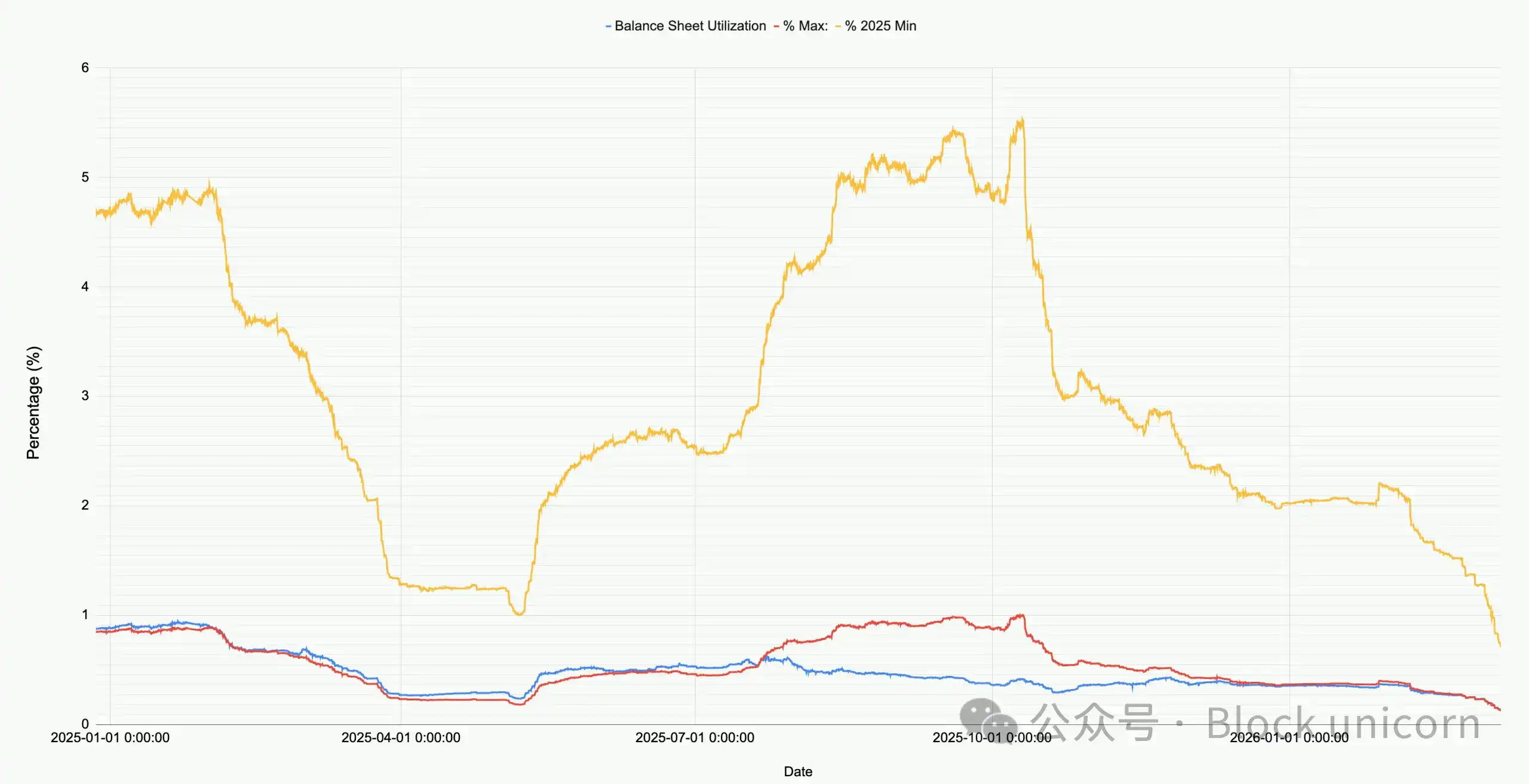

The chart below shows the deployment of Ethena's balance sheet relative to its total size, the 2025 minimum, and maximum values.

<极i data-index-in-node="0" data-path-to-node="29" style="font-size: inherit; font-family: PingFang SC,Helvetica Neue,Helvetica,Arial,Hiragino Sans GB,Heiti SC,Microsoft YaHei,WenQuanYi Micro Hei,sans-serif;">(Chart: Ethena Deployment Comparison)

Observing the current market, the total capital deployed by Ethena across all markets (BTC, ETH, SOL, BNB, XRP, HYPE) is only about $791 million. This is only 71% of the 2025 minimum and a mere 12.9% of the peak value before October 10th. This figure is not a criticism of Ethena but reflects the current market conditions: net long demand is at a historically low level.

It is particularly noteworthy that during the market crash where Bitcoin price plummeted to $60,000, Ethena deployed over $2 billion in capital. Since just a month ago, on February 8, 2026, Ethena's deployed capital has astonishingly decreased by 60%!

The chart below zooms in on Ethena's deployed capital and the price trend of Bitcoin since January this year.

(Chart: Ethena Deployed Capital vs. Bitcoin Price Trend 2026)

Since the Bitcoin price fell to $60,000, Ethena's basis positions have shrunk by over 60%, from over $2 billion to less than $800 million. This change is puzzling because the market has been relatively stable during this period. The reasons for this are as follows:

-

Profitable but unsustainable basis trades established after the February crash (the basis turned negative, but funding rates were also negative) are being gradually unwound.

-

Increased hedging activity from directional shorts and price-insensitive participants is squeezing out opportunistic basis traders.

-

Insufficient demand for leveraged exposure from longs.

(Chart: Open Interest vs. Funding Rate Trend)

In my opinion, the truth is primarily determined by a combination of factors 1 and 2, with factor 3 playing a minimal role. As shown in the chart above, during this period of gradual Ethereum project unwinding, the overall open interest for Bitcoin (and other major cryptocurrencies) has remained relatively stable. Meanwhile, funding rates have been negative for an extended period, with many cryptocurrencies (e.g., SOL) having cumulative negative funding rates across multiple exchanges. This indicates an increasing demand for shorting or hedging some form of risk exposure.

If I had to guess, I would say that small and medium-sized cryptocurrency companies and venture capital firms are both facing a crisis. Think of small-cap projects like Eigen, Grass, Monad, etc. There are hundreds of such cryptocurrencies, each representing dozens of venture capital firms and a company with capital and employees. Venture capital firms need to control losses and lock in profits to meet fund investment targets, and these companies need to ensure cash flow and headcount. This creates a situation where all participants want to squeeze the maximum benefit from the "stone," and the answer lies in relatively crowded trades through actively managed structured products that short a basket of correlated assets.

We saw the presence of these structured products during Ethereum's (ETH) explosive rally days, which also triggered short-covering rallies in numerous small and medium-sized cryptocurrencies. Another piece of evidence is the significant crowding out of opportunistic basis traders like Ethena.

Regardless of the specific reason, we can be sure that this is the first time in the history of the crypto market that directional longs and directional shorts have almost reached equilibrium. There is no充分 reason why this state cannot become the new normal, nor can it be proven that this market regime must change, but looking at other asset classes and markets, it is very unusual for such a trend to persist.