Starknet

Project Twitter: https://twitter.com/Starknet

Project Website: https://starknet.io/

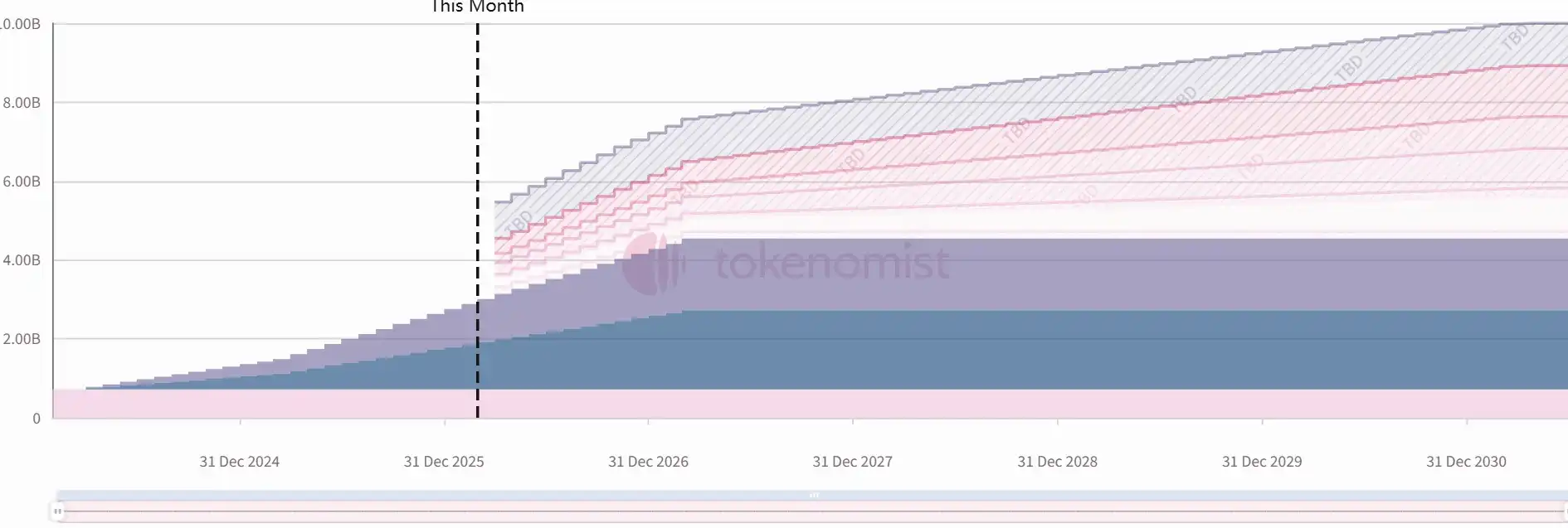

This Unlock Amount: 127 million tokens

This Unlock Value: Approximately $4.84 million

Starknet is an Ethereum Layer 2 that utilizes zk-STARKs technology to make Ethereum transactions faster and reduce fees. StarkNet's parent company, StarkWare, was founded in 2018 and is headquartered in Israel. Its main products include Starknet and StarkEx. By using STARK, Starknet verifies transactions and computations without requiring all network nodes to validate each operation. This significantly reduces the computational burden and increases the throughput of the blockchain network.

The specific release curve is as follows: